(Due to the President’s Day Holiday, the next report will be published Feb. 23rd.)

After the Syriza party won 149 of the 300 seats in the Jan. 24th Greek elections, European markets have been roiled by worries over another crisis developing. The party has engaged in some provocative behaviors; its leader and Greece’s new prime minister, Alexis Tsipras, decided that his first official visit would be to a monument that honored Greek citizens who suffered a mass execution at the hands of the Nazis. That symbolism wasn’t lost on anyone. Tsipras, and his new finance minister, Yanis Varoufakis, have indicated that they have no interest in fulfilling the bailout requirements of the European Central Bank (ECB), the European Union (EU) and the International Monetary Fund (IMF), the “troika” that has managed the bailout for Greece.

Austerity has severely harmed Greece’s economy, cutting its GDP by 26% from the pre-crisis peak. The unemployment rate is 26% and youth unemployment is over 50%. The election of Syriza is a reaction against the economic depression that Greece has endured as Syriza ran on an anti-austerity platform.

Of course, one nation’s austerity is another nation’s reform. The German position, which has become the establishment position in Europe,[1] is that excessive Greek fiscal spending and borrowing is responsible for the problems in Greece. This excessive spending and borrowing is seen as leading to rampant corruption, gold-plated salaries and benefits for government employees and economic inefficiency. Only reforms, or austerity, can bring Greece any hope of recovery.

The Greek and anti-establishment position is that Germany is the cause of not just Greece’s economic collapse, but the economic crisis in the Eurozone periphery.

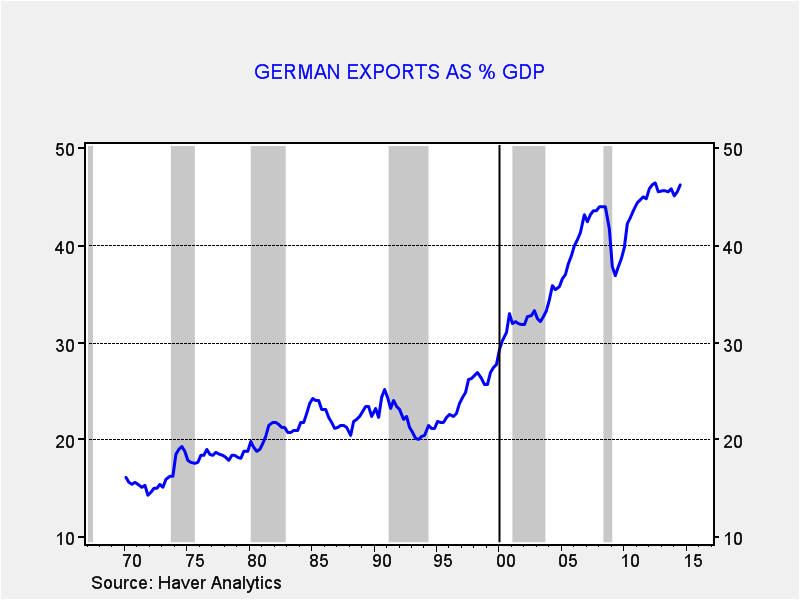

This chart shows German exports as a percent of GDP. Prior to reunification, exports generally represented around 23% of German GDP.

Exports rose as the German government changed policy following reunification and have moved steadily higher since the euro was formally introduced in 2000, now representing over 45% of Germany’s GDP.

Germany engaged in policies after reunification that were designed to reduce labor costs, improve productivity and build saving. These policies made the German economy overly dependent on exports that were mostly sold within the Eurozone, which for Germany is a single-currency free trade zone.

In order to sell these exports to the rest of Europe, German banks engaged in a sort of “vendor finance,” where German banks and investors bought the debt from the periphery who then purchased German exports. Of course, this problem was exacerbated by the use of a common currency and the perception among investors that the bonds of individual countries in the Eurozone were, somehow, mutualized. In other words, no country would default because the Eurozone was unified. Thus, borrowing costs fell to northern European levels in the periphery which spurred even more consumption in the southern regions of the Eurozone. Of course, we now know the debts were not mutualized and that the Eurozone has serious unresolved issues.

