WWI began on July 28, 1914. It was the second industrial war and considered a “world war,” although nearly total global military engagement didn’t occur until WWII. It was a devastating conflict, with an estimated 37 million military and civilian casualties and roughly 17 million fatalities.

The postwar effects were also substantial. Europe’s global domination was severely weakened and, as a consequence, the U.S. became a rising global power. Classical economic liberalism, which supported free markets, free trade and small government, was replaced by deeper government involvement in the economy. This occurred because governments, in an effort to mobilize the economy for the war effort, began to extend their regulatory control of the economy. The war tightened labor markets, allowing for increased union membership. As laborers increased their political power, the gold standard was undermined. The gold standard required governments to manage their monetary policies toward external balance, meaning that if a nation was running a persistent trade deficit then contractionary policies were automatically implemented. These austerity policies tended to most disadvantage the working class. For the gold standard to work, therefore, a compliant and politically weak working class was necessary. After the war, the rise of organized labor made it very difficult to maintain the gold standard.

From a market perspective, measuring the impact of geopolitics is difficult. Some events are very short-term in nature and have only a modest impact. Others are more substantial but are still mostly cyclical. And then there are those events that permanently change the investing landscape. At the time the event is unfolding, it is never easy to know exactly what sort of situation one is dealing with. In retrospect, cause and effect can appear almost perfectly linear; however, in the fog of the moment, it is never completely clear whether a geopolitical event is a “game changer” or simply a blip.

In this report, we will begin with a short recap of the onset of WWI. We will also examine the problem that comes from induction, the logical process of observing the world and predicting the future. From there, we will discuss the “lessons learned” from the post-WWII and post-Cold War era with an analysis of what may be changing. As always, we will conclude with market ramifications.

The Onset of WWI

Going into the second decade of the 20th century, global economic growth was steadily expanding. European nations dominated international relations due to the colonial expansion of the previous two centuries. Although the U.S. had the world’s largest economy, it had only a passing interest in global affairs.

It should be noted that the present boundaries of the lower 48 states were not completed until the Gadsden Purchase of 1912. America’s focus had been on building out its “manifest destiny” and populating the West. Britain was considered the global superpower with the British pound as the global reserve currency. Furthermore, the world economy was heavily globalized; some economists have argued that the global economy did not exceed the pre-war level of integration until the 1980s. In 1910, Norman Angell published The Great Illusion, which argued that society and the global economy had reached a point where war was simply futile because it didn’t pay. Because of economic integration, even victors in war would not make significant gains compared to the benefits that come from peace. In other words, Angell argued that using war as an instrument of foreign policy was outdated. Although Angell has been criticized for saying war was “impossible,” that really wasn’t his position. He said it would be futile; the events of 1914-18 generally proved his point.

Historians have debated the causes of the war. Barbara Tuchman’s theory was that the structure of treaties and the beginning of mobilizations made the war inevitable, much like dominos set in motion. In a book published recently, Christopher Clark argues that a series of miscalculations by European leaders, rising Balkan nationalism and a crumbling Ottoman Empire were the proximate causes. However, at any point, a different decision may have led to a different outcome. Tuchman would argue that the war was unpreventable; Clark would counter that the war could have been avoided if the parties involved had not played a “game” of brinkmanship that ended up triggering the conflict.

The fact that eminent historians can come away with different theories as to why WWI occurred shows how complicated Europe was before the war. Despite these differences, nearly all historians that have examined this period (including the aforementioned) have noted the tensions that a rising Germany caused in Europe. Germany formed in the aftermath of the 1870 Franco-Prussian War and developed into an economic powerhouse. Germany’s army became the strongest in Europe and its navy grew rapidly. The response to a rising Germany was the creation of treaties between France, Britain and Russia. Germany countered with its own treaties with the Austro-Hungarian Empire and Italy (which the latter failed to honor).

