Since the initial Greek financial crisis in 2010, economic and financial problems in the Eurozone continue to periodically emerge. The most recent issue is that the Eurozone may soon face deflation; price levels continue to decline. The current yearly CPI is up a mere 0.3%. Although the Eurozone did experience a bout of deflation in 2009 in the aftermath of the Great Financial Crisis, the current flirtation with deflation is due to weak growth in the Eurozone.

Traditional Keynesian prescriptions for deflation include expanded fiscal spending and accommodative monetary policy. However, there is no unified fiscal policy in the Eurozone, and the European Central Bank (ECB) has an unclear mandate to execute unconventional monetary stimulus measures. Complicating matters significantly is German opposition to both fiscal and monetary stimulus measures.

Germany’s opposition to reflation policies are usually attributed to simple national interests (Germany is a creditor nation and benefits from deflation) or due to the lingering effects of the post-WWI hyperinflation. However, we believe that a more careful examination of the historical record suggests that the experience after WWII and the Wirtschaftswunder (economic miracle) that lasted into the early 1960s has played a larger role in shaping current German policy.

This week we discuss German history from 1946 into the late 1950s with a focus on how German leaders shaped the economy and rebuilt the nation after the war. We will pay particular attention to the economic model that German leaders constructed and show how the Merkel government is trying to impose that model on the entire Eurozone. As always, we will conclude with market ramifications.

Post-WWII

After Germany’s surrender in 1945, the country was divided into four zones controlled by the major victorious powers, the U.S., U.S.S.R., U.K, and France. Initially, the plan was to reunify Germany. All of the victors wanted to ensure that Germany would not threaten Europe again but disagreed on how best to accomplish that goal. The Soviets wanted to create a communist state; the U.S. was not sure what it wanted. Initially, the Morgenthau Plan was designed to return Germany to its “pastoral” roots by deindustrializing the country. That idea was quickly jettisoned but no clear plan emerged from the Americans. The U.K. and France were mostly following the lead of the Truman administration, although both wanted some type of reparations.

As the occupation wore on, it was becoming apparent that the Soviets were going to oppose any sort of Western-style democracy for a unified Germany. The U.S., U.K, and France would either have to abandon the

Germans to the tender mercies of the Soviets or refuse unification. Although the decision wasn’t completely settled until 1950, the U.S. was generally preparing for a divided Germany. During this period, the U.S. and U.K. decided to jointly manage their zones in Germany, setting the stage for the creation of West Germany.

During WWII, Hitler funded the war effort through deficit spending and debt monetization. Normally, such policies would lead to inflation. Like other nations during WWII, Germany implemented rationing along with wage and price controls to contain inflation. While these instruments keep prices stable, they create “pent up” demand for scarce goods and services. Since there is ample liquidity due to deficit spending and debt monetization, inflation can explode once controls are lifted. Such was the situation the allies found when they took control of Germany after the war.

There were other conditions that affected postwar Germany as well. Although the allies had conducted an aggressive air campaign against Germany, much of the industrial sector survived the war intact. In fact, most of the allied bombing destroyed residential areas. Thus, Germany had a mostly secure industrial base but a severe housing shortage. In addition, it also had a well-trained workforce; although many German soldiers died in the war, a large number of workers had learned manufacturing skills during the war. In addition, there was heavy German migration into the Western sectors of Germany. Some were trying to escape from the Soviets while others were expelled from Czechoslovakia and Poland where Hitler had resettled Germans during the war. These immigrants had worked in industry during the war as well. In effect, a base for recovery survived the war.

However, it wasn’t clear how these assets would be put to work. The allies, worried about inflation, maintained rationing along with wage and price controls. This led to a flourishing black market and scarcity. Since workers couldn’t buy much, it was difficult to spur work effort as households received ration cards without working. None of the Western allies had a clear idea how to restore Germany and prevent unrest.

Ordoliberalism

Into 1948, inflation continued to rise despite controls. Two major political figures, Konrad Adenauer and Ludwig Erhard, developed a plan to restore economic growth. Their ideas came from a concept called Ordoliberalism. This concept is something of a middle ground between pure neoclassical economics and government intervention concepts, like Keynesianism and socialism. Essentially, Ordoliberalism relies on the market to allocate goods and services but believes the government must intervene to prevent firms from dominating an industry. Thus, the role of government is to prevent economic concentration. Essentially, like neoclassical economics, it believes that perfect competition is the best model for the economy but the Ordoliberal economists argued that neoclassical economics will not prevent concentration. And so, if the government ensures that markets remain competitive, there is no need for government deficits, redistribution policies or activist monetary policy.

