Reflections on the 25th Anniversary of the Fall of the Berlin Wall: Part 2

Last week, we began our two-part series on the fall of the Berlin Wall with an examination of the end of Marxism. In this report, we will examine the rest of the important consequences from the fall of the Berlin Wall. These are:

- The Collapse of the U.S.S.R.

- The Onset of the U.S. Unipolar Moment

- The Impact of German Unification

We will conclude our comments with potential market ramifications.

The Collapse of the U.S.S.R.

In 1946, George Kennan, a U.S. diplomat in the Soviet Union, penned his famous “long telegram” to the State Department in Washington. This telegram became the basis of U.S. policy toward the U.S.S.R. until it dissolved in 1991.

Kennan became convinced that the Soviets would never coexist with the West. He also determined that an all-out war with the U.S.S.R. was probably either unwinnable or too costly. Kennan concluded the Soviets would constantly try to expand their territory and would always be pressing for advantage. Kennan’s solution was containment. He was convinced that capitalism and democracy was a system superior to communism and totalitarianism, and if the U.S. simply waited it out, the U.S.S.R. would eventually collapse.

When a nation has nuclear weapons and a way of delivering them, forcing unconditional surrender would likely elicit a nuclear response to prevent such surrender from taking place. Thus, once the Soviets acquired nuclear weapons and delivery systems, full scale war with unconditional surrender became impossible.

Kennan’s plan worked, and a number of “containment wars” did occur in Korea and Vietnam. The U.S. supported jihadists that eventually defeated the Soviets in Afghanistan but at the cost of “blowback” that culminated in the attacks of 9/11. Still, as economic growth diverged between the Soviet Union and the U.S., it became increasingly obvious that communism as an organizing principle for economies was a dismal failure. After the Berlin Wall fell in 1989 and the Eastern Bloc began to spin out of the Soviet Union’s orbit, the collapse accelerated. By late 1991, various “republics” within the Soviet Union had left and the country ceased to exist; what remained was Russia.

The U.S. and the West celebrated its victory over the U.S.S.R. and, for the most part, ignored Russia’s concerns. Boris Yeltsin, the Russian president, was initially effective, but succumbed to excessive drinking. The country tried to use “shock therapy” to restructure its economy, rapidly privatizing businesses. However, this led to a few crafty and well-connected operators gaining control of industries at dramatically reduced prices.

This situation led to the creation of the “oligarchs,” who controlled the formerly state-owned businesses. The economy fell into a deep depression which culminated in a debt default near the end of the 1990s. Conditions became so bad that the life expectancy for Russian men fell during this period, one of the few times in recorded history when life expectancy declined outside of war or pandemic. Perhaps the clearest sign of Russia’s declining influence was the Kosovo conflict. Russia had supported Serbia for years; in fact, Tsarist support for Serbia was one of the factors that led to WWI. Russia opposed Kosovo’s separatist movement and supported Serbian efforts to keep Kosovo as part of Serbia. The Clinton administration and NATO, horrified by genocide in the region, bypassed the U.N. (where Russia still carried a veto) and, under NATO auspices, ran an air campaign against Serbia. U.S. and European behavior signaled to Russia that it was weak and its concerns would not be considered.

At the end of 1999, Boris Yeltsin’s period in office ended and Vladimir Putin became president. He immediately moved to stabilize the political and economic situation. The steady rise in oil prices supported Russia’s economic recovery. Putin began to reduce the power of the oligarchs, exiling or arresting those who opposed him. Putin ended the practice of regions voting for their own governors, instead appointing them from the Kremlin. He viciously put down the rebellion in Chechnya, generally putting an end to worries that additional areas of Russia would secede.

From Putin’s perspective, the West was still trying to undermine Russia. The Rose and Orange Revolutions in Georgia and Ukraine, respectively, were of deep concern to Putin. Whereas the Bush administration characterized these events as indigenous democratic movements designed to create more responsive and responsible governments, Russia viewed these color revolutions as U.S.-intelligence orchestrated efforts to create hostile governments in Russia’s sphere of influence.

Putin became increasingly unfriendly toward Georgia and Ukraine. Russia cut off natural gas flows to Ukraine on numerous occasions. The first disruption came in the winter of 2006, shortly after the Orange Revolution. Others occurred in the spring of 2008 and the winter of 2009.[1] And, this year, open warfare erupted between Russia and Ukraine with the former annexing the Crimea. In Georgia, Russian troops invaded in the summer of 2008, supporting the regions in Georgia that had difficult relations with Tbilisi.

Since 2005, Russia has been clearly opposing independent policy actions by its neighbors. It has become obvious that Russia is trying to resume its influence in its “near abroad.”

Western policymakers failed to consider Russia’s geopolitical situation. Russia lacks significant geographic obstacles to invasion. As history shows, its most effective means of protection is to extend its borders (or increase Russia’s influence, at a minimum) as far as possible and force invaders to extend supply lines to reach Moscow. On two occasions (Napoleon and Hitler), winter ravaged the invaders and allowed the country to repel the invasion. Thus, Russia has a natural desire to expand as far as possible.