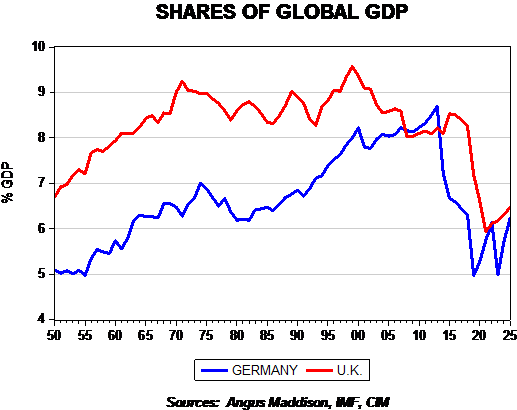

This chart shows the global shares of GDP of Germany and Britain from 1850 to 1925. Just before 1910, the German economy had eclipsed the British economy. When a rising power begins to rival the ruling power, the tensions that arise are called the “Thucydides’s Trap.” Thucydides noted that a rising Athens threatened the hegemony of Sparta, leading to the devastating Peloponnesian War.

WWI turned out to be the war that signaled the beginning of the end of Western European hegemony in world affairs. At the outset, it wasn’t obvious that this war would be as devastating as it was. Although most nations go into war on the assumption it will be short, the European powers were really not prepared for how this war evolved. Trench warfare and the introduction of industrial weapons (aircraft, poison gas, massive artillery, tanks, etc.) made WWI a modern war.

To understand how this war changed the world, imagine that an investor was putting together a conservative bond portfolio that could not be changed for a decade; the bonds would be placed in a deposit box in 1913. Most likely, our investor would have put his investment into five of the world’s largest nations’ sovereign bonds. So, Germany, Britain, the United States, France and Russia would have been reasonable choices. Assuming equal weighting, by the time the box was opened in 1923, 40% of the portfolio would have had no value and probably only 20% would have maintained its value. German bonds would have become worthless during the hyperinflation. Czarist bonds were not honored by the Soviet Union. Britain and France were struggling to meet their obligations. Only the U.S. would have been completely safe. This exercise shows that, at certain times, what appears to be safe can sometimes become toxic.

Geopolitics and the Problem of Induction

Since 1946, the Center for Systemic Peace has documented 331 episodes of major armed conflicts. How does an investor know which ones are irrelevant to the markets, which ones have significance and which are true inflection points? Analyzing these situations is difficult to assess but all geopolitical analysts eventually rely on inductive logic. Induction is described as projecting a future effect from an apparent persistently causal factor. In his book, The Black Swan, Nicholas Taleb reports that biologists believed that no swans were black. The discovery of black swans in Australia meant that that theory was incorrect. But, until that discovery, biologists held that no black swans existed.

Induction at all times carries a degree of uncertainty. It is always possible that an exception to a rule can be found. For example, investors began to expect that the Federal Government would always bail out large financial institutions when they faced bankruptcy. The government’s behavior since the 1980s supported that idea. And so, when the Treasury decided to allow Lehman Brothers to fail in September 2008, it created a massive financial shock.

Philosophers have generally been uncomfortable with the lack of certainty inherent in induction. David Hume, the British skeptical philosopher, pointed out serious problems with cause and effect. Bertrand Russell had his famous “chicken problem.” Although induction is uncertain, the reality is that induction is how humans have survived. Our ancestors analyzed patterns in the environment and were able to use that information to prosper. Hume speculated that humans were induction machines; we watch for patterns and behave accordingly. In the investing process, we engage in similar behavior.

Perhaps the best way to think about cause and effect is to understand that virtually all cause and effect relationships are “surrounded” by other factors. The reliability of the relationship is dependent upon the continued stability of these surrounding factors. Unfortunately, there is no way of knowing completely which factors are critical to the process. The condition known as “spurious correlation” highlights this problem. In a spurious correlation, two variables seem to move closely together (or are a near-mirror image, in the case of negative correlation) to the point where one of the variables appears to cause the other. However, in reality, they only behave in that fashion because one or both are highly correlated to an unknown third (or fourth, fifth, sixth, etc.) variable. It doesn’t become clear that these other variables matter until the first relationship breaks down. This analysis suggests that “repeatability,” the number of times or the duration for which a relationship holds, may not be meaningful. After all, for the Russells’ chicken, 100 good days end badly on the 101st! In general, analysts try to combine observations with plausible theories to explain why variables behave in a certain fashion. However, in reality, there is a fine line between a theory being a workable explanation of why two variables move together to being a “just so” story that merely offers justification for believing that two variables will continue to correlate in the future.

