- The combination of fundamentals, technicals, valuations and global central bank policies drives our overall constructive outlook for global credit in 2015.

- Economic growth dynamics, including an improving outlook in the U.S., along with likely changes in global central bank policies, continued energy price volatility and the potential for more shareholder-friendly actions by companies inform our credit views and strategies.

- Specific sectors including U.S., European and Asian investment grade credit, high yield, bank loans, emerging market credit and municipal bonds may offer compelling opportunities. Bottom-up research remains crucial.

PIMCO remains constructive on the outlook for the global credit markets in the coming year given the combination of fundamentals, technicals, valuations and global central bank policies. Investors will need, however, significant global credit expertise in order to pick potential winners and losers given likely changes in global central bank policies and growth dynamics, continued energy price volatility and the potential for more shareholder-friendly actions by companies.

Fundamentally, developed market economic growth is supported by a gradual recovery in the private sector, improving bank balance sheets, the prospect for less fiscal restraint, an ongoing wealth effect, lower oil prices and accommodative central bank policies. Technically, the demand for high quality, income-producing assets continues to exceed the supply. Finally, valuations remain attractive for many credit assets given that the private sector, particularly in the U.S., continues to improve fundamentally and central banks are likely to remain accommodative due to low inflation, which should support the global economy and credit markets.

Within the global credit markets, specific sectors including U.S., European and Asian investment grade credit, high yield, bank loans, emerging market credit and municipal bonds may offer compelling opportunities in 2015. Bottom-up research is crucial, as always.

Investment grade U.S. credit

The outlook for the U.S. investment grade (IG) credit market remains stable to improving. From a fundamental standpoint, the improving U.S. growth outlook is supportive for U.S. credit: PIMCO expects roughly 3% real GDP growth for the U.S. over the next 12 months. While growth is picking up, the outlook is not strong enough yet to meaningfully alter the Federal Reserve’s accommodative monetary policy; we expect only gradual interest rate increases next year given low inflation globally.

On the technical front, inflows in IG credit remain strong from retail investors as well as from non-U.S. investors looking for a high quality, less volatile asset class with steady income. Additionally, with modest rate rises anticipated next year, higher yields would improve demand from yield-driven investors like insurance companies and pension funds, further supporting IG credit spreads. Finally, broad U.S. IG credit valuations look fair at current levels when compared with the long-term average but attractive when compared with high quality credit in other developed regions.

With this favorable to improving outlook for U.S. IG credit, sector and security selection will be key to generating incremental returns. Financial conditions remain such that it is increasingly easy for corporates to issue debt and raise leverage, thereby potentially reducing expected returns for bondholders. Credit selection should focus on companies that not only are expected to show strong growth, have high barriers to entry and enjoy pricing power but are also using their earnings growth to delever instead of increase leverage. Sectors that look attractive based on these criteria include banks and financials, healthcare, building materials, airlines, lodging, gaming, autos and cable.

Investment grade European credit

The outlook for European IG credit remains supportive going into 2015. The European Central Bank (ECB) should stay very accommodative; European rates will likely be at zero for the foreseeable future, anchoring European duration and generating strong demand for credit and higher income. The ECB has finally embraced quantitative easing: Purchase programs of covered bonds and asset-backed securities are already underway, and as European inflation remains stubbornly low, we expect that the ECB will further expand its balance sheet by buying euro-denominated IG corporate and sovereign bonds.

Those purchases will be supportive for European assets. In anticipation, euro-denominated IG corporates have outperformed U.S. credit by 20 basis points (bps) in the past two months (source: Bank of America Merrill Lynch (BAML) Euro Corporate and US Corporate indexes – change in option-adjusted spreads versus LIBOR from 30 September 2014 to 30 November 2014). Although valuations are already tight, limiting potential spread compression to 10 bps–20 bps, credit curves remain relatively steep in the five- to 10-year sector, offering some opportunity for carry and roll-down. Both European fundamentals and technicals remain supportive; the lack of growth in the eurozone is limiting corporate releveraging despite low absolute yields, while net supply is unable to meet the growing investor demand for high quality credit.

Within European credit, the banking sector continues to offer some of the best opportunities now, given the continued deleveraging trend encouraged by regulators. We favor the subordinated part of the capital structure in the strongest banks with mid-single-digit yields. We also expect peripheral country bank spreads to tighten as they will be able to refinance their upcoming maturities at the ECB for four years at 15 bps. In the corporate sector, we favor rising stars – companies that we expect will be upgraded in the next 12 to 18 months – as well as euro investment grade corporate hybrid bonds, with high quality utilities or telecom companies offering LIBOR + 200 bps–250 bps.