Unfortunately, the areas Russia subjugates in this process tend to resent Russian rule. Over time, Russia struggles to control these areas and, eventually, loses them. Moscow then retreats, regroups and restarts the process. American policymakers failed to understand that, at some point, Russia was bound to try to expand again. The fall of the Soviet Union masked the fact that Russia is still going to behave as it has for centuries. Thus, the idea that a new “Cold War” is developing is probably wrong. Russia isn’t the vanguard of an alternative vision for human society. Instead, it is more likely to try to expand into its surrounding areas based on historic geopolitical conditions. That doesn’t mean Russia isn’t a threat; however, it is more of a threat to the Baltics than it is to Vietnam, which the Soviets supported in the 1960s.

The U.S. Unipolar Moment

After the fall of the Berlin Wall and the end of communism, the U.S. became the world’s only superpower. This was a heady situation. America, after having faced down the communist menace from 1945 to 1991, suddenly faced no existential threats.

Although a great cause for celebration, it has become clear that U.S. policymakers have been adrift since the Cold War ended. During the Cold War, due to the penetrating insights of George Kennan and others, the U.S. had a foreign policy paradigm that was maintained until the Soviet Union fell. Unfortunately, since the fall of the Berlin Wall, no new paradigms for foreign policy have emerged. Instead, the U.S. has fallen into two competing paradigms. The first is a Wilsonian policy construct that has led to democracy promotion, inconclusive and probably unnecessary conflicts, and situations in which military intervention has probably made conditions worse. The second is isolationism, which is promoted by the populist classes on both the right and left wings who have been steadily opposing U.S. military actions and are opposing free trade and the dollar’s reserve currency role.

The populists represent the less affluent; as we described in Part 1, this group tends to be tied to place with less resources to cope with the vicissitudes of fate. From their perspective, the superpower role is simply a cost. They face wage pressure from free trade and outsourcing. They or their children are often in the military, fighting the proxy wars in which the superpower is engaged. For the capitalists, the globalization that the superpower role fosters allows them to leverage their talents on a global scale. Thus, they support the superpower role which benefits their global perspective.

No superpower reigns forever. Unfortunately, history does show that the periods between superpowers tend to be dangerous. Before Britain took the role from the Dutch in the late 1700s, we had the French and American Revolutions and the rise of Napoleon. When the British were losing their grip and the U.S. wasn’t prepared to accept the role, we had two world wars and a Great Depression. Overall, giving up the role isn’t something the U.S. should do lightly. Unfortunately, it may occur that the U.S. ends the role without even being conscious of the benefits and costs that come with the role, or the ramifications that could occur from ending or maintaining the position.

German Unification

Germany became a country in 1871 after Prussia and Otto von Bismarck unified various duchies and regions to create the state. Germany’s geopolitics were problematic from the start. The country is positioned in the center of Europe with no significant geographic barriers from an external enemy. The lack of geographic barriers and its positon in central Europe strongly supported its economic development. At the same time, it also made it vulnerable to invasions from both the east and west. This situation became known as “the German Problem.” As Henry Kissinger notes, “Germany is too big for Europe and too small for the world.”

From 1871 until 1945, German military doctrine was based on managing a two-front war. In WWI, Germany tried to quickly attack France and end its participation so it could concentrate on attacking Russia. When France stopped German advances at the First Battle of the Marne River, WWI settled into the dreaded two-front war.[2]

In WWII, Germany signed the Molotov-Ribbentrop pact with the Soviet Union. This non-aggression pact divided Poland between the U.S.S.R. and Germany and allowed the Nazis to focus their attack on Western Europe without having to open an eastern front. Some historians speculate that Stalin assumed that Germany would become bogged down in France like it did in WWI. Instead, German troops overran France and quickly controlled Western Europe. Hitler violated the pact in June 1941 by attacking the Soviet Union.

After WWII, the allies tried to come up with a way to prevent the German Problem from fostering a third world war in Europe. While trying to manage the situation, the four allies, the U.S, U.S.S.R., U.K. and France were all granted zones of Germany to control. Initially, there were plans to end the occupation with a unified Germany. However, as it became apparent that Stalin was not going to allow a single Germany to exist that wasn’t communist, the nation was divided into West and East Germany, with the former being comprised of the sectors controlled by France, the U.S. and U.K. and the latter by the Soviet zone.

As a divided nation, the German problem was essentially solved. The German military was emasculated; the country was protected by NATO (which mostly meant the U.S.) with its foreign policy controlled by the European Union. Under these constraints, Germany focused on rebuilding its economy; on the back of American consumption, Germany built a formidable export economy.