We believe that history is important, but the hard part is gleaning the right lesson. Why did European leaders fall into WWI, for example? First, they probably underestimated how powerful the other side was in the conflict. By focusing on their own strengths, they failed to account for the strengths of their opponents. Second, they probably used the wrong war as an analog. The Franco-Prussian War lasted less than a year and was mostly a war of movement. As noted above, the U.S. Civil War was a better comparison, with its use of industrial armaments, some trench warfare and, perhaps most importantly, a war of attrition. Essentially, the North had too large of an economy for the South to overcome. In the case of WWI, neither side could win the war of attrition; it wasn’t until the entry of the U.S. into the war that it was decided. Third, because they failed to prepare for a long war of immense cost, none of the nations involved in the conflict were aware of the devastation it would cause. If the leaders would have had a better idea of how difficult the war would be and the precarious positions in which they would find themselves in the aftermath, they may have been more reluctant to march toward war.

Lessons Learned

So, what do the history of wars and conflicts tell us about markets? Clearly, some events have greater effects than others. Here are a few “lessons learned” since 1945.

Strategic commodities matter. The Middle East has been unstable since the end of WWII. Other regions have been unstable as well. However, the importance of oil supplies has made Middle East conflicts particularly important. The Yom Kippur War, which led to the Arab oil embargo, led to a deep recession in the U.S. and occurred in the midst of a secular bear market. Thus, wars that disrupt key commodity supplies can have outsized importance.

Nuclear weapons changed everything. Although nuclear weapons effectively ended WWII, they have evolved into the ultimate defensive weapon. In a war between nuclear powers, it is hard to imagine either side fighting to unconditional surrender. The losing side would be tempted to unleash a nuclear holocaust on its opponent. Because of the impact of nuclear weapons, the U.S. and the U.S.S.R. generally avoided direct confrontations during the Cold War. Instead, both nations tended to become involved in proxy wars. Although there were some long and bloody wars during the Cold War era (e.g., Korea, Vietnam, Afghanistan), none of them were on a comparable scale to WWI or WWII. Thus, markets are inured to believe that a world war isn’t possible, assuming that a world war would involve two or more nuclear powers.

A bipolar world is easier to analyze. It is tempting to argue that a bipolar world was more stable. After all, when the U.S. and U.S.S.R. divided the planet into their respective spheres of influence, foreign policy centered on countering the behavior of the other superpower. The record unfortunately shows that the incidents per year during the Cold War averaged 5.1, whereas in the post-Cold War era the average has been 4.6 incidents per year, hardly an appreciable difference. Instead, it’s more likely that our perceptions of apparent stability were due to the fact that most incidents during the Cold War years were viewed through the prism of the superpower struggle, even though they were often more complicated. After the Cold War ended, incidents had to be examined using other parameters which tended to show the complexity of the “real world.” A trend we are noticing in the U.S. is that, in the absence of the Cold War, Americans are becoming more jaded about the superpower role and U.S. military involvement in global incidents. Politically, it was easier to motivate the populous to act when the action could be couched in Cold War terms.

The Problem with Inductive Lessons

Based on what we have observed from the post-WWII era, what mistakes could political leaders and investors make?

