Russia’s international behavior has become steadily and increasingly belligerent. From the 2008 incursion into Georgia to the seizure of the Crimea and the destabilization of eastern Ukraine, a strong case can be made that Putin is trying to reassert Russia’s influence into his “near abroad.”

In recent weeks, we have discussed Russia’s behavior, Putin’s goals and the regional impact at length (see WGRs: 3/10/2014, Reflections on Ukraine; 3/24/2014, Will Putin Stop with the Crimea?; 4/7/2014, Russia and the Baltics; 4/28/2014, Putin’s Ideologist; 6/2/2014, From Russia, Without Love). However, to date, we have not discussed how the West may react to Russia’s actions. This report will address one potential response.

In this report, we will begin with a basic analysis of the oil markets. From there, we will examine Russia’s economic dependence on energy. We will offer a historical analysis of Saudi Arabia’s decisions in 1985 and 1997 to retake oil market share and the impact these choices had on the Soviet and Russian economy. Using this historical parallel, we will offer an example of how the U.S. could drive down oil prices in a bid to undermine Russia’s economy. We will analyze the likelihood that the Obama administration will use this potential weapon and the potential “collateral damage” its deployment might bring. As always, we will conclude with market ramifications.

The Oil Market

The critical factor that drives the current global crude oil market and has for at least the past 120 years is cartel-type behavior. Oil demand is generally steady, rising with global economic growth. At the same time, since oil is a necessity, the short-run demand curve tends to be inelastic, meaning the quantity demanded is insensitive to price. Because of this condition, small changes in supply can lead to outsized changes in price.

The supply side of the market tends to be “lumpy,” meaning that oil discoveries tend to come in waves. The development of an “elephant” field will tend to dramatically lift supply. Combined with the inelastic nature of demand, new oil discoveries can have a significantly adverse impact on prices. Clearly, the opposite case is true as well; small cuts in supply can lead to commensurately higher increases in prices, leading to higher revenue for oil producers.

The market structure of crude oil is conducive to cartel behavior. Having a group that controls supply growth tends to keep prices higher than a pure market would generate. At the same time, the higher prices usually lead to better field maintenance and more rational production policies. In addition, a cartel, in its bid to restrict supply and raise prices, deliberately creates a buffer of unused productive capacity. This tends to lower price volatility as this buffer will tend to be deployed during supply disruptions.

In effect, society trades lower price volatility and rational production policy for higher oil prices. Cartel behavior has been consistent from Rockefeller’s Standard Oil Trust to the Texas Railroad Commission to OPEC.

Managing a cartel requires some form of “muscle.” Rockefeller would use predatory pricing and legal maneuvers to control the production of rivals. The Texas Railroad Commission used government power to regulate production. OPEC uses regular meetings and the threat of lower prices to coerce compliance. The problem for the cartel is that by keeping prices higher than the market-clearing price, rival competitors are encouraged to increase production. Unless the cartel can use military or government power to force compliance (as the Texas Rangers did from 1931 into 1971), it is forced to occasionally flood the market with oil to drive down the price and threaten the higher cost producers with ruin. Assuming that the lower cost producers are in the cartel (which is reasonable, since they have the most to benefit from higher prices), these periodic attacks on “free riders” to the cartel are necessary to enforce price discipline.

Russia’s Energy Dependence

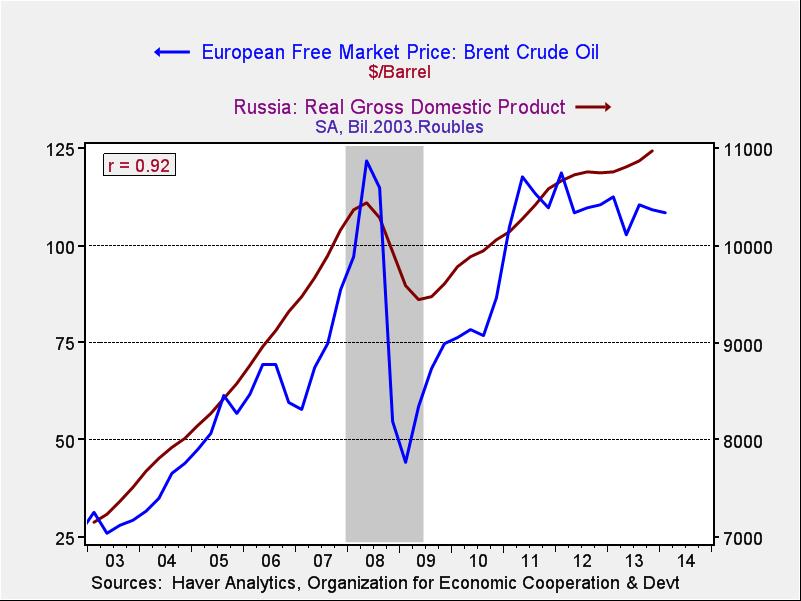

Russia’s economy is heavily dependent on natural resources; hydrocarbons represent about 30% of the country’s GDP and half of its growth since 2000.

