N.B. Due to the upcoming Independence Day holiday, the next report will be published July 14, 2014.

As is our custom, we take the middle of the year to reflect on the current geopolitical situation. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for the rest of the year. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

#1: America’s Strategic Drift

This issue has dominated our thinking for the past several years. As we have noted in the past, the U.S. has and continues to struggle with creating a workable foreign policy since the end of the Cold War. For all its troubles, the Cold War brought focus; communism had to be contained and all foreign policy decisions had to pass that test. Even though there were policy disagreements during this period, the general requirements of defending the Free World were a strategic constraint for all administrations from Truman to G. H. W. Bush. Although we have discussed this condition in all of our outlooks and updates in recent years, we must admit that events of the past few months have led us to fear that this strategic drift is accelerating and becoming a serious threat sooner than we expected.

What are the missing elements for continuing America’s superpower status? Primarily, there has been no clear definition of policy goals. The Hamiltonian realism of the Cold War years has mostly been jettisoned; the last instance was the First Gulf War. In its place, there have been two policy themes. First, there has been a tendency for Wilsonian intervention. The incursion into Kosovo and Somali would fall into this category. The second was a form of Jacksonian policy[1] in the aftermath of 9/11. This led to the Afghan and Iraqi Wars (although it is arguable that the latter was mostly Wilsonian). However, these two policy themes have failed to address three key issues for the continuation of the superpower role.

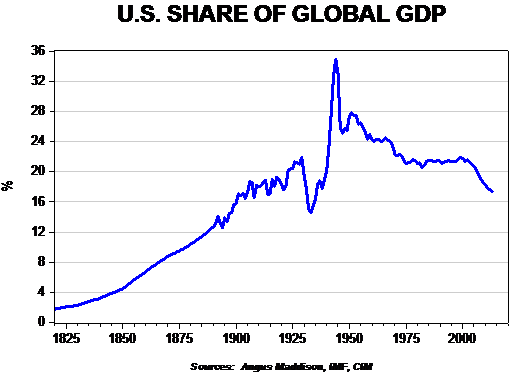

Relative Decline in Economic Power: At the end of WWII, American GDP represented 35% of global GDP. That percentage has declined to 17% in recent years.

The steady rise of China (currently around 14% of global GDP) and the 2008 Financial Crisis has reduced the relative dominance of the American economy. If the U.S. was not the superpower, this decline would not be critical. However, part of the financial element of the superpower role is to provide the global reserve currency. That position requires the U.S. to take on the role of global importer of last resort, meaning that the U.S. must run a persistent trade deficit in order to provide global liquidity. This requirement distorts the U.S. economy, creating a situation where the U.S. over-consumes. To create this consumption, the U.S. has implemented two broad policies. The first, which ran during 1932-78, was based on creating an egalitarian society. Through fiscal and tax policy, the U.S. built an economy that created a plethora of high-paying, low-skilled jobs. Although this policy was effective in supporting consumption, it was also rather inefficient and led to persistent inflation in the 1970s. In 1978, President Carter began the process of reversing that policy to one of greater efficiency. Through the policies of deregulation and globalization, the economy restrained inflation. However, this occurred by destroying all those high-paying, low-skilled jobs, leaving the mass of Americans struggling to maintain the necessary consumption to meet the reserve currency role. In order to support consumption, the economy expanded lending, leading to the massive debt bubble which collapsed in 2008.

Clearly, policymakers have not resolved this issue. In fact, it does not have an easy solution. However, maintaining the superpower role will be impossible unless the U.S. can develop a method to maintain high levels of consumption without triggering either inflation or excessive debt. The most likely solution is a guaranteed income, a sort of “Social Security for all” that would allow the economy to maintain its efficiency without supporting consumption through debt. At present, such a policy seems unlikely.

