- Smart beta is increasingly important when returns are likely to fall short of what most investors need and expect.Â

- Active managers can use multiple tools to help generate higher returns.Â

- With outcome-oriented strategies, investors can align their portfolios toward meeting specific risk and return objectives.Â

- Investors with more aggressive income or return needs may benefit from bespoke, multi-asset solutions. ​Â

The world’s economies have been operating in a lower gear since the financial crisis, constrained by high debt levels, unfavourable demographics and a pendulum shift toward reregulation, with the result being subpar recoveries and much lower growth relative to prior cycles. Yet many investors have been handsomely rewarded during this period, thanks to hyper-aggressive central bank policies, including direct asset purchases, which have pushed government bond yields to new lows and equities and other risk assets back toward record highs. There were certainly potholes along the way, most notably Greece and the other European peripherals during the heart of the eurozone crisis, not to mention last year’s Federal Reserve-induced ‘taper tantrum’. Indeed, these are all straight out of the New Normal playbook, which we first introduced in 2009, with structural impediments to global growth, speed bumps, S-curves and potential T-junctions all being part of the mix.

Are we past the extremes? We think so. In fact, at PIMCO’s latest Secular Forum where we look three to five years down the line, our global team of investment professionals called for an outlook we term The New Neutral: As detailed in our most recent May 2014 Secular Outlook, we still see structural headwinds, multi-speed economies and restrained, New Normal-style growth in the years ahead. This means that, even as they move toward policy normalisation, the Fed, the Bank of England (BoE), the European Central Bank (ECB) and other major central banks will target New Neutral real policy rates closer to zero rather than the normal 1%–2% that’s currently priced into the markets.

Bond and equity market returns will likely average a more modest 3%–5% in this environment, though risks will be lower as well. This doesn’t signal an end to volatility; it just means bond yields are unlikely to increase much above current forward rates, while equities and other risk assets remain relatively range-bound. So what’s an investor to do in this environment?

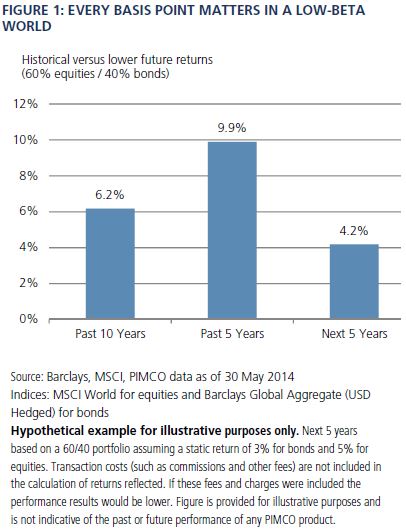

Be smarter about beta

This should be a statement of the obvious, though many still view ‘smart beta’ as a clever marketing ploy rather than as a serious investment strategy – who, after all, would ever invest in ‘dumb beta’? Yet in a world of lower expected market returns, or beta, every basis point matters. Just look at Figure 1, which compares historical returns on a 60/40 blend of global equities and bonds over the past 10 and five years with a lower future return 60/40 blend portfolio we are more likely to see over our secular horizon. The analysis is simplistic, but our concern is that future returns will not only be lower than in the recent past but will also fall short of what most investors need and expect.

Â Â

Â

Smart beta comes in several forms. For many, it means creating more targeted benchmarks or portfolios that exclude certain countries, sectors or issuers that are perceived as either being too richly priced or having excessive risk. This is obviously an active decision and one that needs to be regularly revisited. But we’ve seen a number of examples of this over the years: global bonds ex Japan (yields too low), emerging markets ex Argentina and other countries (volatility too high), corporates ex financials (post-Lehman concerns) and European governments ex peripherals (eurozone crisis). And we’re currently seeing a variation of this in the UK, with pension funds de-risking out of equities into diversified, low-turnover ‘buy and maintain’ credit portfolios structured to achieve specific yield targets while actively avoiding securities with default risk.

The second means to a smarter beta is through the use of derivative-based overlay strategies, which combine beta-replicating futures or swaps with an underlying portfolio of cash and/or other securities. This is a common approach for pension funds employing LDI (liability-driven investment) techniques, with long duration swaps providing the liability hedge and cash equivalents, short duration bonds or an absolute return portfolio providing the backing. And it’s also one that has been successfully applied over the years to a number of other markets, including equities and commodities. The approaches can vary, ranging from simple beta replication, with the derivative positions being backed by pure cash; to enhanced beta, or ‘portable alpha’, with the derivatives being backed by an alpha-focused portfolio of cash equivalents and short duration bonds; to higher-return-seeking forms, with derivatives backed by more aggressive alpha-focused portfolios. But, in all cases, the underlying objective is to create a better, if not higher returning, form of beta.

The third and perhaps purest means toward a smarter beta is simply to adopt more forward-looking benchmarks. There are literally dozens, if not hundreds, of widely available benchmarks across the various asset classes, some very straightforward, others more complex. Yet most come with the same inherent disadvantage: They are backward-looking and market-capitalisation-weighted. For fixed income investors, this pushes allocations more toward countries, sectors and issuers with high and growing amounts of debt as opposed to those with healthier balance sheets – which, other than for liquidity reasons, makes little sense. For equity investors, this forces a momentum-driven approach with larger allocations to countries, sectors and issuers that have already increased in price and correspondingly smaller allocations to those where prices have already fallen – which, again, seems counterintuitive. In both cases, we believe investors would be better served by adopting smarter, more forward-looking benchmarks – using, say, GDP-weighted indices for bonds and more fundamentally driven indices for stocks.