This chart shows the relationship between the level of Russia’s GDP and the price of oil. The Russian political economy is heavily dependent upon oil and natural gas revenues. The Putin regime uses these funds to enrich the nation’s oligarchs, who support his continued rule, and government workers, which offers jobs to the masses. Russia’s former finance minister, Alexei Kudrin, estimates the Russian government needs a Brent price of $117 per barrel to meet its funding needs.[1]

About 67% of the country’s export earnings come from oil, oil products and natural gas exports, the majority of which are sold to Europe. Although Europeans have been criticized for their over-dependence on Russian energy, Russia is also vulnerable to European sanctions on energy; of course, getting Europe on board for sanctions would require making the actions as painless as possible for ordinary Europeans.

The Oil Weapon

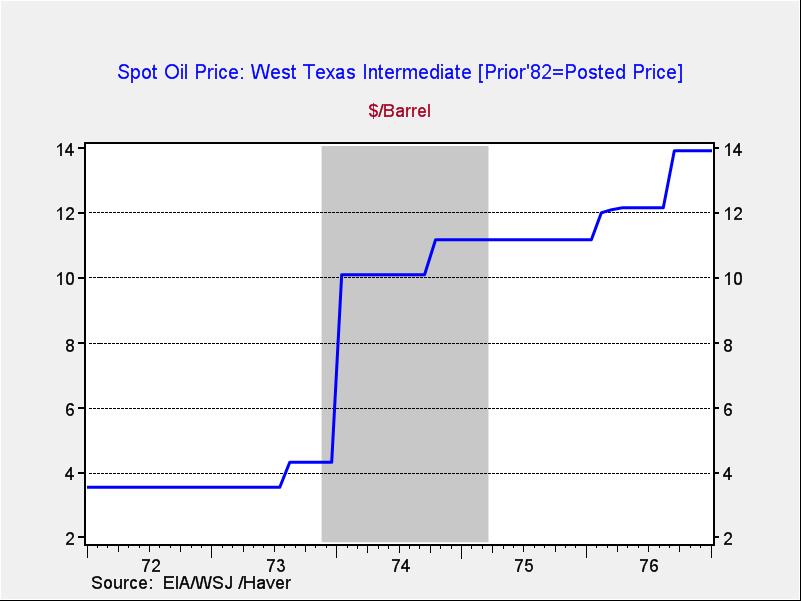

The term “oil weapon” was used liberally during the 1973 Arab Oil Embargo. After the Nixon administration resupplied Israel during the Yom Kippur War, the Arab nations of OPEC implemented an oil embargo. Prices rose significantly, rising from $3.50 per barrel in mid-1973 to over $10 per barrel by late 1974.

However, the embargo was generally considered, at best, a mixed success. The U.S. continued to support Israel despite the pain of higher oil prices. The embargo lifted the idea of oil supply insecurity in the minds of the American public and some policy steps were taken to lower consumption and support non-cartel production.

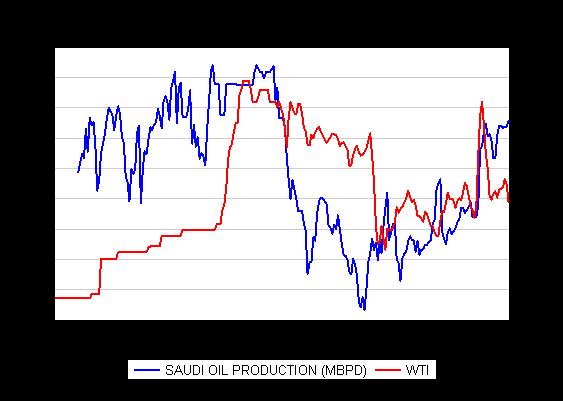

On two other occasions, Saudi Arabia used the oil weapon to lower prices. The first came in the mid-1980s. In order to manage oil prices, the kingdom had taken on the cartel role of “swing producer,” lowering its production in order to maintain a target price. By design, this allowed other producers to take market share away from Saudi Arabia. The kingdom, on several occasions, asked other members of the cartel and large non-OPEC producers to reduce output in a bid to maintain prices and protect Saudi Arabia’s market share. As one would expect, the Saudis did not receive assistance.