In this report, we are going to use game theory to describe the situation between Greece and the EU/Germany/ECB. This method shows how misunderstandings can develop and how catastrophic mistakes are made. Using this structure, we will outline the positions and perceptions of both sides and describe how this situation could lead to another crisis. As always, we will finish with market ramifications.

Game Theory

Game Theory was developed after WWII and was used by analysts to predict behaviors between a limited number of players. In economics, it is often used to describe the interplay between firms in an oligopoly. In defense analysis, it was used heavily to create the rules of the road between the U.S. and the U.S.S.R. The concept of “mutually assured destruction,” or MAD, came out of game theory.

The canonical game in Game Theory is Prisoner’s Dilemma. It describes a situation in which two players, acting in a rational fashion, end up with a less than optimal outcome.[2]

|

Quiet |

Rat |

|

|

Quiet |

1,1 |

10,0 |

|

Rat |

0,10 |

3,3 |

Game theorists have created iterative tournaments to observe how players behave in multiple rounds. A number of interesting outcomes have developed; in general, the best strategy is “tit-for-tat,” which is to be quiet until someone rats then always rat with that particular player. They have also noticed that “nice” players tend to congregate with each other and group-punish defectors. In a single play without collusion, we expect the Rat/Rat outcome. In economics, when that outcome isn’t observed, regulators often fear that collusion has occurred which often leads to antitrust violations under U.S. law. At the same time, prisoner’s dilemma undermines the idea that economic actors, operating under conditions of self-interest, will always arrive at the most optimal solution. The prisoner’s dilemma game suggests that under conditions of imperfect competition, a less than optimal outcome is likely if participants follow self-interested behaviors.

Another canonical game is chicken.[3]

|

VEER |

HOLD |

|

|

VEER |

-5,-5 |

-5,+10 |

|

HOLD |

+10,-5 |

-100,-100 |

If both veer, both suffer some loss of face. If one veers and the other doesn’t, the holding player wins. If both hold, they suffer severe damage.

This game assumes that the losses are symmetric. The MAD concept assumes a game of chicken, in which Veer becomes No Attack and Hold becomes Attack. If both attack, the world ends. If the losses become asymmetric, then one of the players who perceives that his relative loss is less may consider a hold position. That is why, in MAD, treaties were put in place to prevent the creation of missile defense systems for fear it would make one of the parties believe that their losses in an Attack/Attack outcome would be survivable and thus encourage war. As long as both parties believe that complete destruction is the most likely result, neither would attack. In effect, if both players can create rituals that minimize the costs of “loss of face,” a chicken game can be repeated.

Greece, the EU/Germany/ECB and Chicken

We believe that Greece and the Eurozone are effectively engaged in a game of chicken. However, Alexis Tsipras has concluded that the payoffs are more favorable to Greece than those of his predecessors, and so he is willing to risk a financial crisis to get the troika to Veer. The establishment is equally worried that Tsipras has underestimated the dire straits his nation is in and is at risk of triggering a crisis that may lead to Greece’s exit from the Eurozone.

Syriza’s Positions and Issues:

Positions:

- The party believes that the German economy is so dependent upon the Eurozone for its export-driven economy that it cannot risk anything that would lead to a breakup of the single-currency bloc.

- It also believes that the exit of Greece from the Eurozone would set off the exodus of other nations and bring into question the entire European unification project that began in the 1950s with the European Coal and Steel Community. A breakdown of this order would trigger fears that Europe is heading into a period of rising nationalism that was responsible for two world wars in the last century.

- Syriza believes that an ECB cutoff of liquidity from its banking system would trigger bank runs in the periphery nations and trigger a broad banking crisis in the Eurozone. The inability to contain bank runs may have led Chancellor Merkel to bail out Greece in 2012.

- It also believes that the ECB will not take steps which would force Greece out of the Eurozone. To have a non-elected central bank essentially make a major political decision of this magnitude would undermine the concept of a democratic Europe.

