When I entered the Fed-watching business over three decades ago, a clichéd phrase of advice from graybeards was: “Watch what they do, not what they say.” Thinking back, there was not actually much Fed rhetoric to either watch or hear.

Paul Volcker was new in the job of Fed Chairman, Ronald Reagan had just been elected President, and Ted Turner had not yet launched CNN Headline News. All three men are now recognized as giants of transformative change in America’s life, altering not just how we conduct our affairs, but also how we think about ourselves.

It really was a good time to be a newly minted graduate in short pants on Wall Street. The fiscal authority was pursuing something called supply side economics and the monetary authority was putatively pursuing monetarism. Keynes was in rehab for inflationary intoxication, and Friedman was the straw stirring the free-to-choose drink. The visible fist of government was cursed and the invisible hand of markets celebrated.

Ah, yes, a most interesting time to start a career on Wall Street: a time of existential ferment in our nation’s economic policy, best characterized by tight monetary policy, loose fiscal policy and blind belief in the ability and willingness of capitalists to regulate and discipline their own affairs. At such a juncture in history, the advice of the graybeards to me to watch what “they” do rather than what they say was sage counsel.

This was particularly the case in watching the Volcker-led Fed, which pegged short-term interest rates, but said it didn’t, maintaining that it simply controlled growth in the money stock via changes in “the degree of pressure on bank reserve positions.” Volcker also thundered that the Fed had virtually no influence over long-term interest rates, which were putatively sky high because of outsized budget deficits and inflationary expectations.

Accordingly, the Fed-watching community of that era was, in practice, a community of plumbers: We spent a huge amount of effort and time anticipating and reverse engineering the day-to-day flows (called “operating factors”) that drove the activities of the New York Fed’s Open Market Desk, which were necessary to maintain the existing “degree of pressure on reserve positions.”

Yes, we were obsessed with what the Fed actually did, which they ordinarily did at 11:40 Eastern time: customer repo versus system repo, term versus overnight, bill passes versus coupon passes and the dreaded matched sale. Were the operations strictly “technical,” orchestrated to sterilize the net of churning operating factors, or was the Desk implementing a FOMC-directed change in the degree of pressure on reserves – to wit, changing the FOMC’s implicit fed funds rate target?

To be sure, we Fed nerds were also expected to forecast such changes, with especial focus on changes in the FOMC’s “inter-meeting bias,” also known as the “tilt,” which granted the Chair authority to implement changes without further FOMC deliberations. But our day job was as plumbers, to literally figure out when policy changes were actually unfolding by chasing the Fed’s open market transactions through the banking system’s pipes.

Dot mavens

Now a graybeard, I preach to youngsters the opposite of the sermon I was given: Watch what they say, not what they do. The Secrets of the Temple that Bill Greider wrote so poignantly about in 19831 are no longer secret. The FOMC not only very publicly pegs the fed funds rate (albeit in a 25 basis point range, so as to maintain some degree of no-hands-Mom myth), but also provides “forward guidance” as to its fed funds rate peg: The FOMC forecasts itself!

Thus, the game of Fed forecasting is no longer an absolute sport, as in my youth, but a relative game: The FOMC’s dots are the benchmark, and forecasting is an over-under game versus those dots. To be sure, today’s game is similar to yesterday’s game, in that betting money on Fed forecasts involves wagering relative to market prices, notably the forward curve for future short rates.

What is new is that the forward curve is now an explicit instrument of monetary policy. More bluntly: The Fed explicitly seeks to influence and manage long-term asset prices, all of which, by the (Gordon) laws of financial arithmetic, embed expectations of future Fed policy.

The Fed doesn’t put it exactly that way, of course, preferring to speak of influencing “financial conditions.” Political correctness and all that. But “financial conditions” don’t have ticker symbols with prices: Long-term financial assets do – bonds, stocks and currencies.

Thus, central bank watching in today’s world is all about reverse engineering where central banks “want” those big-three asset prices, which are now Fed “targets,” in a fashion similar to the money stock “targets” of my youth. That is not to suggest, I hasten to add, that central bankers always get what they want!

There are many slips between cup and lip, between instruments and targets. Reality has a nasty habit of intruding on wants and best intentions. And needs.

