Most of you know I spend my days gathering “thin reeds” and try to weave them into a favorable “investment bouquet.” As Yogi Berra said, “You can observe a lot by just watchin’!” To this point, about a month ago I wrote:

While seeing accounts in San Francisco recently, I read a story about Boston-based Fidelity having a good year in 2014 from an earnings and revenue standpoint, but that they were losing assets to passive investments, aka index funds, ETFs, etc. Here the observation is that this is what you see at inflection points where individual investors are doing the exact wrong thing at the wrong time.

Since then numerous articles have suggested that you can’t outperform the indices, so you should just index your portfolio and forget it. The flow of funds data indicates that is exactly what many investors are doing; and why not, after a few years where ~90% of active portfolio managers have underperformed the S&P 500 (SPX/2108.10). Last week there was yet another article titled “The Bottom-up Stock Picker Is Dead.” I felt like sending that article to some famed “stock pickers” like Ron Baron, but thought better of it. Harkening back to the “thin reeds” approach, you tend to hear about indexing, worthless robo brokers, and such stuff around inflection points. The inference is, you should probably be selling, or at least reducing, your passive investments and switching those funds to active managers. It’s not that passive investments don’t have a place in portfolios, but at this stage of the market cycle I would underweight passive investments and overweight active investments.

In my February 23, 2015 Strategy Report I discussed The Wall Street Journalarticle, “The Case for the Active Mutual-Fund Manager” by Michael A. Pollock. Mr. Pollock began with, “Index funds clearly have won the hearts and minds of many investors.” A paragraph later he writes, “Little surprise, then, that last year, people yanked $98.58 billion out of actively managed U.S.-stock mutual funds while putting $71.34 billion more into ‘passive’ ones that merely track an index.” Hereto, the observation for the contrary investor is that participants should be doing the opposite. The article goes on to state five reasons why you should consider active management at this stage of the bull market (as paraphrased):

- Investors have flocked to dividend-paying ETFs for income as yields have fallen. Such ETFs, however, are often focused too narrowly on certain sectors. Such ETFs only sell a stock if it no longer fits the mission. Meanwhile, if market sentiment shifts away from that sector, it can hurt its performance. An active manager could limit the impact of such shifts by diversifying.

- If the markets start trading sideways, like they did from 2000 – 2008, nearly two-thirds of active managers of large-cap funds beat the S&P 500.

- Bond yields are likely headed higher. Since yields move in the opposite direction of bond prices, if rates are going higher it could be risky to own an ETF that closely tracks a broad bond index.

- ETFs make it easy to get non-U.S. exposure. But those ETFs tend to be based on market capitalization weighted indexes that tilt toward the largest foreign markets, often exposing investors to weaker markets like Russia and Western Europe. Active managers can fare better by diversifying away from such markets.

- If you are worried about volatility, active managers have more ways to play defense. They can own higher-quality stocks and trim positions as valuations rise. They don’t have to have the “pedal to the metal” when markets are going up, and they can put a brake on more quickly when markets are going down.

Also speaking to this point, Rob Isbitts published a MarketWatch article in December 2014 titled “Index Funds Beat Active 90% of the Time; Really?” Using the timeframes of 15 years, as well as 10 years, ending 12/31/13, he found:

Specifically, there were no time periods in which the S&P 500 outperformed 90% of mutual funds. The index was a middle-of-the-road performer in most of the 24 separate time period/peer group combinations we studied. During the two bull periods, the index outperformed 80% and 63% of its peers. However, during the down market cycles (bear), the index beat only 34% and 38% of its active management competitors.

Another, almost unreported “thin reed,” is that index king Vanguard Group’s actively managed funds outperformed their respective index benchmarks. To wit, “Over the last three years, 20 out of Vanguard’s 30 actively managed stock funds outperformed their benchmark,” according to Thomson Reuters (dated 12/2014).” So I will say it again, “I would rotate out of, or at least reduce, passive investments and into active investments at this stage of the market cycle. Yet, a few other rotations are going on currently.

In talking to a number of portfolio managers (PMs) at our recent institutional investors conference I gathered that one of the rotations is out of U.S. stocks and into European stocks. As one PM stated, “It’s not that the U.S. has lost its status, not because the U.S. is going to have negative returns, but because other places around the world have become more attractive.” And it’s true; places like Europe are cheaper than the U.S. Moreover, many think Draghi’s quantitative easing bazooka is going to produce the same kind of asset elevation seen in the U.S. since 2009. While I would like to believe that, I do not. Certainly there are select companies in Europe that are attractive, but strategically I don’t think Europe is there. For Europe to get to a better structural place over the next three to five years requires policy reform, particularly in France and Italy, and I just don’t think that is in the cards any time soon.

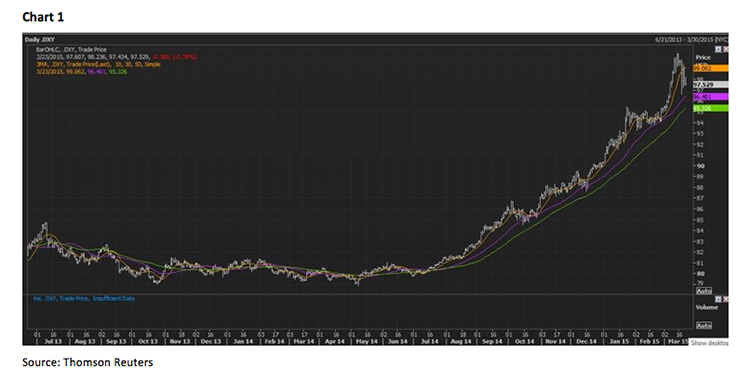

The other noticeable rotation is into small- and mid-capitalization stocks here in the U.S., driven by the belief the strong dollar is going to the hurt the earnings of many of the international companies that populate the S&P 500. With last week’s 2.66% sprint, the SPX is now up 2.39% year-to-date (YTD). However, the S&P MidCap is up 6.00% and the S&P 600 SmallCap is better by 4.63%. I also find it interesting that “growth” is beating “value” with MidCap Growth up 8.64% YTD, while SmallCap Growth is higher by 8.02% YTD. To be sure, the strong dollar is impacting many international companies. It is also true the small/midcap complex has much less exposure to currency fluctuations. Accordingly, this rotation makes sense to me. That said, a number of indicators suggest the Dollar Index rally is going into a pause, if not a pullback, phase, having made a trading top on 3/13/15 with a peekaboo “look” above 100 (see chart 1 on the next page). As for crude oil, I still think it is in a bottoming phase and may have already bottomed.

The call for this week: To use another Yogism, “It’s déjà vu all over again” because last week was reminiscent of the week of February 22, 2015 where there was a Greek deal and dovish words from the Federal Reserve that caused stocks to jump. Last week’s Dow Dance took the senior index within ~161 points of its all-time closing high of 18288.63 made on March 3, 2015. Not to forget the Industrials made a new all-time high last December. What is interesting here is that the D-J Transports (TRAN/9148.13) are close to their all-time high of 9217.44. If the Trannies can close above that level, it would be yet another Dow Theory “buy signal.” This morning, however, the S&P preopening futures are lower (-4.50), troubled by the letter Greece’s PM wrote Merkel about the “impossible debt obligations” and the Houthis seizing a strategic Yemeni city.

(c) Raymond James