Investors have long relied on the assumption that asset returns are normally distributed with correlations that are slow to change.

Based on our analysis, however, we now have flat distributions and correlations that are much less stable; a fat-tailed event to either the left or the right is as likely to occur as a non-event.

Active management that recognizes and adapts to these changes will be essential to seeking strong returns in the future.

Economists, financial engineers and traders have long relied on the assumptions that asset returns are “normally” distributed with correlations that are slow to change. However, the New Neutral, the current environment of slower global growth and lower neutral policy rates, and new geopolitical events are leading to price action that is less apt to follow this rule. Returns (and price action) are likely to be less “continuous,” more violent and more random in the future given the structural changes in initial conditions and end investor reaction functions.

There are many reasons that the familiar underlying assumption of normally distributed returns and stable correlations may not describe realized asset returns going forward, including:

- Changing and erratic central bank policy (including negative interest rates)

- New global regulations

- Less balance sheet availability from market-makers to provide liquidity (lower leverage ratios)

- Global uncertainty over growth prospects

- Divergence in global central bank policy – as bankers respond to regional economic conditions with the backdrop of a multi-speed global recovery

- Increasingly narrow client mandates leading to “herding” action in asset classes

A “normal” distribution meant that the odds of a market move up or down were equal and that over the long term, the average expected return was symmetric around the “trend” return (similar to flipping a coin). During and after the financial crisis, there had been increased talk of “fat tails,” “black swan events” (Taleb 2007) and “bi-modal” distributions – all pointing to the fallacy of normal distributions (or the higher probability of more violent market events).

But these concepts were not widely accepted in 2008, and certainly most market participants had not planned or reserved capital for them. As a result, when the market repriced in 2008, the knock-on effects were disastrous: Very few participants had contingency plans in place for the market’s new, more volatile state.

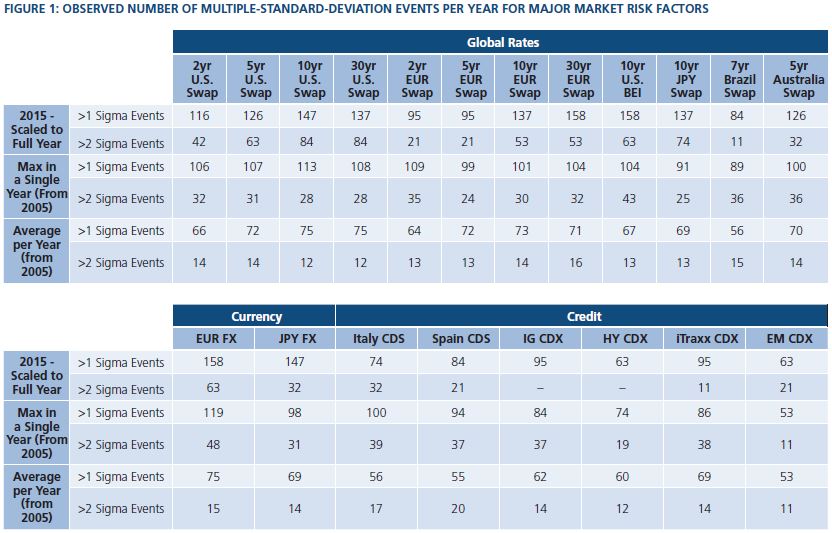

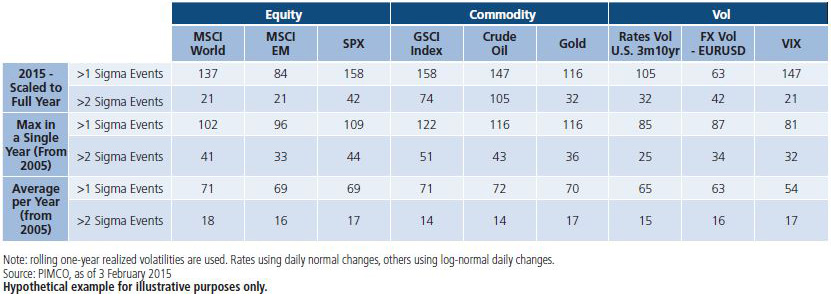

The same could be said today: Volatility that affects returns across markets still catches many participants by surprise. But based on our analysis of the current market versus historical performance, such events are now part of the New Neutral landscape. Take, for example, the number of multiple-standard-deviation events that have occurred to date in 2015 assuming that this pace continues for the remainder of the year versus the 10-year history of these events, as shown in Figure 1. In the major markets PIMCO tracks daily, all except credit have seen dramatic increases in these large moves. (Note that if we assume returns are normally distributed, then a two-standard-deviation event will occur approximately 23 out of 1,000 observations, a three-standard-deviation event approximately 1.4 times out of 1,000 observations, and a four-standard-deviation approximately three times out of 100,000.)

Additionally, there have been at least seven four-standard-deviation events in 2015, several of which have been driven by central bank policy changes, including the Swiss National Bank’s recent removal of its currency peg, easing of monetary policy in Canada and Russia and larger-than-expected asset purchases by the European Central Bank. Changes in the yield curves in Japan and Europe in response to policy changes have also played a part in these events.

Investment implications

Today, market-makers and risk takers are well versed in fat-tail analysis and stress-test methodologies to manage the risk of multiple-standard-deviation events. Is the world better off? Yes and No.

Initial conditions have changed so much and central banks have become so much less predictable since the financial crisis that market participants should have much less confidence in estimating the size or direction of market moves.

As discussed earlier, structural changes in initial conditions have led to higher probabilities of multiple-standard-deviation events that are larger in size and have different relationships to each other than in the past. This is why PIMCO believes that a fat-tailed event to either the left or theright is as likely to occur as a non-event is – we now have flat distributions and correlations that are much less stable. As illustrated in Figure 2, the probability of small market moves that would otherwise be expected when considering a normal distributed variable, shown by the green line, is reduced and instead larger moves may occur with higher probability, shown by the purple line.

In our view, portfolio construction should be particularly mindful of hidden (or assumed) correlations and regime transitions, and traditional normal distribution assumptions for pricing risk are no longer fully valid. We believe active management that recognizes and adapts to such fat tails and changing correlations will be essential to seeking strong returns on capital – as well as the return of capital itself – going forward.

Past performance is not a guarantee or a reliable indicator of future results. This material contains hypothetical results based on theoretical investment and statistical principals. Hypothetical and simulated examples have many inherent limitations and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated results and the actual results. There are numerous factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect actual results. No guarantee is being made that the stated results will be achieved.

This material contains the opinions of the authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2015, PIMCO.

© PIMCO