Issues:

- Syriza ran on an anti-austerity platform. To agree on extending the current bailout package would seriously undermine the party’s support and might lead to a breakup of the coalition. Syriza is itself a broad mix of radical and center-left members; about one-third of Syriza is controlled by Left Platform, a group of unreconstructed Marxists. Any backtracking would likely lead to this group leaving the coalition and trigger new elections.

- Syriza must deliver on some easing of austerity. Tax receipts fell as it became apparent that Syriza was likely to win as Greeks are expecting a sort of “austerity holiday.” If nothing changes, Syriza will face a nasty domestic backlash.

- Greece will not be eligible for bailout funds if it does not agree to an extension of the current program, which it has vowed not to follow. Although the country could probably scrape by as its fiscal situation has improved due to austerity, its banks need liquidity from the ECB. If the ECB decides not to support the banks without a bailout extension, which the ECB is signaling, bank runs are very likely. Essentially, Greece has until 2/28 to make a deal. Syriza wants the ECB to fund its banks for six months to give it time to negotiate. At this point, it doesn’t look like it will get that buffer.

- Syriza is a party of government newcomers. Nearly all of its members have limited experience in formal governing. The potential for mistakes are elevated due to the party’s lack of experience. It isn’t obvious how much time the Greek electorate will give Syriza if it can’t restructure the debt quickly.

EU/Germany/ECB Positions and Issues:

Positions:

- The group seems to believe that Greece could exit and contagion would be limited. First, while Greek sovereign yields have increased with Syriza’s election, the yields of other periphery nations have not. This was not the case in 2012. Second, the collapse of Portugal’s second largest bank, Banco Espirito Santo, last August suggests that European regulators can, with the efficiency of the FDIC, close a large bank and quickly contain any damage. This bank, an €80.7 bn institution, was split into a “good” and “bad” bank last August without incident. Policymakers believe that any banking crisis that spreads beyond Greece could be handled as efficiently.

- Germany especially fears that its vision of reform (called austerity elsewhere) would be irreparably harmed if Greece were to receive significant debt relief. The mainstream parties that have embraced reform, like those in Spain, would be seriously hurt if Syriza were successful. When the Popular Party in Spain argued that austerity was the only program available, it put tremendous strain on its economy. However, its leader, Mariano Rajoy, is now calling his country the “Prussia of the South” as the economy begins to lift. If Syriza succeeds in getting a deal, it will call into question why Rajoy subjected Spain to austerity. Simply put, if Merkel doesn’t stop Syriza, the German view of reform will be undermined throughout the Eurozone.

Issues:

- If Greece is given relief, it will foster nationalist parties in Europe which are showing signs of strength. It would also support Chancellor Merkel’s most potent opposition, the AfD Party, which is calling for German exit from the Eurozone. If Germans begin to fear that they will be on the hook for paying the bad debts of other Eurozone nations, the message of AfD will become increasingly attractive.

- Unlike in 2012, nearly all of Greece’s foreign-held sovereign debt is with international organizations, like the IMF, at the ECB or with national central banks. If Greece defaults, it will be the taxpayers who will be on the hook to recapitalize the banks or the ECB will need to print money to cover the losses.

- The ECB does not look inclined to help. Greece has a line of credit with the ECB of €15 bn backed by Greek T-bills; Greece wants to expand to €25 bn by using more of its debt. The ECB has indicated that this won’t happen. Although the ECB is still allowing Emergency Liquidity Assistance (ELA), this source is more expensive and is issued by the Bank of Greece. If a bank fails, Greek taxpayers will be hit for recapitalization. President Draghi used a lot of political capital to implement QE; it seems unlikely that he would expend more to defy the Germans to support Syriza.

