I am El Niño! All other tropical storms must bow before El Niño! ¡Yo soy El Niño! For those of you who don't habla Español, “El Niño” is Spanish for...“the Niño”!

As analysts and investors, we often look for discrepancies between market prices and intrinsic prices inferred by the odds of certain future events. Sometimes these opportunities present themselves conventionally, such as a regime change in an emerging economy that the market underappreciates. Another example is how domestic bond investors overestimated the speed and magnitude of the Fed tightening, initially pushing up yields, only to see yields fall again in the beginning of this year. Oftentimes, mispricing is created by investor misjudgment by not correctly assessing the odds of an event or the degree to which the event affects prices.

In our investing process, we look across the spectrum at a multitude of possible events, their probabilities, their effects on markets and weigh them against market prices. Sometimes these discrepancies come from unexpected places. This week we will explore the ramifications of a weather event, El Niño. The soft-commodity markets (grains, sugar, coffee, cocoa and other annual crops) seem to have priced in about a 20% likelihood of an El Niño occurrence this year, while last week the Climate Prediction Center issued a 65% probability for this summer.

What is it?

Years ago, Peruvian fishermen noticed a periodic warming of the ocean temperature. The warming cycle seemed to occur around Christmas in certain years, so it came to be called “the Christ Child,” or El Niño in Spanish.

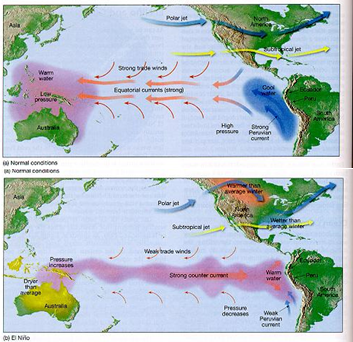

El Niño is an interruption of the ocean water and air-atmosphere in the Pacific Ocean. An El Niño starts as warm water near Indonesia spreads eastward and rises to the surface of the Pacific. Weak easterly trade winds and strong westerly counter currents move warm water west across the Pacific. This ocean water movement also shifts air pressure, taking rain from Australia and Asia and shifting it into the Americas, especially South America. This El Niño-induced unusually warm ocean water along the Pacific coast of South America also increases temperatures in Alaska and the northeastern U.S.

(Source: USC)

The top chart above shows climate conditions under normal weather years, while the bottom chart shows El Niño years, when warm water moves westward across the Pacific.

(Source: NOAA)

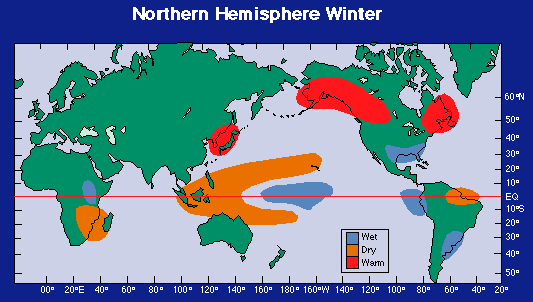

As the chart above shows in blue, El Niño rains are heavier in Peru, southern Brazil and Argentina. The orange areas on the map indicate dry areas and include pretty much all of Southeast Asia and northern Brazil.

The usual El Niño interval is between two and seven years and the warming period lasts nine months to two years. The warming trend has a ripple effect throughout the world. Normally, the climates around the eastern and western Pacific are very different, and the climates almost reverse during El Niño years. Southeast Asia and Australia become drier, while the Pacific coast of South America sees warmer ocean and air temperatures and regionally heavy rains.

It is worth noting that the last El Niño interval occurred in 2009-10 and since then the Pacific has either seen normal temperatures or cooler conditions, called La Niña.

Strength of El Niño

Weather forecasters are no longer talking about if there will be an El Niño this year; they are almost certain there will be one. They are not even talking about whether it will be a mild or severe El Niño. The language seems to have turned to weighing the odds of a super vs. super-super El Niño.

The National Weather Service released a note in May indicating that the chances of El Niño start at 65% this summer and go up from there. By November or December, the chances are near-certain.