Doing what we were trained to do!

We Fed-watching plumbers of long ago now finally get to do what, for me, is most rewarding:reverse engineering the internal consistency, or lack thereof, in the FOMC’s theoretical musings. And, in turn, opining on the logic of the explicit FOMC forecasts of its own future behavior, in the context of those theoretical footings.

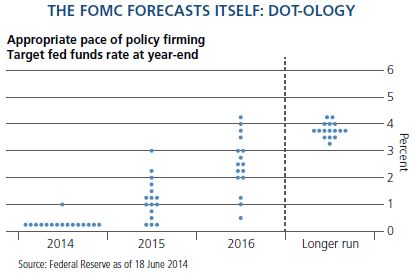

Yes, for me, it is the most satisfying time of my Fed-watching career. And not just because I’ve got a cool new job, though I do. What I pinch myself most about is actually one blue dot: the FOMC’s “longer-run” forecast of the steady-state “neutral” fed funds rate, which has a current “central tendency” of 3¾%, recently shaved from 4%; see the Dot-ology Box!

Recall: It was only in 2012 that the Fed began explicitly hanging its collective hat on a numericallonger-run forecast for its short-term peg! But the 4% “neutral” number has long existed in the ether of Fedspeak, notably since 1993, when John Taylor devised and divined his famous Rule, which postulates that a perfectly tamed business cycle should/will beget a 4% fed funds rate: a 2% real rate plus an at-target 2% inflation rate, in the context of at-potential, or full-employment, GDP growth.

Taylor’s Rule was and is a cyclical operating guide for the FOMC to modulate the fed funds rate on both sides of secular “neutral,” founded on the cyclical Phillips Curve trade-off between unemployment and inflation. Rational-expectations perfection would be no modulations at all: Markets would so understand the FOMC’s reaction function, efficiently discounting prescribed modulations in the Fed’s policy rate, as to obviate the FOMC from having to make them!

Indeed, Taylor argues – to this very day! – that if only the Fed had religiously followed his Rule over the last two decades, the U.S. economy at present would be in a much finer place than it is. Not a perfect place, to be sure, not even Taylor would argue, but a much better place.

I have no present desire to pick a fight with Taylor about his counterfactual assertion: Serenity starts with accepting that which cannot be changed, and that includes history. Forward!

But I do applaud John for the ubiquity that his Rule has achieved, because it conveniently frames conventional wisdom, which can also be called active intellectual laziness – which has plagued my profession pervasively ever since the Minsky Moment of 2007–2008.

The Taylor Rule was not designed for dealing with Liquidity Trap pathologies, because it was modeled on a time frame that didn’t include any Liquidity Traps! At least in the United States, and when Taylor published his Rule in 1993, Japan was in the infant years of its then-denied Liquidity Trap.

As a pragmatic matter, the Taylor Rule over the last half decade has been useful primarily in confirming the wisdom of Keynes’ parting observation in the closing chapter of The General Theory:

“The ideas of economists and political philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed, the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually slaves of some defunct economist.”

The tenacity of some FOMC participants in defending the rounds-to-4% longer-run blue dot confirms too, perhaps, the robustness of yet another Keynes dictum:

“Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

Channeling Rudi

Long-time – and patient! – readers probably are now bracing for an ode to Minsky, a most unconventional theorist, an outcast and renegade in academic circles, whose Financial Instability Hypothesis has greatly informed and influenced my own work.

Gotcha: Ain’t going to do it!

Rather, I want to riff on the work of another (sadly passed) man, who was held in highest esteem at the highest rungs of the academy: Rudi Dornbusch. In 1976,2 Professor Dornbusch took on conventional wisdom that floating exchange rates – adopted after the breakup of the Bretton Woods fixed rate regime a half decade earlier – were inexplicably volatile, relative to the doctrine of monetarism, as espoused by none other than Milton Friedman.

Conventional monetarist religion had held that a regime of floating exchange rates would unleash market forces to adjust exchange rates in real time, guided by the lodestar of Purchasing Power Parity (PPP), thus truncating buildup of imbalances in trade, which had, in the earlier fixed exchange rate regime, begot violent volatility when governments were “forced” to break the fixes.