When the Berlin Wall fell and East Germany officially joined West Germany in March 1990, the German problem returned. Initially, U.K. PM Thatcher opposed unification, referring to WWII. France was cool to the idea as well. To make the unification more palatable, Germany agreed to give up its beloved Deutsche mark for a currency of Europe, the euro. France believed that this move would make Germany more integrated into Europe and less likely to dominate it.

Unfortunately, this idea was in error. The German economy has come to dominate the Eurozone, forcing austerity across the single currency. Germany has been essentially dictating bailout terms to troubled nations in the region; needless to say, these countries are coming to resent Germany’s behavior.

Essentially, the German problem has returned. So far, Germany has not rearmed, although expanding its military would not be difficult. It has an educated population, a deep industrial base, an already impressive defense industry and a strong enough economy to expand defense spending. If Russia continues its expansion into Eastern Europe and the U.S. continues to withdraw from the superpower role, Germany may have no choice but to evolve into a regional hegemon. Given the history of Germany since 1871, such a development is bound to increase concerns.

Ramifications

When communism fell, a famous debate emerged from the academic community between Francis Fukuyama and Samuel Huntington. Fukuyama argued that the end of communism was the end of the debate; there was no other alternative to capitalism and democracy for development. Thus, the world would certainly become a more stable place with all nations operating under similar systems. Huntington argued that this would not be the case. Instead, he worried that all sorts of frozen conflicts that had been subsumed under the mantle of communism versus capitalism would now emerge. Initially, it appeared that Fukuyama was correct. However, events since 9/11 suggest that Huntington is probably correct.

What does that mean for markets? Arguably, the end of the Cold War probably contributed to the sharp improvement in sentiment that lifted financial markets.

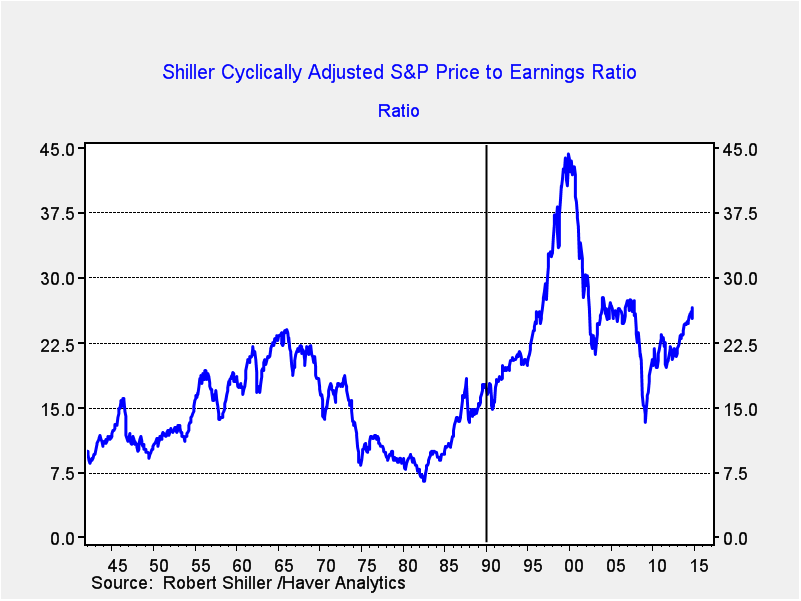

This chart shows the Shiller cyclically-adjusted P/E ratio. We have placed a vertical line when the Berlin Wall fell; note that the P/E steadily rose to unsustainable levels. Although there were other factors that boosted equity values, the fact that the U.S. won what may be the most important war of the past century was bound to lift confidence. Perhaps 9/11 and concerns about how the world will evolve is partly to blame for the drop in sentiment as well.

There is no doubt that the end of communism was a very positive development. However, this isn’t to say that there were not consequences that followed that have been surprisingly difficult. In no way would we want to return to the Cold War. However, in retrospect, a better appreciation of the challenges that followed would have been helpful.

The uncertainty surrounding Germany, Russia and the U.S. will affect financial markets. Unfortunately, history can only offer vague patterns of what we may be coping with in the next several years. In general, if the U.S. does abandon the superpower role, foreign investing will become more difficult, commodity prices will likely rise and the U.S. will probably become the global safe haven for frightened capital. Thus, the globalization that the world has enjoyed over the past 35 years may be threatened. We continue to monitor these developments closely.

Bill O’Grady

November 24, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[1] The recent conflict in Ukraine has led to yet another disruption of flows; there is an agreement in place for gas to flow, but given rising hostilities it is unclear whether the agreement will be honored.

[2] One interesting development was that Germany sent Lenin in a sealed train car to Moscow along with some $10 mm in gold in February 1917 with the idea that Lenin would start a revolution that would end Russia’s participation in WWI. The plan worked. Russia did leave the war after the October 1917 revolution. The Treaty of Brest-LItovsk in March 1918 ended Russia’s participation on very favorable terms to Germany. Most of Germany’s gains from the treaty were lost to Russia over the next few years.

© Confluence Investment Management