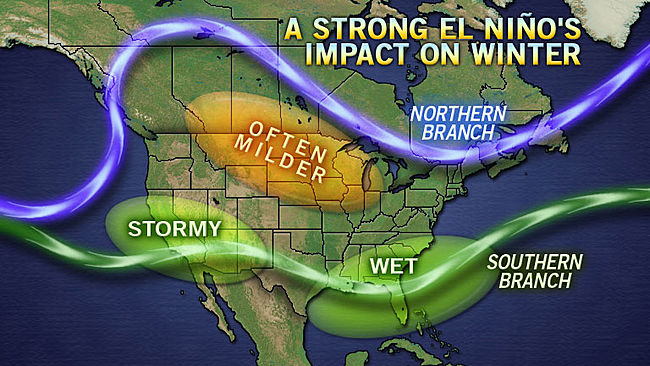

As the strength of El Niño varies, so does its effect on global climate. Let’s say that forecasters are correct and this year’s El Niño will be strong. The map below shows the effects on the U.S. winter climate. The southern half of the country would become wetter and stormier than usual. At the same time, the northern half of the country would see a milder winter, reducing heating costs.

(Source: AccuWeather)

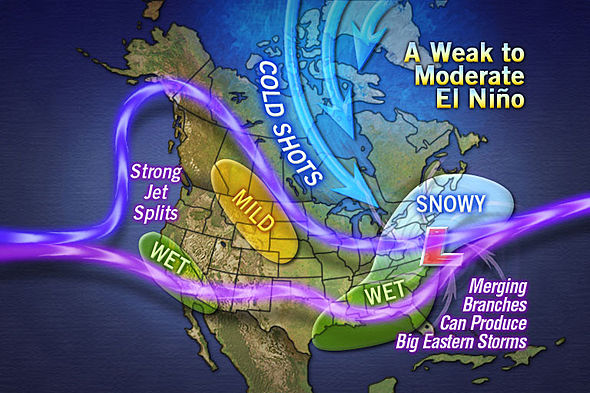

On the other hand, if this year’s El Niño is weak or moderate, the Northeast would see colder fronts move in.

(Source: AccuWeather)

The likelihood of a strong El Niño is high. Still, as can be observed from daily weather forecasting, sometimes even a near-certain weather event does not materialize, so there’s also a chance that El Niño will be extremely weak.

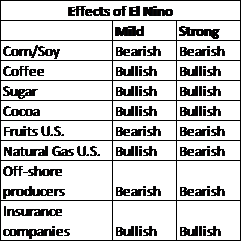

Effects of El Niño

El Niño is associated with severe weather changes, so it is assumed that the climate consequences would be adverse. This assumption is not necessarily true. Although parts of the world may see the development of unfavorable weather, other parts may benefit. Asia and Australia usually see droughts during El Niño years, which can be damaging to the local agriculture. Indonesia and the Philippines seem to be close to the epicenter of El Niño-induced droughts. The lack of rain caused by the cooler ocean water can damage coffee, cocoa and palm oil yields. Additionally, wildfires can develop, threatening local villages. Many agriculture-dependent economies can be severely affected.

In Southeast Asia, most of the effects of El Niño depend on its effect on the monsoons, which has been somewhat unpredictable. Most El Niños weaken the monsoons, but the Indian monsoon season may be unaffected. Although the 1997-98 El Niño was the biggest on record, it did not affect the Indian monsoon season.

However, this part of the natural climate cycle allows for various benefits to the eastern side of the Pacific. Plentiful rainfall in the spring in southern Brazil, central Argentina and Uruguay leads to better yields from summer crops. Soybean and livestock supplies are likely to improve due to increased rainfall. At the same time, mineral exploration is likely to see work stoppages due to the rains.

El Niño periods are also associated with warmer winter temperatures in the Americas, which mean lower heating costs across the northern United States. El Niño also brings fewer Atlantic hurricanes, but does not reduce the intensity of the hurricanes that do develop. This could help off-shore refiners and the insurance industry.

Although global temperatures generally rise during El Niño, Alaska seems especially susceptible. The warming jet stream melts more ice and snow, leading to higher ocean levels. Ocean levels around California could rise as much as 12 inches; at the same time, given the current California drought, such storms would be welcome to replensih depleted reservoirs. Higher sea levels could also mean increased storm surges, leading to mud slides as seen in the San Francisco area during 1997-98.

In general, soft-commodity prices rally between 10-40% during El Niño periods. Sugar and coffee prices have risen the most during the last six El Niño events as their production is concentrated in areas mostly affected by droughts. Coffee prices have risen more than 60% year-to-date due to drought conditions in Brazil. A season of adverse weather following such steep price increases would support coffee prices across all grades, likely pushing the lower grade prices up at a faster pace. Palm oil production may also suffer if an El Niño develops, following a recent dry spell in Indonesia and Malaysia.