Reality did not conform to those monetarist promises, with wild over- and under-shooting of PPPs, and Dornbusch sought to theoretically explain why, developing his exquisitely simple, yet elegant model of rational overshooting. Its theoretical foundation is very simple: Prices on Wall Street move much more quickly than prices on Main Street.

Duh, you say, don’t we all know that? Yes, we do. But that reality is often assumed away in economic theory, most especially in high academic churches steeped in the efficient markets hypothesis, presuming that the invisible hands of markets all wear the same behavioral gloves.

They don’t. What Dornbusch demonstrated was that:

1) If a country has an “overvalued” currency on a PPP basis (its burgers are way overpriced relative to the rest of the world on the Big Mac Index) and is experiencing a growth-debilitating erosion in trade, and

2) If the country responds with a “shock” of monetary easing, slashing interest rates (as it is free to do under a floating exchange rate regime!), then

3) Its currency will rationally plummet not just to “fair,” but to “undervalued” on a PPP basis.

The reason:

1) A country’s Main Street prices (inflation) are very slow to adjust to the “shock” of monetary easing (reducing imports and increasing exports, improving growth), and

2) Until that adjustment has unfolded, global investors will be stuck with the country’s shocked-lower interest rates, and accordingly,

3) Will rationally be willing to hold the country’s bonds only if its currency plummetsbelow PPP, fostering expectations of room for future appreciation.

Simply put: Rudi explained to us that global investors will buy a country’s rich bonds only if the country’s currency falls so far as to make its burgers dirt cheap.

Really, his model is that simple, yet profound (as all great breakouts in economic theory tend to be!). In turn, Rudi’s theoretical nugget provides huge insight into the why and how of escape from a Liquidity Trap: Wall Street prices move much more quickly and further than Main Street prices.

Wall Street’s unjust moment

Traditionally, the political catechism of monetary policy is that the Fed doesn’t really give a damn about Wall Street, that the capital markets are only the conduit between the Fed and Main Street. Main Street outcomes for employment and inflation are what really matter, we are taught, and thus the only “targets” of monetary policy. And so long as a Liquidity Trap can be avoided, this theological tenet has a loud ring of truth.

This was particularly the case before financial deregulation, when monetary policy “worked” primarily through the conventional banking system, with Main Street’s savers on the liability side of banks’ balance sheets, and Main Street’s borrowers on the asset side. Wall Street was a place walled off from the banking system (by Glass-Steagall, among other things), where people of money traded securities amongst themselves, while also channeling capital – notably equity – to the frontiers of economic growth.

In that catechism and that world, the notion of the Fed “targeting” stock and other long-term financial asset prices was blasphemy. And politically, it still is. But that world no longer exists: Wall Street and the deregulated banking system – conventional and shadow – have morphed into one.

In turn, when a Liquidity Trap hits, the Fed is in a pickle. The Fed can take its policy rate to the Zero Lower Bound (ZLB), but it will not generate a revival of either increased demand for or supply of bank credit and, in lagged train, upside action for prices and wages on Main Street. Such is the nature of monetary policy in a Liquidity Trap, which is akin to the position of a cheesecake vendor at a convention of recovering overeaters: The customers ain’t buying, even though they are known to like the product, and the price is zero.

In which case, the Fed isn’t impotent. But with the banking system and its Main Street customers locked in the Nurse Ratched Center for Deleveraging of Balance Sheets, where exuberance, rational and otherwise, is strongly discouraged, the monetary authority, by default, must turn to Wall Street for able-and-willing partiers.

Yes, it is a Hobson’s choice. Theoretically, the choice should never be on the table, if the fiscal authority is willing and able to party hardy, backed by the sovereign’s borrowing prowess. But ifthe fiscal authority demurs, for whatever reasons of defunct orthodoxy, the monetary authority must – unless it wants to nursemaid an enduring Liquidity Trap – dance with Wall Street.

It is not a tasteful choice for the Fed at all. It reeks with social injustice. But it also happens to be the only viable choice: Use all available powers, with whatever-it-takes abandon, to reflate prices that are amenable to going up: long-term bonds and stocks.

How does it work?