In Ordoliberalism, the government should monitor competition but avoid deficit spending. The central bank should focus on price stability only. The market itself, the interaction of business and labor, would act to stimulate or depress the economy as necessary.

Adenauer and Erhard were Christian Democrats. During the Nazi years, Christian Democrats pressed for a social market structure aligned with mostly Catholic social teachings. Due to the tragic excesses of fascism and communism, both wanted to follow a different path, which became Ordoliberalism. It should be noted that the other major party in Germany, the Social Democrats, have leaned more toward socialism or Keynesian policies. But, even Social Democrat administrations have implemented policies that were in line with Ordoliberalism. For example, the Hartz labor market reforms, which emerged from a government-sponsored commission in 2002, were implemented by Gerhard Schroder, a Social Democrat. It appears that Ordoliberalism is a commonly held ideology among the ruling classes in Germany.

To implement this plan, Adenauer and Erhard, in 1948, simultaneously ended price and wage controls along with rationing, and introduced a new currency, the Deutsche mark (DM), replacing the war-era Reichsmark (RM). The new currency was swapped with the old one at 10:1 (RM to DM), which dramatically reduced the money supply and lessened inflation pressures. The combination of ending market restrictions caused by rationing and wage/price controls and the introduction of a stable currency led to rapid changes. Goods quickly returned to store shelves and the hated black markets collapsed without a serious rise in inflation. Simply put, producers and consumers were properly incentivized to bring goods to market and purchase them.

The program was a rousing success. Industrial production jumped 25% within two months and was up 50% in six months. GDP rose 15% per year from 1948-50 and averaged 8% per year in the 1950s. This Wirtschaftswunder returned Germany to its status as a major economic power in Europe and the world.

Perhaps most importantly, Adenauer and Erhard were able to show that capitalism under the proper constraints could be a viable economic and social system. For much of the last century, various forms of socialism and corporatism (fascism) were considered better systems for organizing economies. Germany’s success showed that capitalism could compete and, in fact, outperform these other systems. Although the failure of socialism, corporatism and communism became virtually self-evident by the 1990s, that was not the case for much of the past 100 years.

For Germany, solid and stable economic growth, low inflation and a hard currency became the symbol of the country. As the economist Robert Hertzel noted:

The end of World War II had left Germany without national institutions. The DM became the first national symbol of the new Germany. West Germany had the DM before it had a flag…Germans prized the stability of the mark as a symbol of social stability and economic prosperity. The DM symbolized everything that Germany did right after the war.[1]

Narratives and Other Factors

Like any founding narrative, Germans believe that hard money, stable fiscal policy and reliance on free markets, with the proviso that competition is maintained, were solely responsible for the economic miracle in Germany. However, there were other circumstances that supported the recovery.

The intact industrial base: Because Allied bombing had not destroyed Germany’s industrial base, the economy had enough capacity to grow rapidly without inflation.

Geopolitically induced immigration: Fear of the Soviets and the expulsion of Germans living in Poland and Czechoslovakia increased the potential labor force in West Germany. This influx of skilled labor supported growth and productivity.

The Marshall Plan: Although the Marshall Plan initially supported Western European nations except Germany, rising growth in those nations supported German exports.

Korean conflict: As the U.S. led a coalition of forces to liberate South Korea, demand rose sharply for commodities and industrial goods. Germany was able to increase its exports to support the war effort.

The reserve currency: Because the U.S. accepted the reserve currency role at Bretton Woods in 1944, America became the global importer of last resort. Germany was able to prosper under this system by selling goods to the U.S. More importantly, Germany was able to ignore the international effects of its domestic policy because the U.S. absorbed any excess German production.

Since Ordoliberalism assumes that markets automatically balance when there is competition, free markets and stable price levels, policymakers can safely ignore the rest of the world. If the Keynesians are correct, and sticky wages and prices prevent an effortless adjustment to equilibrium, the German model actually relies on foreign demand to achieve equilibrium. In other words, when Germany has excess saving or a drop in investment, it simply exports its way to balance the economy. Although there is an endless debate among economists as to whether Keynes was correct in his assumption about wages and prices, Germany’s history of trade surpluses does suggest that the country has used foreign markets as a “safety valve” for excess production. This safety valve also supports full employment.