During the post-WWII era, we never had a rising power threaten the established order. The U.S. and the U.S.S.R. generally managed their respective spheres and neither was faced with competitive powers within their groups. The U.S. fostered the economic recoveries of Germany, the U.K., Japan, Italy and France. However, American policymakers generally didn’t allow these nations to fully run independent foreign policies. For example, when France and the U.K. tried to oust Egyptian leader Gamal Nassar during the 1956 Suez Crisis, President Eisenhower stepped in to prevent that from occurring. In similar fashion, the Soviets put down a couple of rebellions in the Eastern Bloc in the 1950s and 1960s. During this era, there was no situation resembling the Thucydides’s Trap.

The same cannot be said about the current situation. The rise of China could create conditions similar to what Britain and Germany faced prior to WWI. Thus, the pattern of superpowers avoiding direct confrontation may not hold in the emerging post-Cold War world.

The previous patterns were determined with an established superpower. If the U.S. decides that it cannot, or will not, continue this role, then all the “lessons learned” from the previous 70 years won’t necessarily work going forward. These lessons would include the correlations and patterns observed in financial and commodity markets. For example, the U.S. has generally protected the Middle East from outside powers since 1945. In addition, the U.S. has also acted to stabilize conflicts from within the region. America’s actions have had a clear impact on oil prices. It would be reasonable to assume that if the U.S. reduces or ends this involvement, then oil price behavior will likely change. Similar factors exist in the debt, equity and foreign exchange markets.

Ramifications

WWI was an epic tragedy that changed the trajectory of world history. Unresolved issues from that war, including a fading superpower in Britain and a reluctant emerging superpower in the form of the U.S., contributed to financial and geopolitical instability, reduced globalization and, eventually, a global depression. The resolution ended with WWII. Going into WWI, there is very little evidence that European leaders or any contemporary thinkers were prepared for the carnage that followed.

In this report, we examined some of the historical interpretations that tried to explain why the war occurred. From this analysis, we moved to discuss the issues of induction; although this process is unavoidable when performing market analysis, analysts and investors need to be aware of the limitations of this approach. We concluded by drawing on the lessons learned from the past 70 years, including the caveats that the insights derived from the past seven decades may not hold as the world evolves.

Bill O’Grady

August 11, 2014

1The American Civil War is generally considered the first industrial war, due to its heavy use of railroads and the introduction of armored steamships (e.g., the U.S.S. Monitor).

2Simmons, Beth A. Who Adjusts? Princeton, NJ: Princeton University Press, 1994. Page 19.

3 Keynes, John Maynard. The Economic Consequences of the Peace. 1920. Excerpt:

The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep; he could at the same moment and by the same means adventure his wealth in the natural resources and new enterprises of any quarter of the world, and share, without exertion or even trouble, in their prospective fruits and advantages; or he could decide to couple the security of his fortunes with the good faith of the townspeople of any substantial municipality in any continent that fancy or information might recommend. He…could dispatch (sic) his servant to the neighboring office of a bank for such supply of the precious metals as might seem convenient, and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference. But, most important of all, he regarded this state of affairs as normal, certain, and permanent…The projects and politics of militarism and imperialism, of racial and cultural rivalries, of monopolies, restrictions, and exclusion, which were to play the serpent to this paradise, were little more than the amusements of his daily newspaper, and appeared to exercise almost no influence at all on the ordinary course of social and economic life, the internationalization of which was nearly complete in practice.

4Tuchman, Barbara. The Guns of August. New York, NY: Random House, 1962.

5Clark, Christopher. The Sleepwalkers: How Europe Went to War in 1914. New York, NY: HarperCollins, 2012.

6Estimated prior to 1870 to include the regions that became Germany.

7www.systemicpeace.org/warlist.htm

8Taleb, Nicholas Nassim. The Black Swan. New York, NY: Random House, 2007.

9A chicken believes humans are kind and supportive. They provide food, shelter and protect the bird from predators…until that unfortunate day when the owner decides chicken will lead the menu. From an inductive reasoning standpoint, until that fateful day, the chicken has no reason to believe that humans are anything but supportive.

10Op cit, www.systemicpeace.org.

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

© Confluence Investment Management LLC

© Confluence Investment Management