Investment grade Asian credit

For Asian credit, investment grade fundamentals remain generally positive, but sector selection will continue to be key. Structural excess supply and slowing Chinese demand have been creating headwinds for iron ore and coal prices, directly affecting the expected free cash flows of some Australian mining companies. Conversely, ongoing re-regulation in banking will continue to provide more capital support for Japanese and Australian banks.

From a policy perspective, the Bank of Japan has recently announced even more quantitative easing, and the recent election affirmed an overall re-commitment to Abenomics. The Reserve Bank of Australia (RBA) has indicated a period of ongoing stability in policy rates at the current moderately stimulative level of 2.5%. These accommodative policy settings are expected to support current credit valuations.

Within the Asia-Pac investment grade sector, we anticipate significant opportunities in Basel III Tier 2 issues from major/mega banks and life insurers in both Japan and Australia. The structure of Basel III notes issued by Japanese mega banks is very credit investor friendly: Negative net worth will be a credit trigger and pre-emptive capital injection will not result in principal losses. In addition, subordinated notes from the Japanese life insurance sector will directly benefit from the asset reflation theme in Japan, presenting unique opportunities with limited supply risk. Also, Australian major bank Basel III Tier 2 issues will be technically supported as their capital effectiveness dissipates, and we expect these securities to be called at the earliest opportunity. Finally, yen-denominated credit is typically expensive in global relative value terms, so we strongly prefer buying Japanese issuers in other currencies to be sufficiently compensated for credit risk.

High yield

Global high yield (HY) markets have seen spreads widen and yields move higher this year against a backdrop of retail outflows and energy-sector-related volatility. While high valuations were a major driver, especially at the onset of market volatility in late June, technical factors, such as unpredictable fund flows and imbalanced supply and demand, have dominated high yield performance. Adding to the mix is the selloff in energy exploration and production and cyclical oilfield services issuers, which now constitute approximately 8% of the global HY market. Nonetheless, the global HY market has managed to deliver a 2.5% return for the year as of early December, largely on the back of outperformance in more interest-rate-sensitive (and relatively higher-quality) BB companies. (Source for all data is the BAML Developed Markets HY Constrained Index as of 11 December 2014.)

While the HY market has been on a roller coaster ride of volatile prices and yields, fundamentals have improved slightly, especially in the U.S. Earnings for U.S. high yield companies grew at a strong pace of 12.4% year-over-year through the end of the third quarter, based on results from nearly three-quarters of all publicly reporting high yield issuers (source: BAML). Nearly all industry categories registered positive year-over-year growth in EBITDA (earnings before interest, taxes, depreciation and amortization), while leverage declined and margins held up at a healthy 27.9% as of 30 September 2014, according to BAML. High yield companies continue to benefit from elevated equity cushions as enterprise valuation multiples have expanded. And while mergers and acquisitions (M&A) activity picked up in 2014, leveraged buyouts as a percentage of total M&A volume were only 6%, well below the peak of 18% in 2006. Consequently, BB rated credits now represent 45% of the high yield market today, compared with 38% in December 2007 (source: BAML US HY and BB US HY indexes as of 30 November 2014). Albeit more of a backward-looking indicator of fundamentals, the annual default rate at 2.2% (as of 30 September 2014) remains less than half its historical average. HY issuers have been proactive in terming out maturities over the past five years, so that only a relatively small amount of bonds will mature over the next two to three years. That said, there are pockets of stress in the market, most notably among credits that are directly exposed to price volatility in commodities such as coal, iron ore, oil and natural gas.

Going forward, we expect high yield performance will continue to be dominated by coupon income. However, with average prices just above $98 (source: BAML US HY Index), a buyer in the high yield market has potential for capital appreciation as well, if – as PIMCO believes – U.S. Treasuries remain range-bound and defaults do not pick up materially outside certain pockets of weakness in energy. Regionally, we see the best opportunities in the U.S. where growth prospects are better than in Europe. The higher absolute yields in the U.S. (6.84%) versus Europe (4.11%) (source: BAML US HY and Euro HY Constrained indexes) also offer more total return potential as well as a better cushion to absorb a potential rate increase should that play out gradually in the U.S. even as Europe embarks on a path of prolonged stimulus. (All data is as of 11 December 2014.)

Whether in the U.S. or Europe, HY credit research and security selection remain paramount – for instance, picking the winners and avoiding the losers from the sectors exposed to commodity price volatility will be among the most important factors driving performance in 2015.

Bank loans

In the U.S. bank loan market, we expect 2015 to continue on the path of 2014, with strong credit fundamentals driving steady performance. After another year of active issuance, including a continuation of the refinancing and maturity extension trend we have seen for the last several years, issuers in the loan market have generally improved balance sheets, and with strong earnings supported by a prolonged low rate environment, we see the fundamentals remaining strong as we enter 2015. With this backdrop of strong earnings and limited maturities, defaults are expected to remain low in 2015, with most forecasts at just 2%–2.5%, well below the long-term average.

