- A disorderly decline in energy prices could spill over into consumer and business sentiment, which would worsen any drop in Canada’s economic output.

- More rate cuts this year are likely a part of the Bank of Canada’s base case scenario.

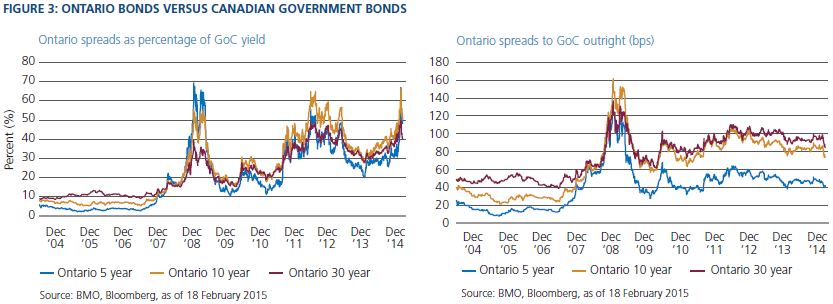

- Investors may be able to improve their returns by buying bonds with high-quality credit spreads, including Canadian bank senior debt and Ontario bonds.

On 21 January 2015, the Bank of Canada surprised the market by cutting the overnight rate by 0.25% to 0.75%. We at PIMCO were a bit surprised by the Bank’s rate cut, and we weren’t alone – none of the 22 forecasters followed by Bloomberg anticipated this move. On the same day, the Bank also cut its 2015 GDP growth forecast by a modest 0.3% due to lower energy prices, in line with our Canadian cyclical forecast in December. But given the expected pickup in exports driven by the U.S. economic recovery, we did not view the Bank’s forecast as negative enough to change monetary policy.

Why is the Bank of Canada providing this “insurance” of sorts against sliding oil prices? It is concerned that a relatively orderly decline in oil prices (see Figure 1) is in the process of turning disorderly. A disorderly decline in energy prices could spill over into consumer and business sentiment, which would create a bigger drop in economic output than traditional bottom-up models would forecast.

We expect the Bank of Canada to write more “insurance” in 2015

What is clear is that the Stephen-Poloz-led Bank of Canada is unequivocally dovish, and far more dovish than it was with Mark Carney at the helm. Carney was more concerned with financial stability risks, while Poloz is more concerned about economic growth. The Poloz-led Bank of Canada has consistently looked through positive economic data and highlighted weak economic data. For example, one year ago, the Bank dropped its tightening bias, citing concerns that the key core inflation rate was too low (its forecast for core inflation was 1.5% in 2014). Despite core inflation meaningfully rising above the Bank’s 2% target (now at 2.2%), it has dismissed the surprises as one-off effects (see Figure 2).

Most interestingly, Poloz has modified the Bank’s inflation-targeting reaction function that has served it well for decades. The Bank’s target is headline inflation of 2% (with a control band of 1% to 3%). Given the volatility of headline inflation, the Bank uses core inflation (which strips out the eight most volatile components) as the operational guide to determine inflationary trends. As rising core CPI invalidated the Bank’s dovish stance in 2014, the Bank created a new CPI measure called component CPI, which is about 0.5% lower than core CPI. Ditto for the forecast of the output gap. When the traditional measure of the output gap showed that it had virtually been closed, the Bank created a new “integrated” output gap measure that showed the economy has slack of approximately 1.5% of GDP.

So what should we expect in 2015? No reason to believe the doves will not continue to fly. While oil prices have recovered modestly since 21 January, we still think the Bank will write more “insurance” for the economy in the form of another 25-basis-point rate cut this spring, and possibly a third rate cut later in 2015 (depending on oil prices and economic data). In the appendix to the latest Monetary Policy Report, the Bank simulates that the recent decline in oil should cause output to drop by 1% in 2015 (given no change in monetary policy); given that its 2015 GDP forecast declined by only 0.3%, it is reasonable to imply that more rate cuts are part of the Bank’s base case scenario.

While the Bank of Canada has operational independence from the federal government, it is a federal election year. Lower energy tax receipts will make it tougher for the federal government to stick to its plans to balance the budget while living up to its promises to provide some tax relief. The Bank taking out a “monetary insurance policy” will likely be helpful to the federal government as it evaluates its fiscal options.

The Bank of Canada’s recent decisions have broader implications

Globally, central banks are struggling with their communications strategies. While central banks that are stuck with a zero interest rate policy (ZIRP) or a quantitative easing (QE) program are still using forward guidance to lower term premiums, Poloz has favored a style of less forward guidance. He put an exclamation point on this when he cut rates last month without providing previous guidance that this was a realistic possibility. The 28 January minutes from the U.S. Federal Reserve show that many members of the Federal Open Market Committee also favor less forward guidance. The Bank of Canada may be leading a new trend where central banks try to maintain maximum optionality in the short term by limiting forward guidance. It looks like these central banks (not bound by QE or ZIRP) will likely be emphasizing medium-term goals like the gradual pace of tightening by the Fed or the “insurance” nature of the cuts by the Bank of Canada. These central banks may suffer from short-term overshoots by markets as investors come to terms with their new communication styles.

We think that Canada may suffer more volatility than most markets when the Bank decides it needs to move to a tighter monetary policy. Not only will investors likely receive less forward guidance from the Bank, but they need to figure out the Bank’s new reaction function. Should investors focus on core inflation (which has been the key for the past two decades) or the component CPI? What happens if the traditional measure of the output gap weakens while the new integrated output gap measure improves?

While nominal yields look expensive, investors have to be patient

While the Bank has introduced some confusion regarding its medium- to long-term reaction function, in the short term, there is no confusion: It is dovish. For the foreseeable future, we expect it to continue to look past strong data and focus on weak data.

Long-term nominal bond yields look unattractive (10-year yields at 1.4% and 30-year yields at 2.0%), especially given the Bank of Canada’s long-term track record of successfully hitting its 2% inflation target. Currently, the breakeven inflation rate is 1.7% for 30-year real return bonds. We think it is highly unlikely that inflation will average 1.7% for the next 30 years and that 30-year real return bonds will outperform 30-year nominal bonds in the years to come.

That said, there is no reason for investors to underweight Canadian interest rates in 2015 with a dovish Bank of Canada possibly on its way to setting the overnight policy rate back to the crisis level of 0.25%. We think investors should pick up these paltry yields until the data turn compellingly obvious that the Bank’s monetary policy is too loose, and this will likely include oil prices stabilizing above $60 per barrel.

In the meantime, investors may be able to improve their returns by buying bonds with high-quality credit spreads. Instead of investing in five-year government bonds at 0.8%, investors can more than double their yield by buying the senior debt of Canadian banks at 1.75%. Instead of 10-year government bonds at 1.4%, investors can get 50% more yield by investing in Ontario bonds at 2.15% (see Figure 3).

While the investment environment may not be particularly attractive, there are ways for investors to escape the government’s financial repression and improve returns.

(c) PIMCO

© PIMCO