Testing the Limits of Monetary Policy Without Fiscal Union

- Over the next 12 months, we expect eurozone growth to accelerate from the current annualised run rate of 0.5% to a still-very-weak pace of approximately 1%, while the ultra-low inflation tells us there is a demand problem.

- With the ECB set to expand its balance sheet over the cyclical horizon, the biggest risk to growth is if the ECB buys large quantities of government bonds but the governments do nothing.

- We expect to remain overweight European peripherals and overweight European corporate credit, with the focus on financials. We will look to underweight the long end of the core curve and will be underweight the euro currency versus the U.S. dollar.

In the following interview, Andrew Balls, CIO Global Fixed Income, and Managing Directors Andrew Bosomworth and Lorenzo Pagani discuss the conclusions from PIMCO’s quarterly Cyclical Forum in December 2014 and how they influence our European investment strategy. They also detail the impact of Europe’s economic health on the global economy.

Q: Growth among major economies is diverging. How long will this persist, and where will it lead?

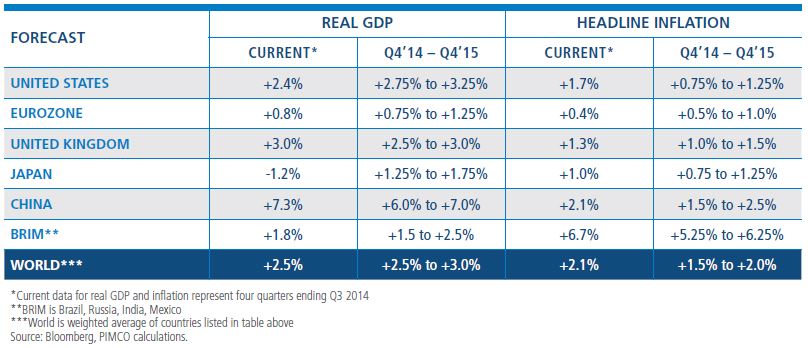

Balls: Over the cyclical horizon, we expect U.S. growth to be above potential and above consensus – and much stronger than that of the eurozone and Japan. In addition to this fundamental divergence in global growth, we expect a policy divergence: While the U.S. Federal Reserve (Fed) has ended quantitative easing (QE) and is set to tighten policy over the next year, the Bank of Japan (BOJ) has stepped up QE and we expect the European Central Bank (ECB) to broaden its asset purchases to include sovereign debt.

Looking at inflation, while headline rates are falling owing to lower energy prices, we see healthy underlying inflation in the U.S., in contrast to the eurozone, which is battling ultra-low inflation, and a mixed picture in Japan.

This divergence in developed economy fundamentals and policy is likely to endure for the next two to three years. This will provide relative value opportunities for active investors and, importantly, we expect the U.S. dollar to continue to appreciate, notably against the euro and the yen.

Q: What else would you add about Europe’s outlook for the next 12 months and how that might affect the global economy?

Balls: We expect the ECB's increasing balance sheet expansion, together with the BOJ’s expanded assets, to continue to provide support to global liquidity and global asset prices at a time when the Fed is gradually tightening policy. Similarly, were the ECB to disappoint on its quantitative easing intentions versus market expectations, we expect that it would be felt via the impact on global risk assets, not just the eurozone.

Weaker activity outside the U.S. reinforces our New Neutral expectations for the Fed policy cycle, via economic and financial market channels, notably the strengthening U.S. dollar. And in spite of such growing fundamental divergence, we expect the low level of German Bund yields to continue to provide some gravitational pull for U.S. and other global yield curves.

Q: How would you assess the ECB’s efforts thus far, and what is its likely next step?

Bosomworth: While the ECB has cut its policy rate all the way to the zero lower bound, inflation has consistently undershot the central bank’s forecasts, so something has occurred in the economy that the ECB’s models are not properly capturing. We suspect they are overlooking the extent to which labour markets have become more flexible and the extent of the output gap, which is notoriously difficult to quantify. Concerning the latter, for example, the private sector’s deleveraging in Europe has been relentless despite all the ECB’s efforts to boost the supply of credit. The inflation undershoot tells us there is a demand problem, too: Aggregate demand has fallen further below the potential supply, exerting downward pressure on prices and leading to the ECB’s response being too little, too late.

The special circumstances of a monetary union with 18 different sovereign states and no central, risk-free asset have complicated the ECB’s response. The ECB, in the meantime, has fired all its monetary shots except QE. We are at the point now where QE is the most likely next step.

We think the ECB will announce a QE programme of €500 billion to €1 trillion at either its January or March 2015 meeting. We expect a programme of this magnitude would be centered on government bonds, and we think the purchases would be broadly distributed across the member states in line with the ECB’s capital key (the percentages of its total capital that each national central bank contributes). There could be some divergence from the capital key reflecting the capitalisation value of different government bond markets. Non-financial corporate bonds are also likely to feature in the mix, but their share would be smaller relative to government bonds, reflecting the larger size of the government bond market in Europe.

Q: What would be the impact of full-blown quantitative easing for Europe? And what would such a move by the ECB communicate to markets?

Bosomworth: Broad-based QE would work through three channels: inflation expectations, borrowing costs and the exchange market.

QE, as described before, will send an important signal that the ECB is serious about achieving its inflation target – a signal that will help raise companies’ and households’ inflation expectations.