From a technical perspective, the largest risk is on the demand side; steady but moderate retail outflows persisted throughout 2014 although they were offset by a robust collateralized loan obligation (CLO) market. In 2014 to date, CLO issuance marked a record at over $120 billion, which more than offset the $15 billion outflow from retail funds. Heading into 2015, demand could shift in both areas. In CLOs, the new risk retention rules, which require managers to buy and hold a 5% share of any CLO they manage, are expected to reduce CLO issuance when implemented, but that is still two years out. So in 2015, we would expect to see continued healthy CLO issuance, as managers seek to grow assets ahead of the risk retention rules implementation. Wall Street forecasts for CLO issuance in 2015 now range from $50 billion–$70 billion.

The retail outflows in 2014 seemed to be driven by the expectation that rates would not rise in the near term, which made owning a floating rate fund less attractive for many investors. As we enter 2015, however, market expectations of Fed policy point to a rate rise as soon as mid-2015, so we could see renewed interest in floating rate funds and separate accounts as well.

Given this expected strong demand for loan assets across CLO, retail, and institutional investors, along with a steady fundamental picture, we should see an active new issue market in 2015. M&A-driven financing is already teed up to open the year with a strong new issue calendar. Market estimates for gross loan issuance in 2015 remain elevated, though it is likely to fall short of the $440 billion in 2014 through early December. This year about half of issuance was refinancing related. In our view, while issuance should remain strong in 2015, we could see a reduction in opportunistic refinancings as underwriters remain pressured by the regulatory agencies to meet leveraged lending guidelines.

With strong fundamentals and loan demand that will likely outpace natural supply, valuations are likely to improve, as we have seen since the October market correction. On a relative basis, loans remain attractive compared with HY, as the loan market currently offers similar yield but benefits not only from seniority and collateral protection, but lacks the duration risk which could challenge valuations in other fixed income credit markets in 2015. For investors seeking income potential in credit, we expect the loan market to deliver another fairly steady year, supported by strong credit fundamentals, low defaults and steady demand, with a downside hedge in the event of a worsening economic environment, and some upside potential if 2015 is indeed the year the Fed acts to move rates higher.

Emerging market credit

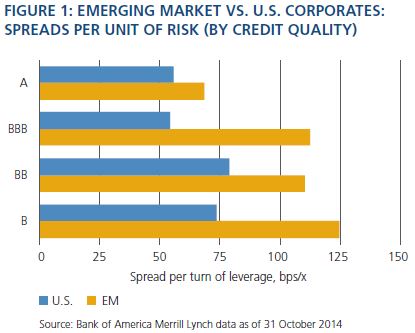

The outlook for emerging market (EM) credit could be volatile given weak commodity/oil prices and investor anxiety over the beginning of what will likely be gradual Fed tightening as the FOMC exits zero interest rates. These near-term “headwinds” are offset by secular “tailwinds” in that emerging markets is an underinvested asset class with compelling credit metrics and should continue to draw investors’ attention. Despite the general fear of a slowdown in global growth, emerging markets as a whole are still growing at twice the speed of the developed markets (expected growth of 4.5% versus 2.2% for 2015) and that, in turn, has created a $1.6 trillion asset class (currently larger than the U.S. high yield market) that is still growing at 15%–20% per annum (source: BAML). The fact that this now sizeable asset class still offers incremental spread pickup for similar credit risk has created a far more stable EM asset class with far better investor sponsorship than in the past. Once we control for credit ratings, emerging market corporates offer more spread per unit of risk (leverage); in the case of the BBB rated segment, EM offers more than twice the spread compensation for the same risk (see Figure 1).

We anticipate new investors will enter the asset class in 2015 given the compelling valuations and solid fundamentals, and existing investors will expand their net EM exposure. Indeed, in 2014 we witnessed a new portfolio rebalancing trend, whereby existing EM investors moved from other segments of the asset class, such as sovereign, local rates and currencies, into EM corporate credit rather than exiting the entire sector as they have during volatile periods in the past. In addition, the previously dominant EM sovereign market continues to shrink (currently half the size of the EM corporate market), which should add to the technical support for EM corporate credit.

With 2015 developed market growth likely to be largely driven by a U.S.-led recovery, and with modest U.S. rate increases expected to follow, the spread cushion and generally shorter duration in EM credit versus U.S. IG credit should further underpin this sector’s outperformance potential. We see pockets of value in Brazil, Russia and China, where current developments favor globally dominant, highly competitive credits with healthy balance sheets. Specifically, we continue to see value in IG/HY Asian and Latin American select sectors such as TMT, export-oriented industrials and gaming.

