Is the Oil Price Slump an Early Holiday Gift for Some Consumers?

With 60% of global GDP driven by consumers, the impact that sustained lower oil prices will have on the global economy is an important factor for investors to take into account.

The benefits of lower oil prices will not be evenly distributed and it is important to think about countries that stand to benefit more because of higher consumption and/or less economic dependence on oil exports.

We are relatively positive on consumer discretionary companies including automobiles and components, durables and apparel, hotels, restaurants and leisure companies as well as media and general retailing. Companies in the industrial sector, such as capital goods, transportation and commercial services and supplies companies, stand to benefit from lower input costs that will support profit margins.

Oil prices have fallen by over $40 a barrel in recent months as increasing production in the U.S., a decelerating global economy and an OPEC decision to protect market share have combined to create a perfect storm for the commodity. But while that poses some challenges for the industry, it will likely be a boon for many consumers around the world as it translates into more disposable income, and like consumers, sectors and companies that cater to those consumers should benefit.

That said, this bonanza will not be evenly distributed and it is important to think about countries that stand to benefit more because of higher consumption and/or less economic dependence on oil exports. Higher GDP growth and lower inflation are key transmission mechanisms.

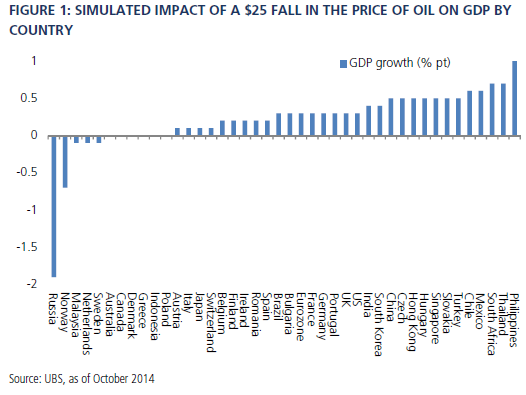

In terms of trade, the losers are oil exporters, including Norway, for whom commodity exports are some 20% of GDP, and Russia. On the other hand Korea, China, Japan, India and Thailand are net oil importers and will benefit from the sharply lower prices. In South Africa, Thailand and the Philippines, the impact of a $25 per barrel drop in the price of oil translates to half to one percentage point of GDP growth. Even in the U.S. a $25 per barrel price decline roughly translates into a quarter of a percent of GDP growth – not an insignificant number given the size of the economy.

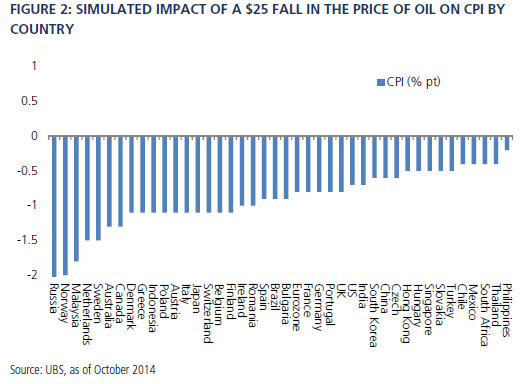

As for consumers, the weight of energy in the CPI is an important factor as it reflects the share of consumer incomes spent on fuel. Lower oil prices affect CPI in all countries, but the impact is likely to be smaller in those economies with a lower energy CPI weight such as Hong Kong and Singapore.

In addition, a different but important measure of how oil prices pass through to consumers is the prevalence of subsidies and the tax treatment of fuel: The higher the rate, of course, the less the price of oil matters. In low tax countries like the U.S. and Canada, the impact is proportionally greater since the cost of oil represents a larger portion of the price at the pump. The opposite is true in places where petrol taxes are high, such as Turkey, the Netherlands and the UK.

For some countries, a combination of a high energy CPI weight and limited taxation should mean a larger boost to disposable incomes. For instance, the U.S., Spain and Greece stand to benefit because energy is a large contributor to CPI and the correlation of energy CPI to the oil price is relatively high. By contrast, countries like Singapore benefit less because oil taxation is higher, limiting the benefit of lower oil prices. Also, energy is not a significant contributor to CPI.

In the U.S., the proportion of disposable income spent on non-discretionary items such as mortgages, food and energy is at its lowest level in at least 35 years. Since the financial crisis, aided by lower interest rates, consumers have been deleveraging. Now, lower oil prices should provide another boost to consumer incomes by reducing energy costs.

Generally, consumer companies should benefit. We are relatively positive on consumer discretionary companies including automobiles and components, durables and apparel, hotels, restaurants and leisure companies as well as media and general retailing. Companies in the industrial sector, such as capital goods, transportation and commercial services and supplies companies, stand to benefit from lower input costs that will support profit margins.

Asian consumers stand to benefit most as the region is a large importer of oil. Singapore, Hong Kong, Korea, Taiwan and Thailand are the largest importers. Hence, lower oil prices translate into better terms of trade, lower fiscal burdens and better inflation trajectories for Asian countries. In Asia, the consumer discretionary sector looks well positioned both from a commodity angle and supportive valuations. This includes areas like autos, electronic goods and travel.

In countries where the debt burden on the household is high, Korea for example, a lower interest rate environment remains supportive. In fact, Korea is likely to have another rate cut. This is likely to help consumers to further manage their interest burden. Now a lower energy burden for consumers is the icing on the cake.

With 60% of global GDP driven by consumers, the impact that sustained lower oil prices will have on the global economy is an important factor for investors to take into account. PIMCO’s secular outlook, The New Neutral, is one where growth and inflation both remain tame and command lower real interest rates than previously seen. Changes in demand and supply in the energy markets, including shale, combined with the increasing impact of energy efficiency, commitments to higher renewable shares given climate change issues all point to a favorable contribution of oil to GDP growth via the consumer for 2015.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world. ©2014, PIMCO.

© PIMCO