Lack of Policy Focus: During the Cold War, the U.S. had to focus on the communist threat. All other dangers paled in comparison. Since the end of the U.S.S.R., the U.S. has not been able to prioritize its geopolitical goals. The Clinton administration’s primary goal seemed to be to extend the “Washington Consensus” on expanding trade, democracy and markets, although the tactics to further this goal were rather ad hoc. The Clinton administration did act strongly during the Asian Economic Crisis and the Russian Debt Default but also acted in Kosovo for what appeared to be purely Wilsonian reasons. The Bush administration was consumed with terrorism, treating it as a mortal threat equivalent to communism. However, in retrospect, it likely overestimated the threat due to the 9/11 tragedy. President Obama has tried to reduce the U.S. role to a more manageable level. He exited from Iraq (which isn’t working out well) and will exit Afghanistan too. He did initially signal a “pivot” to Asia but that strategy appears to lack any tactical structure. In fact, as we will note below, unfortunately, he has created the appearance that the U.S. is in a headlong retreat from the hegemon role.

At this point, there is no single policy goal that the U.S. can point to which is critical. Without a focus, policy becomes ad hoc and disjointed.

Lack of Domestic Unity: During the Cold War, the political elites were able to execute a domestic policy that kept most voters behind the nation’s geopolitical goals. In the 1932-78 policy regime, the majority of Americans benefited from the high-paying, low-skilled jobs policy mix. But even after that policy changed, the policy elites were able to keep most voters on board with the Cold War foreign and domestic policies. However, as the Cold War fades into the distance of history, the issues that were ignored when creating this policy have returned.

America was formed as a republic. Although the founders generally wanted a moderately powerful executive (there was actually a substantial debate on this issue in the Federalist Papers), the basic position was that a too-powerful president would eventually lead to tyranny. Unfortunately, it is virtually impossible to be a superpower and have a weak executive. Thus, since 1945, the office of the president has steadily increased in power; for example, all wars fought since WWII have been conducted without formal declarations of war. The U.S. didn’t have a substantial standing army prior to WWII, nor did it have intelligence agencies. The U.S. prior to its acceptance of the superpower role was a republic with a small government. That is clearly not the case today.

As we detailed in our three-part report on the 2016 elections,[2] significant portions of the electorate have tired of the burdens of hegemony and want to relinquish the role. The establishment wings of both parties, who have benefited greatly from globalization and deregulation, are fighting to fend off electoral threats from the populist wings of their parties. We tend to view this political fight as a battle over the decision to end or continue the superpower role.

And so, the rest of the world looks at the indecision coming from the U.S. and is trying to adapt to this new world. Probably the best way to frame this issue is to understand that a number of potential conflicts worldwide have not occurred because U.S. hegemony prevented them from occurring. If U.S. hegemony is ending, these “frozen wars” will likely thaw.

#2: Chinese Maritime Expansion and the Reaction of its Neighbors

As China’s economy reaches large country status, it is trying to expand its influence in the surrounding coastal waters. This has led to persistent tensions with Vietnam, Japan and the Philippines. Although China does not have a true “blue water” navy, with increasing frequency it has been “bullying” its smaller neighbors.

Underlying China’s behavior is an unresolved conflict with Japan. The latter invaded China in 1931 and held parts of Chinese territory until the end of WWII. The U.S. ended Japan’s threats to the region by demilitarizing the country and installing a pacifist constitution. Although China still resents Japan’s invasion (and the former has a myriad of other historical grudges against the West as well), as long as the U.S. was in place to prevent Japan from reclaiming its regional power status, China was generally content to grow its economy and benefit from global economic expansion.

However, as the perception of U.S. decline accelerates, China is moving rapidly to claim regional hegemon status. It isn’t obvious whether China has the military capacity to fulfill this role, especially if the U.S. supports its neighbors. Additionally, India and Japan have their own military forces which are not trivial. But the key point is that as the rest of the world concludes the U.S. is a fading power, this potential conflict is steadily coming closer to an actual one.

#3: The German Problem

As the U.S. begins to withdraw from hegemony, the issue of controlling Europe, which is essentially the German Problem, is returning. Germany is dominating the Eurozone economy, raising concerns among its neighbors that it is becoming a hegemon. The geographical area that Germany controls is destined to make the country an economic powerhouse. At the same time, it has no natural defenses, meaning it is vulnerable to attack from its neighbors. Thus, Germany has historically been a strong, but fearful, nation.