Ramifications

Every country’s narrative is designed to portray the nation in a positive light. At the same time, the narrative also offers insights into how the country will behave.

The Ordoliberal heritage that Germany holds has important ramifications not just for the Eurozone but for the global economy and financial markets. As we note above, Germany believes that the formula it followed, which is focused on low inflation, hard money and balanced budgets, led to the economic miracle. And so, if other nations would follow its lead, they too could enjoy a Wirtschaftswunder.

Until the Eurozone was created, Germany could safely maintain this model; it suffered through periods in which the DM appreciated and weakened economic growth, but given that the Germans wanted a hard currency, they generally accepted that downside. Since Germany was a major economy but still small enough to use exports to balance its economy without serious international repercussions, the Germans could maintain Ordoliberalism without incident.

However, the creation of the Eurozone changed everything. As noted above, Germany’s national identification was tied to the beloved DM. Its citizens were not prepared to jettison their currency without creating a new one that was similar in structure. And so, in the creation of the European Monetary Union (EMU), Germany pressed for fiscal rules that would “encourage” other Eurozone nations to follow Germany’s fiscal lead. In addition, it wanted the new currency to be “hard”; in other words, the ECB should only consider inflation control in its mandate and not be concerned with stimulus. After all, if the economy were properly constructed, such stimulus was unnecessary.

There is no other nation in Europe, even those who tend to be sympathetic to Germany’s position, which supports hard money and fiscal balance for the same reasons Germany does. For Germany, the essence of its postwar success is based on Ordoliberalism. Germany cannot compromise on this position without forfeiting its national narrative.

And so, what Germany is trying to do with the Eurozone is implement Ordoliberalism, writ large. Unfortunately, this is not just a problem for the other Eurozone nations who do not share Germany’s vision; it is a problem for the world, too. The combined GDP of the Eurozone makes it the largest economy in the world. If it behaves like a single nation, the Eurozone is an economic behemoth that rivals the U.S. in terms of economic power. Such large entities have a global impact.

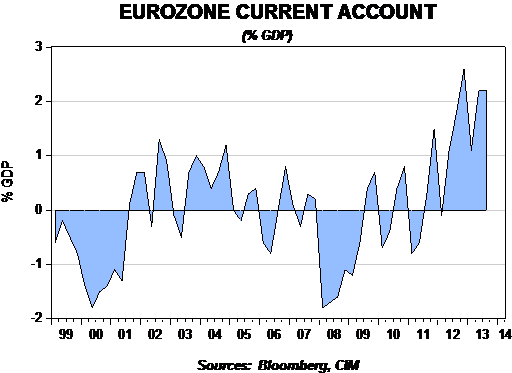

The chart below highlights the issue.

This chart shows the Eurozone current account scaled by GDP. The current account is the broadest measure of foreign trade and transfers. For much of the Eurozone’s existence, the current account was either in deficit or in small surplus. However, since 2011, when the Eurozone crisis spread beyond Greece, the region has been running significantly larger surpluses.

When a country runs a current account surplus, it is relying on the rest of the world to absorb the goods and services it wants to sell. If these nations refuse to participate, there is an oversupply of goods in the domestic economy (or, put another way, a lack of demand for the goods produced). In effect, the Eurozone is doing what Germany has done for years, which is “borrow” demand from the rest of the world to clear its domestic markets and avoid unemployment.

As this chart shows, Germany has run persistent current account surpluses; only during unification and the creation of the Eurozone did Germany run deficits, and these were minor. With labor market reforms in the last decade, Germany has become increasingly reliant on foreign demand. Much of that foreign demand came from within the Eurozone as the periphery nations became the mirror image of Germany—they ran corresponding current account deficits and borrowed to fund this consumption. The lending mostly came from Germany.

Germany appears to be creating the Eurozone in its own image. Unfortunately, this process has had two serious negative effects. First, it has forced near deflationary conditions on much of Europe as these periphery nations struggle to service the debt they have incurred in a slow growth, low inflation environment. Second, it is putting an enormous burden on the world as the Eurozone, the largest combined economy on earth, is running a current account surplus. In effect, it is a global tightening of credit to the degree that the euro is used for reserve purposes.

