Key trends include Asian credit supply, which is on track for another record year in 2014, and China's priority to promote cleaner and more efficient energy.

Our bottom-up research and careful risk assessments – informed by macroeconomic perspectives – have us favoring select investments in several sectors of Asian credit markets, including state-owned enterprises in China and Korea, investment grade new issues and Basel III Tier 2 bank capital bonds.

State-owned enterprises: varying capital discipline, potential restructuring

Many state-owned enterprises (SOEs) in China and Korea are working to delever balance sheets and optimize cash flow. In March 2014, CNPC, China’s largest oil producer, reported a 10% year-over-year decrease in total capital expenditures in 2013 and plans for another 7% cut in 2014. Similarly, Sinopec is proposing to divest up to a 30% minority stake in its marketing segment.

China also laid out its latest SOE reform plan in late 2013, aiming to improve management and allow the private sector to participate in areas that SOEs previously monopolized. While we believe this restructuring initiative is a long-term positive, there could be short-term pains. For example, the liberalization of water and natural gas prices would likely benefit the SOEs operating in those sectors, while deregulation in telecom and banking could bring more competitive pressure to the incumbent SOEs.

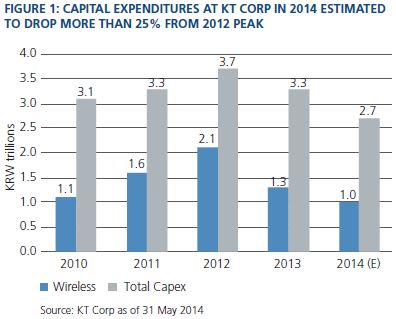

Korean SOEs, under a government mandate, aim to slow their overseas M&A activities and keep leverage in check. For instance, Korea National Oil is focusing on organic growth, Korea Resources looks to optimize its portfolio of mining holdings and KT Corp is lowering capital expenditures (see Figure 1).

By contrast, major SOEs in India, Indonesia and Sri Lanka are increasing leverage, albeit from a low base. ONGC, India’s largest oil and gas upstream company, recently raised 4.8 billion USD, while Pertamina raised 1.5 billion USD from the offshore debt market to fund its overseas investments.

These trends will likely affect net supply in the USD offshore bond market, with North Asia supply largely driven by refinancing and South Asia supply largely driven by capex. Overall, our bottom-up analysis continues to favor SOEs with high strategic importance, favorable industry trends and sound corporate governance.

Default trends in China onshore credit market

After a decade of rapid growth (see Figure 2), China’s bond market – at 30 trillion CNY (roughly 5 trillion USD) – is now the third-largest after the U.S. and Japan. Even more dramatically, credit bonds (i.e., bonds with default risks, such as corporate bonds and state enterprise bonds) constituted 49% of new issuance in 2013, up from just 2% in 2000.

Performance for China’s enterprise bonds and corporate bonds tends to be rate-driven, making it sometimes difficult to differentiate among credits. However, recent defaults have highlighted how overall risk profiles of Chinese corporates may be deteriorating as they re-leverage. That said, we believe the overall impact of defaults on the financial system will be limited at this point, with potential default candidates likely limited to small, mostly privately owned, companies.

In the event of default, offshore investors holding USD-denominated bonds issued by Chinese onshore companies should analyze the regulatory hurdles (court and regulatory systems, repatriation procedures) and corporate controls (gaining control of and divesting assets). Offshore bond investors face potentially very low recovery rates, and therefore need to be appropriately compensated for the risk. Bottom-up analysis is key.

Clean energy demand

With pollution now a widespread concern in China, promoting cleaner and more efficient energy is a high priority for the government, which intends to raise the share of natural gas in the primary energy mix from 5% in 2012 to over 8% in 2020. (Currently, coal makes up approximately 70% of the mix.) Natural gas is already competitively priced relative to liquid fuels and electricity, and local governments are beginning to promote the coal-to-gas switch. For instance, Beijing aims to shut down all coal-fired power plants and build four natural-gas-fueled thermoelectricity centers by 2017. Also, China’s recent gas purchase agreement with Russia should help satisfy China’s growing gas demand. Overall, we expect this trend to benefit global producers who can export gas economically to China (where demand already outpaces production – see Figure 3) along with select upstream SOEs.

In India, LNG (liquefied natural gas) import volume expanded significantly in the last few years as domestic production disappointed and demand rose. The country plans to more than double its total LNG regasification capacity to 55 million tons per year by 2018. The power and fertilizer sectors consume over half of India’s natural gas, and the high current demand has led to high price elasticity and resistance to further price increases (in April, a proposed nationwide gas price hike failed to kick in). Overall, the pricing, demand and consumption patterns have us cautious about natural gas as a source of clean energy in India.