Thus, in late 1985, the kingdom began to flood the market with oil.

As the chart shows, Saudi production fell from over 10 mbpd in the early 1980s to around 2.5 mbpd by late 1985. As the Saudis ramped up production, oil prices eventually collapsed, falling from $30 per barrel to $12 per barrel. As other oil producers began to reduce output to allow Saudi production to recover, oil prices rose and order was restored in the oil market.

The impact on the Soviet economy was significant. The U.S.S.R. share of global exports fell from 10% to 4% in the period from 1986 to 1991. The aforementioned decline in price was around 60%; in today’s market, it would generate a comparable price of $40 per barrel for WTI. The drop in revenue to the Soviet Union was one of the key factors that severely harmed the economy and paved the way for the end of the Soviet state.

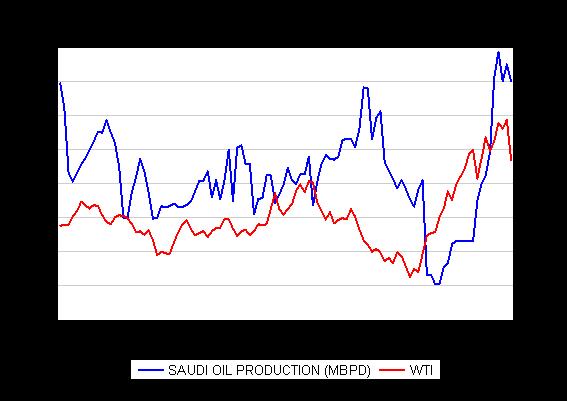

The second occasion occurred in the late 1990s. Saudi Arabia and Venezuela were locked in a market share war, specifically for the U.S. market. The Saudis, dependent upon the United States for military protection, had an unwritten policy of wanting to be the largest foreign supplier of crude oil. In late 1985, their rank had fallen to tenth. In 1997, it had declined to third, behind Canada and Venezuela. The latter had a deliberate policy of supporting foreign investment to boost oil output. In 1997, the kingdom decided to defend its market share and lifted its production from 8.1 mbpd to near 8.8 mbpd. Prices fell from $25 per barrel to just over $10 per barrel in 1997-98.

The timing of the Saudi decision was unfortunate; the Asian Economic Crisis began in May 1997 with speculative attacks on the Thai baht. By July, the region was in turmoil. Since this area had been a major source of incremental oil demand, prices began to decline even though the Saudis started to cut production in 1998. Clearly, the output reductions were not enough to support prices.

The drop in oil prices put tremendous strain on oil producers. Hugo Chavez signaled during the 1998 Venezuelan presidential elections that he would change the country’s oil policy—essentially, he was declaring a ceasefire. After Chavez won the elections, representatives of the new government and Saudi oil officials met and created a plan to lift oil prices. As part of this agreement, Saudi Arabia cut production from 8.2 mbpd to 7.6 mbpd in early 1999. These cuts allowed prices to recover.

This episode played a role in the Russian debt default in August 1998. Although the Russian economy had numerous problems, the drop in oil prices was a contributing factor in the Russian debt crisis.

The American Oil Weapon

One of the lessons from the post-WWII world is that the best guarantee against attack from another nation is the possession of nuclear weapons. Therefore, despite the fact that Russia’s recent incursions into Ukraine violate numerous treaties, the U.S. will not use military force to return the Crimea to Ukraine. Nor will the U.S. use military force to support Ukraine’s attempts to stabilize its eastern regions. Because Russia possesses nuclear weapons, the rest of the world is limited in its response to Putin’s aggression.

Simply put, sanctions and other economic tactics are the only way to retaliate against Russia. Sanctions will have limited effects; although banking sanctions would clearly harm Russia, it would likely also hurt European nations that do business in Russia. It would likely harm some U.S. companies as well. Political support is mostly lacking for effective sanctions.

But, as the history of the two Saudi programs’ attempts to regain market share shows, cutting oil prices can have a devastating impact on the Russian economy. The question is who could take such actions? The Saudis could, but there is little incentive for the kingdom to do so. Its market share remains high and prices are favorable to its revenue needs.

Surprisingly, it appears the U.S. actually has the capability of taking on this role. To some extent, the U.S. played this part from the early 1930s into 1971; America was the global swing producer that kept excess oil productive capacity offline to maintain prices and offer a supply buffer in case of emergencies. It is not well known, but OPEC implemented a supply cut in protest of the 1967 Six-Day War. However, oil prices did not rise despite the OPEC supply cut. The U.S. simply replaced all the oil that OPEC refused to supply. As the above history describes, the situation in 1973 was fundamentally different.