Printing money to reflate Wall Street prices is normally thought to “work” through a trickle-down channel: Make the wealthy wealthier and they will spend more ebulliently, stimulating aggregate demand more generally. There is indeed an element of this dynamic involved. But it is not, in my analysis, the straw that stirs the Liquidity Trap-escape drink.

For, you see, Liquidity Traps are born of preceding (Minsky-type) excesses of debt-to-equity ratios. That is, there is too much private sector debt relative to equity, not too much debt per se. It’s a private sector balance sheet problem that begets an income statement problem, not the other way around.

To be sure, a recession in the wake of a Minsky Moment does create an aggregate demand, and thus aggregate income problem, as recessions poleaxe employment and labor’s bargaining power for wage gains. This dynamic turbo-charges Main Street’s woes in managing any given debt-to-equity ratio.

But the existential macro problem in a Liquidity Trap is a balance sheet problem: too little equityrelative to debt. This problem can be mightily relieved by driving up the price of assets that are the collateral for debt, thereby restoring and creating equity.

Yes, “creating” equity: Capital gains – realized or not – are the only newly created asset withoutan associated, offsetting liability. “Paper wealth!” some of you are no doubt retorting under the breath. And arithmetically, I won’t quarrel with you. I will simply remind that a Minsky Moment itself is a “paper” problem: too much dodgy paper debt relative to the paper value of levered assets.

Accordingly, getting out of a Liquidity Trap with monetary policy playing the lead role necessarily involves a Dornbuschian sequence of rational overshooting: The Fed must drive up Wall Street prices, which move quickly, so as to get to Main Street prices that move up slowly, most importantly, wages.

This sequencing implies that Wall Street’s prices axiomatically will, in the short run, “overshoot” their long-term fair value, as the Fed appropriately and credibly commits to staying at the ZLB,until paper wealth creation endogenously deleverages private sector balance sheets sufficiently to restore animal-spirited risk taking on Main Street.

This sequencing implies that Wall Street prices must become very rich relative to Main Street prices in order to achieve so-called escape velocity from the Liquidity Trap. At the transition point, Wall Street prices will be rationally “overvalued” relative to their long-term “fair value.”

Rational? Ain’t it just a bubble? No, because unless and until Main Street prices go up, Wall Street prices will be rationally priced on the assumption – sometimes called a “Fed Put” – that the central bank will stay pinned against the ZLB.

As and when the Rudi Lag plays itself out, however, Wall Street’s prices must rationally re-price to two-sided Fed policy risks.

Bottom line

This process has been unfolding for well over a year now, ever since Ben Bernanke signaled a plan for ending QE3, a necessary condition for the FOMC to even consider lifting off the ZLB. The early stages of Wall Street’s re-pricing, now known as the “taper tantrum,” were rational, even if violent. Ever since, Wall Street has been in a “price discovery” process for what the post-Liquidity Trap “neutral” Fed policy rate should/will be, once the Fed begins liftoff from the ZLB.

Long-term bond prices have rationally not recovered all the ground lost in the taper tantrum: Removal of the Fed Put axiomatically should lift the term premium for duration risk. But yields have fallen, also rationally, as the market has rejected the FOMC’s rounds-to-4% blue dot: PIMCO’s New Neutral before your eyes!

Stock prices are, of course, higher than before the taper tantrum, and rationally so: If bonds reject the FOMC’s 4% blue dot, then stocks should, via a Gordon Model, rationally follow suit. And they have.

Thus, Wall Street has, so far, gotten lucky twice: the Unjust Moment followed by The New Neutral. Somehow, it just doesn’t seem right. And it isn’t; it just is.

But as Martin Luther King intoned long ago, the arc of the universe does bend toward justice. And as I wrote in July,3 I think it will do so with the Fed letting the recovery/expansion rip for a long time, fostering real wage gains for Main Street.

This implies that the dominant risk for Wall Street is not bursting bubbles, but rather a long slow grind down in profit’s share of GDP/national income. And you can stick that into a Gordon Model, too!

Bonds and stocks may at present be rationally valued, but borrowing from the lyrics of Procol Harum’s Keith Reid: Expected long-term returns are turning a more ghostly whiter shade of pale.

© PIMCO