Take advantage of active management

Investors face a stark choice in a world of 3%–5% market returns: They can go active, employing a multitude of tools in an effort to generate higher returns; or they can go passive, essentially locking in ‘beta-minus’ net of fee performance. Active management obviously comes with risks – even the best managers will experience periods of underperformance. Yet passive has risks too, particularly in this environment where ‘beta-minus’ in a low-beta world is unlikely to meet most investors’ return needs. We obviously come at this as an active manager – and I, having spent 28 years with the firm, have active in my blood. But, if ever there was a time for active management, this is it.

By going active, investors can:

-

Maximise flexibility to play both ​offence and defence in a multi-speed world. Top-down choices of which country, currency or sector, or, more specifically for fixed income investors, what part of the yield curve to target, are highly dependent on relative growth rates, inflation levels, policy actions and valuations. This is not a world where one size fits all – which offers clear advantages for active management.

-

Benefit from bottom-up credit and stock-picking skills in a world of slower yet differentiated growth. Credit and underwriting cycles are at varying stages depending on where you look, with company/issuer fundamentals, relative value across similar companies/issuers, including for credit, the currency of issue, and optimal choice within the capital structure all being extremely important determinants of performance in this environment. And only active management can capitalise on these factors.

-

Seek value in some of the more complex or credit-intensive markets, such as non-agency mortgages, high yield, bank loans and bank capital, where a deep understanding of the underlying collateral, covenants and other provisions is critical to assessing risk and potential reward. These riskier, less liquid sectors – which either are, or should be, off-limits to passive investors – can offer above-average return potential for active managers with the resources and expertise to weed out the increasing issuance with “lite†or “zero†covenants or other overly risky debt.

-

Guard against spikes in volatility, through direct or indirect hedges, and then take advantage of such spikes by adjusting over- and under-weights accordingly. Though we see fewer potential large, ‘left-tail’ risks in our secular horizon, historically low levels of current implied market volatility leave plenty of room for even minor surprises. And while the effects may wash out over time, there is potential for value that only active management has the opportunity to capture.

Focus more on outcomes

Investing for market beta is a great strategy when market returns are strong and even better when risk markets are leading the way. Pensions become more fully funded, return-driven investors get amply rewarded and those with income need have little problem meeting their requirements. Most everyone is happy, as long as they’re fully invested, with markets being the dominant driver of overall performance and alpha generation being viewed as an important, though secondary, factor.

Investors have clearly been shifting toward more outcome-oriented approaches in recent years, with more pensions embracing LDI and others choosing absolute return, real return or income-seeking strategies as part of their overall allocations. In a world of lower expected market returns, where beta can no longer be all things to all investors, emphasizing outcomes becomes even more important. Whether this means generating income, absolute or real returns, hedging liabilities, inflation or tail risk, or managing liquidity, investors will need to align their portfolios much more toward meeting their specific risk and return objectives.

Consider bespoke, multi-asset solutions

For some investors, a greater focus on outcomes will only mean minor tweaks to their overall strategy and allocations – such as adding a little more income, modest amounts of risk or additional hedges – which can be accomplished fairly easily. But for others, depending on their objectives, particularly for those with more aggressive income or return needs, moving to more bespoke, multi-asset solutions may be the better, if not necessary, route. These would be highly targeted portfolios, designed to meet specific income, absolute or real return, hedging and liquidity needs, with well-defined parameters for controlling risk and volatility. An income-seeking investor, for instance, would want a solution emphasising core fixed income, diversified credit and income-oriented bonds and equities, with specific allocations depending on agreed-upon income targets and acceptable levels of volatility. An investor looking for returns, on the other hand, would need a solution more geared toward absolute return fixed income and credit, smart beta global equity and opportunistic strategies – again, with allocations subject to specific return and volatility targets. Multi-asset solutions aren’t for everyone, but they can help.

In summary

We expect below-trend, New Normal growth to continue for the world’s economies over our three- to five-year secular horizon – which, in turn, means global central banks will target a New Neutral for real policy rates well below the historical norm. Given current market valuations, slower growth implies more modest returns for investors in the years ahead. The good news is risks and volatility should be lower as well, given reduced ‘left-tail’ risk and the fact that markets are currently pricing in higher, above-New Neutral real policy rates. Though this should help mitigate the downside risk for both fixed income and equity markets, investors will still face significant challenges meeting their income and return objectives in this environment. Being smarter about beta, taking advantage of active management, focusing more on outcomes and considering bespoke, multi-asset solutions will be increasingly important strategies as investors get into gear for The New Neutral.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investors should consult their investment professional prior to making an investment decision. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Investors should consult their investment professional prior to making an investment decision.Â

Return assumptions are for illustrative purposes only and are not a prediction or a projection of return. Actual returns may be higher or lower than those shown and may vary substantially over shorter time periods.Â

No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Hypothetical or simulated performance results have several inherent limitations. Unlike an actual performance record, simulated results do not represent actual performance and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated performance results and the actual results subsequently achieved by any particular account, product or strategy. In addition, since trades have not actually been executed, simulated results cannot account for the impact of certain market risks such as lack of liquidity. There are numerous other factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect actual results.Â

Barclays Global Aggregate Index provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. The index also includes Eurodollar and Euro-Yen corporate bonds, Canadian Government securities, and USD investment grade 144A securities. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 24 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. It is not possible to invest directly in an unmanaged index.Â

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2014, PIMCO.

© PIMCO