How can the U.S. deploy its oil weapon? There are two actions the U.S. would need to take to drive oil prices lower. First, the government would need to lift the 1970s-era restrictions on oil exports. Crude oil production is running around 8.0 mbpd at present and is rising about 0.9 mbpd per year. Adding natural gas liquids and biofuels would add another 3.5 mbpd of liquids. Although U.S. product consumption is 18.3 mbpd, a crude oil glut is developing at the Gulf Coast due to distribution issues. In addition, rising Canadian production is bottled up due to the indecision surrounding the Keystone pipeline which would add additional oil that would be available for export.

Second, the U.S. could couple the lifting of the oil export ban with a Strategic Petroleum Reserve (SPR) release. Currently, the SPR holds 691 mb of crude oil. As an IEA member, the U.S. is obligated to hold 90 days of import coverage in its SPR. Current commercial and SPR stockpiles hold 150 days of import demand, meaning the U.S. holds a 60-day surplus, approximately 430 mb. Although the SPR’s rated withdrawal capacity is 4.4 mbpd, a safer rate would be 1.2 mbpd, which would allow the latter amount to be exported daily for nearly one year.

What would these combined efforts bring in terms of price? Our ballpark estimate is around $75 per barrel for WTI, which would be close to Brent prices after the oil export ban is lifted. If Russia needs $117 per barrel oil to balance its spending needs, a $25 per barrel drop in crude oil would likely be severely damaging.

There is no doubt that a price drop into the $70s per barrel range of WTI would adversely affect the U.S. oil industry. The administration may need to craft a domestic price support program similar to how grain prices are managed. In effect, the U.S. government would agree to buy oil to refill the SPR at $80 a barrel for domestic producers only. Although this would be a hard sell politically, it would likely be necessary for the weapon to be effective.

Barriers to Implementation

There are three barriers to implementing the American oil weapon:

Offsetting OPEC response: In general, OPEC nations have seen a steady rise in the price needed to support their economies. Saudi Arabia would likely be reluctant to support America’s deployment of the oil weapon. First, due to rising transfer payments to quell unrest due to the Arab Spring, the kingdom needs around $85 Brent prices to achieve budget balance despite being the cartel’s low-cost producer. Second, current relations between the U.S. and Saudi Arabia can be graciously described as “frosty.” The Obama administration’s negotiations with Iran are a major sticking point for the kingdom. The danger is that OPEC could reduce its production to offset U.S. exports and SPR sales, keeping prices from falling. Although this may be hard for the entire cartel to take, the Saudis, if motivated enough, could cut production unilaterally to thwart U.S. efforts.

Incongruity with other geopolitical goals: Low oil prices will clearly harm Russia and the OPEC oil producers. However, it could be very supportive for Asian nations, including China. In effect, the U.S. would be selling American taxpayer-funded oil to indirectly benefit the Chinese economy. In addition, lower oil prices would harm some friendly, non-OPEC nations like Mexico, Brazil and Canada. Dealing with the Chinese situation will be difficult but we would expect a furious reaction from Mexico, Brazil and Canada who would be collateral damage and may need support. For example, Canadian compliance could be aided by approving the XL pipeline.

Lack of political capital: Although President Obama could use a significant foreign policy victory, using the oil weapon would require a great deal of finesse. The drop in crude oil prices should lead to lower gasoline prices which are always welcome by the U.S. public. However, selling SPR oil, which is owned in the high $20 per barrel level, to replace it with government-mandated $80 per barrel will be seen as a sop to the oil companies, which would be a difficult “sale.” Given the past year of administration “unforced errors,” such as the bungled release of the health care program and the recent Afghan prisoner swap, there are concerns that such a sophisticated program would be botched. Deploying an American oil weapon is a bold policy, one that this administration, in the twilight of its term, may simply not be able to implement.

Consequently, we doubt the Obama administration will go so far as to order a major SPR sale. However, we may very well see a lifting of the oil export ban which would have a positive effect on WTI and a bearish effect on global oil prices. However, this action probably won’t be enough to seriously damage the Russian economy. Overall, we doubt the administration views Russia’s threat as serious enough to spend its remaining political capital to push through this policy. On the other hand, for the first time since the late 1960s, the U.S. could take steps in the energy arena to further its geopolitical goals. This factor, by itself, is a significant change.

Ramifications

Although the U.S. has a potentially damaging tool to deploy against Russia, we doubt it will be fully implemented. We would expect the U.S. export ban to be lifted which would be a bullish event for WTI and domestic oil companies.

Bill O’Grady

June 9, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management