The Source of Error

The following payoff table is, in our analysis, Syriza’s perception of the current situation.

|

GR \ EU |

CAVE |

HOLD |

|

CAVE |

-100/-10 1 |

-100/+10 3 |

|

HOLD |

+100/-30 2 |

-100/-1000 4 |

Our view is that Syriza believes that caving in to the EU will end its political movement before it really begins. Caving in produces the outcome of -100 in quadrants one and three. Thus, its only positive payoff is to press for restructuring at all costs, while the EU caves (quadrant two outcome). At the same time, we think Tsipras believes that the costs to the EU of caving to Syriza aren’t all that high, but a situation in which both parties hold (quadrant four outcome), which probably entails a Greek exit from the Eurozone, is devastating for the EU. If the Eurozone breaks up, the Pandora’s Box of European nationalism is released with all the risks that entails. The conditions that led to two world wars will return. And, most importantly, Germany loses its single currency free-trade zone. Thus, we fear that Syriza has concluded that the EU/Germany/ECB has no choice but to cave as long as Syriza holds firm.

The following is our view on the EU/German/ECB payoff table.

|

GR \ EU |

CAVE |

HOLD |

|

CAVE |

-10/-10 1 |

-10/+10 3 |

|

HOLD |

+100/-1000 2 |

-1000/-10 4 |

From the troika’s perspective, a face-saving outcome in which both parties cave on some matters is the best outcome. They fully expect Syriza to take that option and believe the aggressive comments against extending the current deal or even more “extend and pretend” on debt is just political rhetoric for domestic consumption. Thus, the leaders of the EU keep looking for Syriza to signal a first quadrant outcome. They also believe that a Greek exit won’t be a big deal for the Eurozone but a catastrophe for Greece. Thus a quadrant four outcome should be unthinkable for Greece but not overly costly for the Eurozone. On the other hand, a quadrant two outcome, in which Greece holds and gets its way, while the EU caves, is good for Greece but terrible for the Eurozone. The German reform effort will be over. Populist parties across Europe will use Syriza’s success to rebel against austerity and EU rules. A clear debt write-down would need to be avoided at all costs.

These payoff tables model our view of what the parties are calculating for their decisions. The numbers themselves are for illustration. Essentially, our analysis suggests that there is a large divergence in the perceptions of both sides but the rational choice is to hold to their respective positions. In other words, our analysis of the payoffs suggest that the EU won’t offer debt relief and Syriza won’t back down from demanding it.

Ramifications

Our fear is that the markets, inured by previous bailouts, expect the Greeks to cave. And, that may be the outcome. We view a Greek exit and market crisis as a low probability/high impact event. Such circumstances are difficult for markets to discount adequately because the bad outcome is considered so awful that the markets simply assume it can’t happen. We have tried to show in this report that rational behavior based on misperception can lead to bad outcomes.

We do fear that a Greek exit will have unexpected side effects that are not evident to policymakers. The fact that EU officials seem to believe that Greece can exit the Eurozone with minimal consequences is probably wrong. Even if the Bank of Greece implements capital controls to slow the outflow of deposits, the high level of corruption almost makes it certain that money will still flow out of the banking system, putting it at risk. At the same time, EU policymakers are assuming that contagion will not occur, which may not be accurate.

In general, we remain cautious of European investments at this time. If this situation is resolved in a “peaceful” manner, that caution would be lessened. But, until it is, the risk of an unexpected negative outcome in Europe is probably higher than what is currently being discounted.

Bill O’Grady

February 9, 2015

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[1] For a description of the divergence between populism and the establishment, see WGR, 1/12/2015, European Populism.

[2] The story is that two parties are arrested and questioned separately. If both remain quiet, they get a year in prison. If one rats and the other doesn’t, the quiet one gets 10 years and the other walks. If they both rat, each gets three years. Taken together, the best outcome is to remain quiet but it requires trust in the other player. To avoid the risk of a decade in prison, the rational choice is to rat out the other.

[3] The story here is also familiar. Two participants drive their cars at each other onto a single-lane bridge. If neither veers off at the entrance, both suffer certain destruction in a head-on collision. If one veers and the other doesn’t, that player is “chicken.”

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

(c) Confluence Investment Management

© Confluence Investment Management