Bank capital: details matter

Basel III Tier 2 (B3T2) bonds are still a relatively young and fast-growing asset class in Asia and are increasingly turning to the dollar-denominated market (see Figure 4). Asian B3T2 structures are generally vanilla and consistent with Basel III standards, with contractual PONV (point of non-viability definitions, i.e., mostly full or partial principal write-offs). This is unlike many jurisdictions in the West that have resolution regimes and where loss absorption can be taken based on statutory PONV.

New issue trends: bigger supply, new investors

Asian credit supply remains on track for another record year in 2014, with potential to reach nearly 150 billion USD at its current pace. Total market size could hit 1 trillion USD in the next three years. China alone accounts for over 50% of new issues. Despite some supply fatigue (meaning wider new issue premia for new deals), the fundamental backdrop remains very constructive for Asia and we expect issuers will continue to advance any refinancing and funding plans.

The key driver of growth has been disintermediation of the loan market, which is supported by increased demand from a wider investor base. Global (especially U.S.) accounts remain underinvested in Asia, and many are looking to add exposure. The local investor base – especially insurance, pension funds and sovereign wealth funds – is also increasingly participating in new issues.

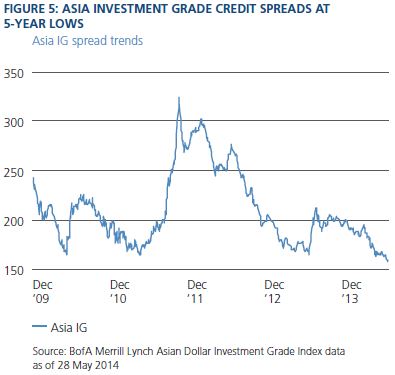

The pattern of issuance is adapting to the demands of these investor bases. Firstly, we see increasing investment grade (IG) issuance YTD relative to high yield (HY), although IG spreads are at their tightest in five years (see Figure 5) – yet they remain above their five-year average versus U.S. IG spreads (see Figure 6). HY spreads, meanwhile, remain far from five-year tights. Secondly, we see a trend toward high quality shorter-tenor floating-rate notes, a segment strongly supported by U.S. investors, and perpetual bonds, a yield-focused sector supported by retail investors. Thirdly, while there is continuous growth of first time issuers, their percentage within overall issuance has dropped, possibly as the changing investor base leans toward repeat issuers. Finally, currency trends support issuers who want to diversify investor bases.

High yield themes: tread with caution

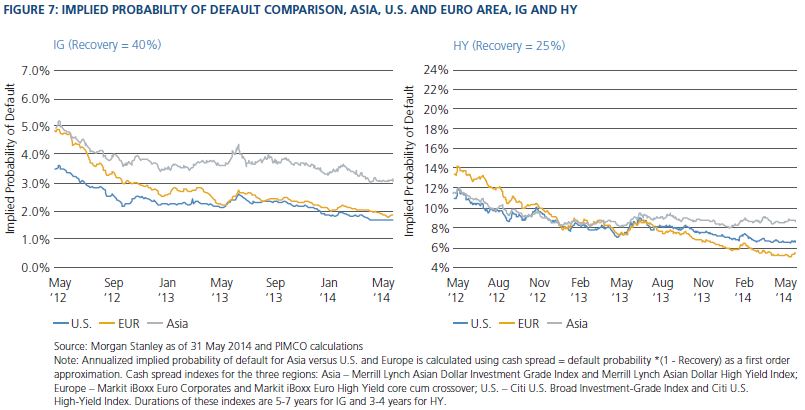

The overarching secular theme for Asian high yield is the search for yield. Investors may need to revisit estimated future default rates and recovery assumptions, which may rely too much on expectations of a “China Government backstop” – note, for example, recent high-profile defaults in the onshore debt market. Assuming the same recovery rate, Asia IG and HY credits show higher implied default probabilities than U.S. and European credits given historical spreads (see Figure 7). While the gap between Asia IG and U.S./Europe has largely stayed the same since mid-2013, Asia HY has underperformed with a wider gap versus U.S./Europe HY as China’s property sector weakened. This combined with overall slowing growth supports our view that spreads still have scope to widen from current levels. Caution is warranted, and we focus on bottom-up analysis to segregate the winners. We look for strong fundamentals, stable business models, potential to generate free cash flow and ability to keep leverage in control, especially in periods of liquidity stresses. We prefer sectors with secular growth outlooks, strategic importance, a sustainable competitive edge and a stable regulatory regime.

Investment implications

At PIMCO, we anchor our investments along these major credit themes, focusing on bottom-up research and careful risk assessments informed by thoughtful macroeconomic perspectives. In 2014, our views have us targeting select opportunities in state-owned enterprises in energy and utility sectors, investment grade new issues and B3T2 bonds.

The authors wish to thank Taosha Wang, Yishan Cao, Takanori Miyoshi and Abhijeet Neogy for their contributions to this article.

A word about risk: Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2014, PIMCO.

© PIMCO