The rise of Germany is what ostensibly led to WWI, which began about a century ago. Germany’s industrialization threatened British economic hegemony and was a military threat to both France and Russia. In response to these concerns, Europe created a web of treaties. The assassination of the Austrian Ferdinand, the presumptive crown prince, by Serbian terrorists triggered a cascade of events that led to WWI. In the aftermath of the war, European leaders tried to contain Germany through the Treaty of Versailles. However, the treaty turned out to be a monumental mistake—it was harsh enough to evoke German hatred but not harsh enough to prevent its recovery and remilitarization. Germany retaliated during the Nazis’ rule; their aggression led to WWII. The allies from this war did not make the mistakes of WWI; Germany was thoroughly vanquished and dismembered. West Germany became part of NATO, while East Germany was part of the Warsaw Pact.

In a fashion similar to U.S. policy toward Japan, Germany was demilitarized and, in fact, occupied by American troops for decades as a protection against Soviet expansionism. However, with the end of the Cold War, Germany was reunited. To date, it remains a minor military power with a deep reluctance to accept a “hard power” role.[3] During its period of division, Germany, like Japan, focused on economic development. It has become the dominant economy in Europe. In the recent Eurozone crises, Germany has essentially dictated terms to several deeply indebted nations in Europe. Although Germany is not a military power, its economic power gives its formidable influence.

At the same time, as Germany begins to deal with its power, it is finding that merely following U.S. or French foreign policy isn’t necessarily in its best interests. For example, during the Ukraine crisis, Germany’s behavior has been more favorable to Russia than Western Europe or the U.S. expected. However, from Germany’s perspective, being allied with Russia is important; it receives natural resources from Russia and Germany isn’t comfortable with the NATO promises being extended into Eastern Europe.

We expect Germany to become increasingly independent of U.S. foreign policy aims. Germany’s behavior will likely increase tensions within NATO and the G-7. However, we view this as a direct consequence of the power vacuum developing due to U.S. behavior.

#4: The Remaking of the Middle East

The current boundaries in northern Africa and the Middle East were mostly drawn by colonial powers. The borders were best suited for these European nations to maintain control. Ethnic and religious groups were often divided and minorities tended to be put in power by colonialists to ensure loyalty. As independence emerged, the new rulers tended to keep the same borders in place, fearing that allowing them to reach their natural state would invite chaos. However, most of the governments became authoritarian in order to maintain these artificial states. That was the only way to maintain order.

The Arab Spring has unleashed a wave of democracy movements that have, thus far, been fraught with risk. In Egypt, the military has reasserted control after an Islamic government was ousted in a coup. Civil conflict has emerged in Syria, Libya and Iraq. Libya may devolve into at least two, or perhaps three, separate nations. Syria is effectively partitioned, and Iraq, with the development of ISIL, is rapidly splitting into three parts.

There is still great potential for ongoing insurgencies and civil conflicts that are essentially ethnic and sectarian. The Europeans experienced this situation with one of the bloodiest wars of the 17th century in the Thirty Years’ War, which was mostly sectarian. As U.S. influence declines in the area, the odds of serious conflict will likely rise.

Ramifications

If the U.S. continues to withdraw from its superpower role, we would expect two major market effects. First, commodity prices and Treasuries prices would probably benefit. Second, in what may be the biggest surprise, U.S. real and financial assets would likely rally as well. As foreign conditions deteriorate, overseas investors would look to protect their wealth by moving funds to the U.S. We would expect a steady flow of capital flight to support U.S. asset prices. Foreign markets, on the other hand, may be particularly risky.

The current situation may change with a new president in 2016. However, as we noted in our reports on that election, it may also solidify the end of U.S. hegemony. Thus, we would expect the geopolitical situation to become increasingly fluid over the next 18 months.

Bill O’Grady

June 30, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[1]For a broader discussion of American foreign policy, see WGR, The Archetypes of American Foreign Policy, 1/9/2012.

[2]See WGRs: 2016 Part 1, 3/31/2014; 2016 Part 2, 4/14/2014; and 2016 Part 3, 4/21/2014.

[3]However, this stance is being questioned. See WGR, The Return of Germany, 2/10/2014.

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

© Confluence Investment Management