“Regardless of very short-term market direction, it is urgent for investors to understand where the equity markets are positioned in the context of the full market cycle. While the most extreme overvalued, overbought, overbullish, rising-yield syndrome we define has generally appeared only at the most wicked market peaks in history, investors have ignored those conditions over the past year. We can’t be certain when the deferred consequences will emerge. But a century of market history provides strong reason to believe that any intervening gains will be wiped out in spades.

“It’s instructive that the 2000-2002 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bills – all the way back to May 1996, while the 2007-2009 decline wiped out the entire excess return of the S&P 500 all the way back to June 1995. Overconfidence and overvaluation always extract a terrible payback.

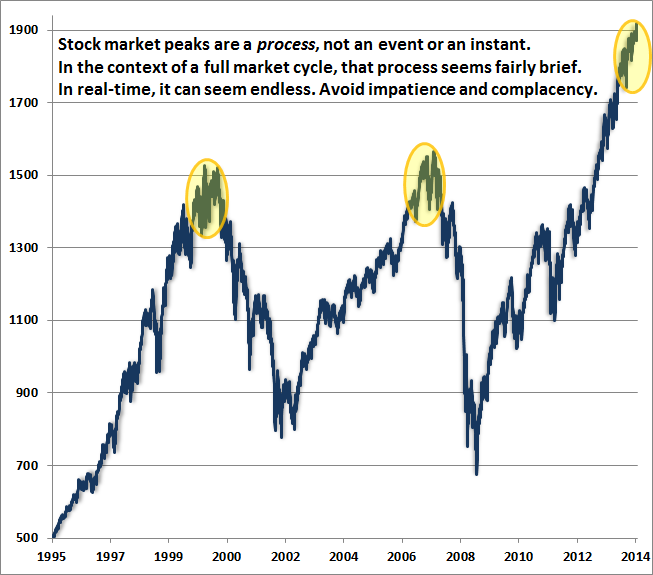

“It may also be helpful to remember that market peaks are a process, not an event. In the presence of a broad range of reliable valuation metrics uniformly at more than twice their historical norms, coupled with the most severe overvalued, overbought, overbullish, rising-yield syndrome we define, it is instructive how shorter-term action has evolved near those points. Outside of today and 1929, the other two instances are, not surprisingly, 2000 and 2007. The chart below provides a more granular reminder that market peaks are often a broad process and can involve hard initial downturns and swift recoveries. The ultimate follow-through provides some insight regarding the full scale of our concerns.”

It is Informed Optimism To Wait for the Rain - Hussman Weekly Market Comment 3/10/14

I should emphasize that the circled areas on the chart above aren’t chosen arbitrarily but reflect points where similar overvalued, overbought, overbullish extremes were observed. As I’ve noted in recent weeks (see The Journeys of Sisyphus and Exit Strategy), depending on how tightly we define this syndrome the 1972 and 1987 peaks can also be captured among the set of extremes that include 1929, 2000, 2007 and today. Remember that at a fine resolution, the full syndrome sometimes doesn’t precisely align with the final market high. Still, we remain convinced that any near term continuation we observe in this advance is likely to appear quite insignificant in the context of what the market loses over the completion of the cycle.

It’s fascinating how investors come to forget that markets move in cycles and not perpetual diagonal lines. As value investor Howard Marks wrote in The Most Important Thing, "Rule number one: most things will prove to be cyclical. Rule number two: some of the greatest opportunities for gain and loss come when other people forget rule number one." A normal, run-of-the mill cyclical bear market wipes out more than half of the preceding bull market advance. We should not be surprised at all to see the S&P 500 back at 2010 levels or below over the completion of the present cycle. From a valuation standpoint, we estimate that the S&P 500 Index would have to fall to the 1000 level to bring prospective 10-year nominal total returns toward their historical norm of about 10% annually. With the exception of the 2000-2002 bear market, valuations have typically been lower, and prospective returns higher, at cyclical troughs throughout recorded history (even in data prior to the 1960’s when interest rates were similarly depressed). Not that we need to forecast such an outcome, and certainly not that we would require anything near historical valuation norms to encourage a constructive stance, provided support from other factors. As always, the strongest prospective market return/risk profile is associated with a material retreat in valuations followed by an early improvement in broad measures of market internals.

A few side notes, in the continued belief that knowledge is power. It's quite accurate to observe that the recent half-cycle has been challenging for us, first because of our direct miss in the interim of our 2009-2010 stress-testing, and then because the resulting ensemble methods - though robust to Depression-era outcomes and having stronger performance in complete market cycles than any approach we've evaluated - did not fully capture certain bubble-sensitive features that were part of our pre-2008 methods. Those features relate mostly to what we called “trend uniformity” during the late-1990’s bubble. Repeated bouts of QE forced us to reintroduce similar bubble-sensitive features as an overlay. As I've often noted, nothing in the historical data encourages the attempt to speculate in a bubble once extremely overvalued, overbought, overbullish features emerge - and nothing in the historical record, even considering prior bubble periods, indicates we should speculate here. In any event, there’s no question or argument that my insistence on stress-testing against Depression-era data was a painful shot to the foot in this cycle, and is more painful because, at least to-date, it turned out to be unnecessary in hindsight.