Thus, Germany’s critics—Paul Krugman, Martin Wolf, Michael Pettis—all argue that Germany needs to expand its consumption and reflate, not only to boost growth and allow for the Eurozone periphery to service its debt, but also to support global growth. However, as we have tried to show here, Germany isn’t engaging in reflation policies due to its core beliefs. Bundesbank President Weidmann, German Finance Minister Schauble and the president of the influential IFO institute, economist Hans-Werner Sinn, have all been very critical of ECB President Draghi. They are questioning Draghi’s use of unconventional monetary policy, fearing that it will debase the euro. However, we believe German opposition to Eurobonds, unconventional monetary policy and fiscal excess is deeply rooted in the founding narrative of postwar Germany. Simply put, Germany is pressing for fiscal and monetary restraint because it views these policies as fundamentally correct, the policies that lead to Wirtschaftswunder.

In some respects, this is a classic case of the “error of composition.” In that logic error, what works at the micro level is assumed to work as well at the macro level. However, that isn’t always the case. Saving is a good example. If some save and some borrow in a society, those who save find productive use of their excess and those who borrow can use the funds for starting a business, buying a house, etc. However, if all save and no one borrows, there is simply a loss of demand. If every nation acted like Germany, the global economy would sputter; not every nation can balance its consumption and production with persistent current account surpluses. Some nations must run a deficit. In the current global economy, that nation is the U.S. due to the dollar’s reserve currency role.

At the same time, given how deep-seated Germany’s beliefs are on this issue, it is hard to see how it would allow for the solutions that Krugman, Wolf and Pettis recommend. For Germany to make this change would be akin to the U.S. deciding that democracy isn’t a universal virtue.

If this notion is true, what does the future hold? We doubt Germany can be successful in its goal of making the Eurozone “Greater Germany.” The rest of the world will likely respond by implementing trade barriers to Eurozone goods and investment. Without the “safety valve” of exports, we doubt Ordoliberalism can work on a large scale. Since Germany probably won’t adjust, we suspect the Eurozone project is probably doomed. Eventually, other Eurozone nations will force Germany’s exit from the single currency or the periphery nations will exit on their own. The disruption this would cause to the world economy would, at a minimum, probably trigger a global recession. It may lead to another financial crisis as well.

When does this occur? There is no clear answer to this question. The periphery nations in the Eurozone seem to be willing to tolerate weak growth and near deflation for now. They all seem to fear the loss of status that would come with leaving the single currency. We will be watching closely the relations between Italy, France and Germany. The former two nations have economies large enough to stand up to German pressure and their exit from the Eurozone would likely trigger the aforementioned crisis. A smaller nation, like Greece or Portugal, probably would not trigger a broader crisis. We don’t know when, but at some point Germany will either be forced to abandon Ordoliberalism (which we see as highly unlikely) or the Eurozone project will fail. We doubt this is going to occur in the next year, but it is important enough to warrant persistent monitoring.

The general consensus is that a weaker euro is inevitable due to the Federal Reserve embarking on reducing policy accommodation while the ECB becomes more aggressively accommodative. To some extent, a weaker currency would seem to be in Germany’s best interest. After all, Germany is an exporting power and a weaker currency would make it even more competitive. However, policies designed to deliberately weaken the currency are an anathema to Ordoliberalism. Thus, Germany may oppose measures from the ECB to reflate even though it would likely boost German economic growth. The euro may still weaken further, which is the overwhelming consensus, but the expanding current account surplus will tend to boost the euro, not weaken it. And so, the surprise for 2015 may be that the dollar doesn’t strengthen as much as expected because Germany will not support policies that will foster a weaker euro.

Overall, we expect Germany to maintain its Ordoliberal position. The emergence of the Alliance for Germany party, which is an anti-euro party running to the right of Chancellor Merkel’s Christian Democrats, is limiting the chancellor’s room to maneuver. Recently, Merkel, who has generally supported Draghi’s efforts to hold the Eurozone together, has become less supportive as conservative opposition to Draghi increases. Given Germany’s influence, it is difficult to see how the ECB will be able to deploy aggressive unconventional policies. If so, Europe may be in for a bout of deflation and recession.

Bill O’Grady

October 27, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[1] Hertzel, Robert. “German Monetary History.” FRB of Richmond Economic Quarterly, Spring (2002).

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

© Confluence Investment Management