Our modern age is becoming more virtual than physical, which I find increasingly depressing if only because I’ve failed to keep pace. I don’t even own a cellphone. Still, it doesn’t take a Boomer to observe that the reality outside as opposed to inside a computer or a cellphone should be the preferred experience. Scientists claim we are all just bits of information with billions of 1’s and 0’s, glued together to form a beating heart. Even so, I’m sticking with live chirping as opposed toAngry Birds for now. Virtual reality seems just a tad UNreal to me.

Aside from a computer or cellphone’s obvious utility though, I think many of those in younger generations that use them are hoping to capture time in a figurative bottle, using a Samsung or Apple handheld as opposed to the proverbial wine-shaped container of another era as they take pictures. YouTube and Facebook apps, for example, record and memorialize events, creating a virtual history that can be preserved, with the most treasured experiences being measured in the millions of future hits as opposed to the euphoria or sometimes depressing succession of individual moments in the here and now. Watching a sporting event or concert, I can’t help but be struck by the thousands of cellphones attempting to capture, in near unison, a moment in time that can be texted to hungry audiences. Recipients seem eager for a seemingly unlimited number of experiences in their or someone’s immediate past, as opposed to the present moment. My view is that there is time stored in that cellphone but its vintage may be somewhat sour, as compared to the sweetness of the here and now. The most unfortunate aspect of this new virtual reality stored deep within “inner space” is that more and more people, especially young people, are evolving to believe that these experiences are “natural.” A Pew survey in 2011 found that the average American teenager sends or receives between 100 and 200 text messages a day. At some point they may get so caught up in their frantic “busyness” that they fail to capture their present.

Still, my plea for “living in the moment” is a most difficult one, is it not? The present comes and then it goes, and staying in the moment is sort of like chasing fireflies on a hot summer evening in the Midwest. The light goes on and off, and then it’s on to the next firefly. It’s hard to capture a firefly unless your focus is laser-like, and the cellphone with its camera may help us to do that in a virtual, but not a real way. All of us, though, may need a bottle of sorts to store time’s mercurial moments. As John Denver once sang, “What a friend we have in time, gives us children, makes us wine.” I like that. But it’s the wine drinking and the children making that should be the highlights. The cellphones? Well in my world they exist just for your calling – not mine. They may be virtual, but they’re not reality.

PIMCO’s reality in recent months has been captured by the phrase “The New Neutral.” Having introduced the “New Normal” in 2009 with much success but unfortunately no trademark protection, we now venture forward in time, hoping to store this new metaphor in a proverbial bottle, cellphone, or better yet – portfolio – to much fanfare and ultimately alpha generating success. But a firefly it is not. To PIMCO “The New Neutral” has a more permanent status, a secular lifespan, that suggests things are just gonna be this way for at least the next 3–5 years, and likely much more.

What is “The New Neutral” and why is it important to the pricing of all financial assets? Well “The New Neutral” refers to the Federal Reserve’s (and other central banks’) policy rate, the fed funds rate, which serves as a foundation for the cost of credit and the ultimate pricing of bonds, stocks and a host of alternative assets. If the FF rate changes, other asset prices move as well, not necessarily in tandem but sooner or later. The Fed’s policy rate is, by its character, the lowest yielding and highest quality investment that can be found over most investment cycles, but it guides all other assets and ultimately sets their prices.

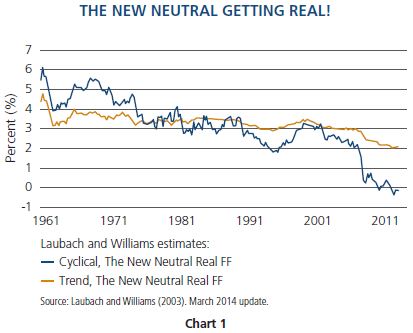

Back in the 1930s a famous economist by the name of Irving Fisher theorized that while the short term FF rate could change, it only moved with inflation, and therefore ultimately the “real” FF rate was constant. Time and historical experience has proved otherwise, suggesting that GDP growth, productivity and now a number of other factors might change the rate aside from inflationary influences; in other words the “real” rate was subject to ups and downs much like everything else. It was as “virtually” impossible to capture at any point in time as that Midwestern firefly. Take a look at Chart 1, displaying perhaps the most frequently cited research on the real FF rate, a study done by Laubach/Williams cited in my last month’s Investment Outlook. It shows not only significant cyclical changes in the real rate but also a significant long term “trend” change that has witnessed a decline in the real yield from over 4% in early 1970 to below 2% (and heading lower) today. Their most recent calculation of the current “cyclical” rate is actually -0.25%.

So the theory that the rate has changed is why it’s “New.” What about the “Neutral” – what does that mean? The Fed’s answer is that it is defined as the rate consistent with full employment trend growth and stable prices. Janet Yellen actually described it in a recent interview as the “Goldilocks rate,” a rate not too hot or not too cold but “just right.” Neutral. But defining it has proved to be much simpler than calculating it. Even so, for those that can calculate it, or even come close, there’s a pot of yummy outperforming porridge in store, and a cozy alpha bed to sleep in afterwards.