In Brazil, the recent re-election of President Dilma Rousseff and general investor ambivalence about the direction of the current administration have created opportunities in various sectors. The corruption investigation at Petrobras has only added to this broad shopping list, and we continue to look at credits within the oil and gas sector that have seen unwarranted spread widening.

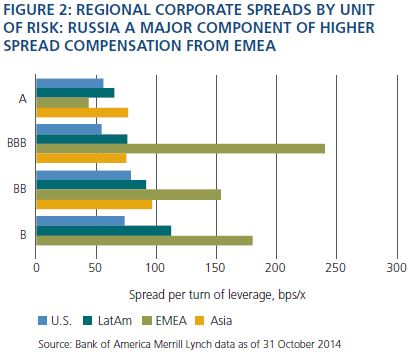

In Russia, spreads now reflect not only a simple estimation of credit risk but also the larger geopolitical risk in these largely sanction-able names. Credits in Russia currently offer 4x–5x the spread compensation of U.S. IG names for the same amount of credit risk, suggesting that Russia could be an interesting opportunity in 2015 (see Figure 2). High quality, best-in-class Russian BBB rated corporate spreads are currently at 500 bps on average, some 40 bps wider than the average spread on U.S. single B rated credits. (For reference, Russia BBB rated corporates have strong credit metrics, with leverage of 1.3x on average versus 5.1x for U.S. single B rated names).

We expect Russia, China and Brazil to be the key drivers of EM corporate credit performance for 2015, but it bears remembering that the investment opportunity is in the growth of this asset class as a whole.

Municipal bonds

The outlook for municipal investment grade credit remains positive due to stable to improving credit fundamentals, a supportive technical backdrop and accommodative central bank policy. However, valuations in the front end of the curve are less attractive than they were at the start of 2014, as evidenced by tight credit spreads and muni/Treasury ratios, which look expensive on a five-year historical basis.

Fundamentally, credit quality across state and local municipalities continues to improve despite a pickup in high-profile bankruptcies in recent years. We are disappointed by the outcomes in the Stockton (California) and Detroit bankruptcies as municipal bondholders received less favorable treatment relative to unfunded pensions. The ultimate recovery on Detroit’s unlimited tax general obligation (GO) bondholders will be lower than the historical average for municipal GOs, with approximately 26% of the dedicated property tax levy diverted to the city’s pensions.

For the 50 states, credit quality continues to improve; governments are adding to payrolls modestly and many states are rebuilding reserves. A few high profile states continue to exhibit deteriorating credit trends, primarily due to lingering debt overhangs, pension and other post-retirement burdens, tepid revenue growth and stubbornly high unemployment.

Local government credit quality is also improving overall, but the recovery is more uneven and slower in general than the states’. Local governments typically rely on property tax revenues based on housing. Tax assessments generally lag the broader housing market by 18 to 36 months, and many metropolitan areas are still in the early stage of a housing recovery. Local governments in some regions are also contending with large unfunded retirement obligations and have less revenue flexibility versus the states. Overall, we expect default rates in line with historical data (the Moody’s five-year cumulative default rate for all municipal borrowers from 1970–2013 is 0.07% versus 7.55% for corporates), and we expect the frequency of Chapter 9 filings to normalize from recent years.

The technical backdrop has been very supportive of the municipal market in 2014. Gross issuance was down a modest 4.6% through early December; however, net negative supply was expected to be about $35 billion for 2014. At the same time, the asset class saw more than $17 billion in positive inflows, primarily into long duration and high yield muni funds. This supply/demand imbalance resulted in strong returns for municipals. Looking forward, new issue supply may increase modestly as low interest rates continue to accommodate refunding opportunities and municipalities gradually increase new money issuance for infrastructure and additions to capital stock.

Municipal valuations generally appear high due to the improvements in credit fundamentals and the supply/demand imbalance. The short to intermediate part of the yield curve looks considerably rich, with the five-year muni/Treasury ratio at 76%. The 30-year muni/Treasury ratio looks more attractive at 102%, but we maintain a duration underweight in all of our municipal portfolios (data is as of 10 December 2014). As the Fed normalizes monetary policy, municipals may be susceptible to a rise in interest rates when credit spreads are also at tight levels. Within municipal investment grade credit, we still find opportunity today in revenue bonds issued by municipalities that exhibit strong growth characteristics and select local GO credits in regions where the U.S. recovery is stronger and population growth is healthy.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. Collateralized Loan Obligations (CLOs) may involve a high degree of risk and are intended for sale to qualified investors only. Investors may lose some or all of the investment and there may be periods where no cash flow distributions are received. CLOs are exposed to risks such as credit, default, liquidity, management, volatility, interest rate and credit risk. Derivativesmay involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included. Investors should consult their investment professional prior to making an investment decision. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2014, PIMCO.

© PIMCO