Far from being perma-bearish, our present methods of classifying market return/risk profiles encourage aleveraged long position about 52% of the time in market cycles across history, encouraging a partially-hedged stance about 12% of the time, fully-hedged about 31% of the time, and hard-defensive as we are today about 5% of the time. I'm quite optimistic that we'll enjoy the full range of those opportunities in the cycle ahead. Both our pre-2008 and present methods indicate a leveraged stance in the early years of 1990’s, defensiveness in 2000-2002, bullishness starting in early-2003, and defensiveness in 2007-2009, as I also advised in real-time.Our stress-testing miss in this cycle is unfortunate, but recall that the 2007-2009 bear wiped out the entire total return of the S&P 500 in excess of T-bill returns going all the way back to June 1995. My view is that even a run-of-the-mill completion of the present market cycle, followed by historically normal constructive opportunities, will make this episode forgettable early into the cycle ahead.

The considerations behind shifts in these market return/risk profiles should be clear - the strongest profiles emerge when a significant retreat in valuations is coupled with an early improvement in market internals; the weakest profiles emerge when overvalued, overbought, overbullish conditions develop or when rich valuations are joined by broadening divergence or deterioration in market internals. Our main challenge in the recent half-cycle resulted neither from our pre-2008 methods nor from our present ones, but from the awkward transition from one to the other. I think it’s a very dangerous mistake to dispense with our present concerns by ignoring the narrative of our stress-testing response to the credit crisis, and concluding that our experience over this half-cycle has been a mechanical reflection of our pre-2008 methods, our present methods, or some perma-bearish disposition on my part.

Understand also that the evidence pointing to steep market risk over the completion of this cycle is quite robust, as the valuation criteria in the overvalued, overbought, overbullish syndromes we now observe would be satisfied even if stocks were significantly lower than they are at present. Other considerations that have historically been important would persist independent of our various concerns about profit margins, Fed-induced yield-seeking, covenant-lite leveraged loan issuance, equity margin debt, economic deceleration, and so forth. One of the casualties of writing as frequently as I do is that it’s easy to assume that our market assessments are highly dependent on any one of the score of topics we discuss. The litany of these concerns at present simply creates the risk that the completion of this cycle will be worse than the typical cycle, but we would be defensive here even in that absence of that prospect.

In my view, investors should be thinking very seriously about the extent of potential market losses over the completion of the present market cycle. It is the wrong question to ask “where else am I going to put my money with short-term interest rates near zero?” The problem with that question is that it carries the implicit assumption that the expected return on stocks is even positive or adequate given the prospective risks. At present, the better question is “do I prefer a zero loss to the prospect of a 40-60% interim loss in a market that is strenuously overbought and overbullish, and has returned to valuations that are more than double reliable historical valuation norms?”

On Friday, our estimate of prospective 10-year S&P nominal total returns set a new low for this cycle, falling below 2.2% annually. This is worse than the level observed at the 2007 market peak, or at any point in history outside of the late-1990's market bubble. It's possible that investors could drive prospective returns even lower than they are now, and valuations even higher than they are now, as investors did during that bubble. Still, even that advance started to be punctuated by abrupt vertical declines or "air pockets" once overvalued, overbought, overbullish features emerged (recall for example the increasingly frequent and distinct peak-trough corrections of 10% or more in Oct 1997, Jul-Oct 1998, Jul-Oct 1999, Jan-Feb 2000, Mar-Apr 2000, and Sep-Oct 2000 even before more severe losses got underway). See Setting the Record Straight for a general review of current valuations and prospective returns.

If your answer is still to take your chances in stocks, my only hope is that you do it consciously, fully aware that you’ve decided to ignore or discount the lessons from a century of historical evidence. The simple fact is thatsomebody has to hold stocks at present levels, so there’s really no point in trying to convince others to embrace our concerns, or to answer every second-guess that presumes that “this time is different.” I’ll be quite happy if at least stocks are being held by those who understand the full narrative of the recent half-cycle, and have seen, considered, and discarded our work.

"Well bought is half-sold. it takes a lot of hard work or a lot of luck to turn something bought at a too-high price into a successful investment. There aren't always great things to do, and sometimes we maximize our contribution by being discerning and relatively inactive. Patient opportunism - waiting for bargains - is often your best strategy."

- Howard Marks