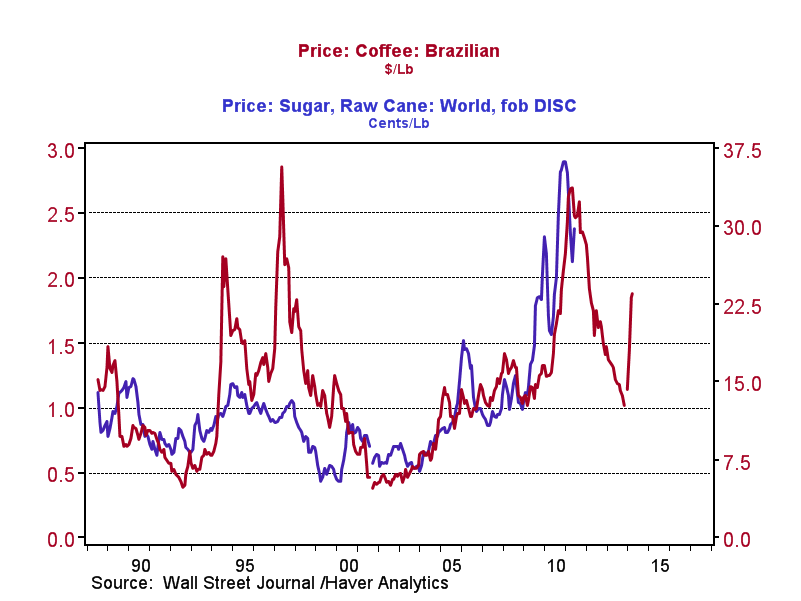

(Source: Haver)

The chart above shows the prices of a pound of coffee and raw sugar cane. The 1997-98 El Niño years can be clearly seen on the chart. Although prices moved higher during the 2009-10 El Niño, we believe there were other supply-demand forces also affecting prices.

Global trade could also be physically affected as shipping through the Panama Canal could be restricted due to low water levels which have occurred during prior El Niño periods.

Ramifications

We have prepared the following table to list the effects of a mild and a severe El Niño.

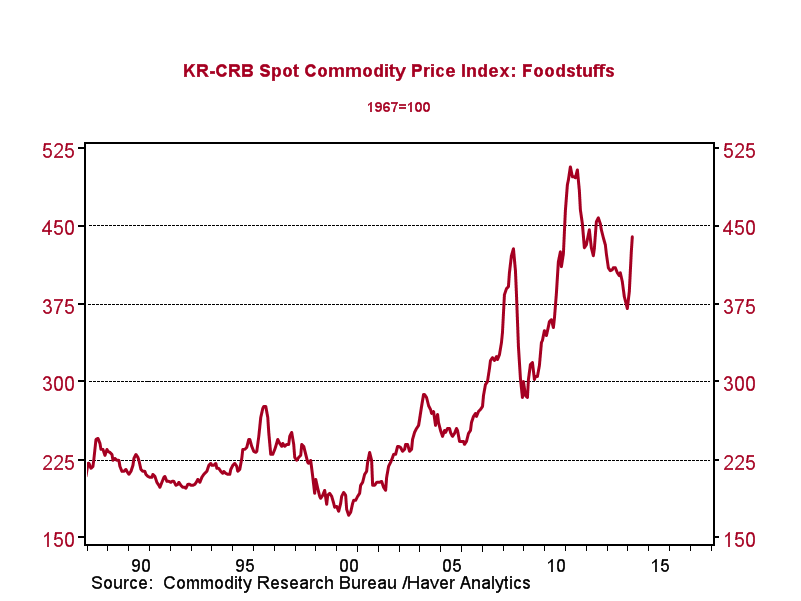

The chart below shows the price level of the CRB Foodstuffs Index.

(Source: Haver)

We would keep in mind that the year-to-date increase in the prices of soft commodities has not been related to the upcoming El Niño, but a consecutive year of bullish events for the space could mean a further surge in prices.

Kaisa Stucke & Bill O’Grady

May 12, 2014

This report was prepared by Kaisa Stucke and Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

(c) Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

© Confluence Investment Management