Purchases of non-financial corporate bonds would probably have a direct pass-through effect on the financing costs of those firms that have the ability to tap credit markets directly. And they could indirectly – through a trickle-down effect – lower loan costs for smaller firms. Purchases of government bonds would compress the risk-free curve further, thereby helping to lower the real expected rate of interest. We would also expect broad portfolio effects to materialise, with sellers of government bonds willing to reduce their excess holdings of cash by bidding up the price – and hence lowering the yield – of riskier assets further out on the concentric circles than those purchased by the ECB. For banks, for example, these portfolio effects might entail a shift out of government bonds into loan creation. This essentially works via banks’ opportunity cost of lending. Lowering the lending rate to governments will incentivise banks to lend to companies instead.

And by increasing the quantity of euros in circulation relative to other currencies, QE will likely lower the euro’s external value versus other currencies.

However, it is important to recognise the limits of QE: Sustainable, real growth ultimately derives from productivity and population growth. These are in the domain of the eurozone’s governments. In an ideal world, they would support the ECB in both the short and long term by allowing greater use of automatic stabilisers and by implementing reforms that enhance potential growth. We think markets will not be concerned about larger budget deficits as long as governments are underwriting structural reforms.

Ultimately the eurozone will likely have to move in the direction of political and fiscal union.

No other monetary union has endured without doing this. The biggest risk for investors, therefore, is if the ECB buys large quantities of government bonds but the governments do nothing. That would undermine all the ECB’s efforts to kick-start growth.

Q: How does PIMCO’s outlook vary from Europe’s core to its periphery?

Pagani: Over the next 12 months, we expect eurozone growth to accelerate from the current annualised run rate of 0.5% to a still-very-weak pace of approximately 1%. The sharp drop in oil prices, a weaker euro and increased ECB stimulus will likely add to growth in the coming quarters. However, ongoing deleveraging pressures and the need for structural reforms in the region mean that the acceleration in growth will be constrained.

There will be significant divergences in economic performance within the eurozone. Member countries that have done the heavy lifting, successfully undergoing fiscal and structural reforms, will perform relatively well – we expect Spain, in particular, to grow at a pace of approximately 1.75%. Countries, on the other hand, that still need to implement further reforms and cost adjustments will do poorly, such as Italy and France, where we see growth of approximately 0.25% and 0.5%, respectively. In Germany, we see economic growth of 1.5%; although better than the region’s average, growth is still subdued given a corporate sector that remains cautious and the lack of any significant fiscal stimulus.

At current levels, we believe eurozone growth will be too weak to meaningfully lift inflation and will therefore remain well below the ECB’s target of 2%. We see inflation at around 0.75% one year from now. Significant slack means that Spanish and Italian inflation will likely be barely above zero (we estimate 0.25%). Looking at the eurozone core, we also expect inflation to stay low in France (0.5%), given the required cost adjustments, and in Germany (1.25%), where the economic model is geared towards cost containment. Low inflation will remain a key hurdle for governments and the private sector in the eurozone to successfully deleverage their balance sheets.

Q: What is PIMCO’s outlook on the UK economy? What do you expect from the Bank of England?

Pagani: We expect UK growth to remain above trend over the next year, albeit at a slightly slower pace than the current 3% rate. Despite the weakness emanating from the eurozone, UK domestic demand remains strong, with both consumer and business confidence holding up well. In that context, we expect the unemployment rate to continue to fall and real wages to rise as the labour market tightens. Inflation is currently well below the Bank of England’s (BOE) 2% target, in part due to lower food and energy prices. In the short term, it is more likely than not that the headline consumer price index (CPI) will fall below 1% as the full effect of the recent commodity price moves takes hold. Thereafter, we expect headline CPI will converge towards core inflation of around 1.5%.

Given the benign inflationary backdrop, the BOE can afford to leave the policy rate at current levels of 0.5% until we have greater certainty over the rise in real wages and the global economic backdrop. The BOE will likely lag any rate move by the Fed, with UK policy tightening likely to commence in the second half of 2015.

Q: How will PIMCO’s outlook for European growth, inflation and central bank policy inform your investment strategies over the medium-term horizon?

Pagani: Given the low nominal growth in the eurozone, we expect the ECB will maintain a supportive monetary policy over the cyclical horizon that will result in a favorable environment for fixed income investors, characterised by stable positive returns. In an effort to profit from this stable environment, we remain overweight the seven- to 10-year maturities in core rates, while expressing an underweight in the long end of eurozone sovereign bonds where long maturity Bunds at approximately 1.50% are already pricing in a Japan-type scenario.

We expect the ECB to start its purchases of government bonds at the beginning of 2015 to lift inflation expectations. This would be supportive for spreads, especially in eurozone peripheral sovereign issuers, so we continue to maintain an overweight position in Italian and Spanish government bonds.

Looking at the UK, we favour a neutral duration in UK rates, as the yield curve already reflects a first rate hike by the BOE in the second half of 2015.

Importantly, while volatility should continue to remain subdued in general, we see the possibility of short periods of volatility spikes as we approach the start of the Fed tightening cycle, and we recognise the importance of available liquidity in portfolios to be able to profit actively from temporary market corrections.

|

|

All investments contain risk and may lose value. The strategy overview discussed herein is intended to illustrate major themes for the identified period. No representation is being made that any particular account, product or strategy will engage in all or any of the above themes. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2014, PIMCO.

© PIMCO