Up until this point, Yellen and her predecessors have attempted to model the appropriate rate based on a variety of factors. As the then San Francisco Fed President wrote in 2005, “Research suggests that the neutral real rate depends on a variety of factors – the stance of fiscal policy, the trend of the global economy … the level of housing prices, the equity markets, the slope of the yield curve ... and it changes over time.”

We at PIMCO cannot quarrel with such logic although that paragraph seems to have left off two rather important “structural” qualifiers that don’t fit neatly into preferred Federal Reserve quantitative models. First would be the acknowledgement that “The New Neutral” in significant part is determined by the trending real growth rates, rates that because of demographic and technological changes must fight growth headwinds because of slower labor force growth and less participation. If GDP growth is composed of labor force growth and productivity, then significant changes have occurred in recent years which likely have lowered “The New Neutral” by at least 1% or more as the Laubach/Williams statistics hint at.

Additionally, however, what Yellen and other central bankers are reluctant to admit – at least publically – is that neutral real rates are dependent upon financial system leverage – a Minsky concept that doesn’t fit neatly into mathematical models because the number of historical observations is limited and it doesn’t have a neat digital input that fits the “Taylor Model.” No matter – PIMCO tries to think out of the box. As a matter of fact, Paul McCulley (Paul is back!) in addition to being the creative thinker behind “shadow banking” and the “Minsky moment” had his own theory of “The New Neutral” back in 2009–2010. Our highly leveraged system, he theorized, contained increasing trillions of dollars of “new cash” – overnight repo, Fed Funds themselves, credit cards, etc. … that could be converted overnight into goods and services just like a $20 bill. And a $20 bill never got, nor ever deserved an interest rate; it got 0% sitting in your wallet or on your dresser. Its utility came because it was a unit of exchange, not a store of value with compounding interest; same thing with much of the $75 trillion of official and shadow bank credit now floating around the system. Maybe because interest was taxed, McCulley theorized, then the price of “real” short term credit should be 50 basis points or so, but nothing more – there should be “The New Neutral” and its price should be close to 0% real because there was so much of it that was finance as opposed to real economy related. Actually Paul did not come back to PIMCO in time to coin the term “The New Neutral” – that, trademark pending, would go to Rich Clarida – our new leader of the Secular Forum, but the foundation was there.

On top of that comes another thought piece – this one of my own creation – that argues for an extremely low “New Neutral”-led policy rate going forward. Commonsensically it seems to me that the more finance-based and highly levered an economy is the lower and lower real yield levels must be in order to prevent a Lehman-like earthquake. If the price of money is the basis for an economy’s prosperity – and it is increasingly so in developed global economies – then central banks must lower the cost of money to maintain that prosperity – and keep it low. How low? Well a little bit of history might help. During the period of similarly high leverage from 1945–1982 in the U.S. and U.K., real policy rates averaged

-31 and -133 basis points respectively. Other developed countries in Europe and Japan were even lower. These statistics come courtesy of a co-authored paper by Carmen Reinhart titled “The Liquidation of Government Debt,” written in 2011 and available at the following website: http://www.nber.org/papers/w16893.

The commonsensical correlation between high leverage and low interest rates comes to us most recently via the past few decades of experience in Japan. Although “The New Neutral” real policy rate has been mildly positive there, it is because of unwanted deflation as opposed to the unwillingness of the Bank of Japan to keep normal FF close to rock bottom zero. Too much leverage = artificially low policy rates = The New Neutral = 0–50 basis points real in the U.S. and many lesser developed economies. We should get used to it – and hopefully profit by it.

Investment Conclusions

The profiting by it is the hard part. With “The New Neutral” real and nominal interest rates, savers and investors are effectively being “taxed” in order to benefit debtors. As mentioned in last month’s Investment Outlook, there are ways to fight back, most of which involve emphasizing more attractively priced forms of “carry” than duration, especially at 10-year Treasury yields of 2.50% and below.

These alternative forms of earnings include credit, volatility, yield curve and currency overweights that themselves appear to be artificially priced, but less so. In addition, if “New Neutral” interest rates favor debtors as opposed to savers, then becoming a conservative debtor while structuring a portfolio appears to make common sense. It just has to be done carefully with a mind to future Minsky moments that can’t be conveniently captured in a cellphone, a bottle or even a diversified portfolio of stocks, bonds or alternative assets.

Prices of assets are, after all, quite similar to those Midwestern fireflies. On/off, up/down, they never stop moving – and the chasing of them is often frustrating and unproductive. PIMCO’s “The New Neutral” suggests that the real policy rates will be frigidly low for an extended period of time. If so, portfolio management will require a new approach, a new reality that PIMCO has always been willing to adapt to. To me and all of us here, that’s a virtual certainty – cellphone or not.

Time on a Cellphone Speed Read

1) PIMCO’s New Normal evolves into “The New Neutral.”

2) “The New Neutral” is a central bank’s policy rate that is just right. Not too restrictive, not too stimulative.

3) PIMCO believes that “The New Neutral” real policy rate will be close to 0 as opposed to

2–3% in prior decades.

4) If “The New Neutral” rates stay low, it supports current prices of financial assets. They would appear to be less bubbly.

William H. Gross

Managing Director

© PIMCO