Managed Futures: Positive Trends Ahead??

Trend-following, the primary approach used in managed futures strategies, seeks positive returns by capturing momentum across major asset classes.

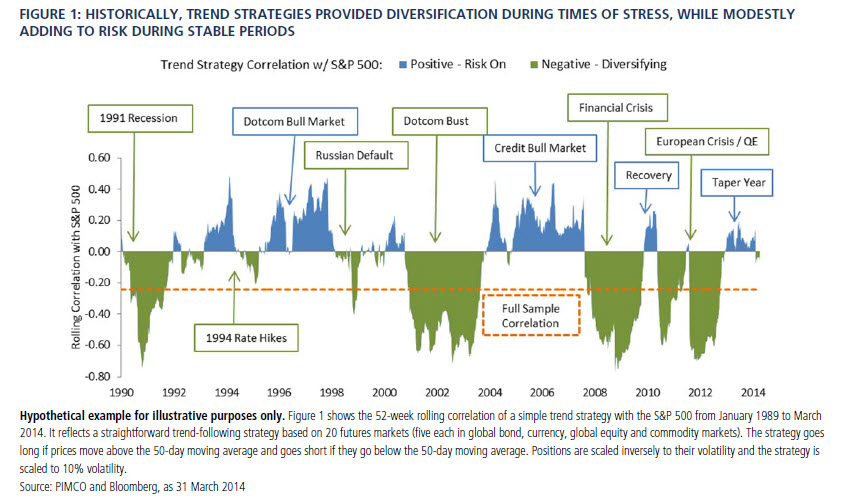

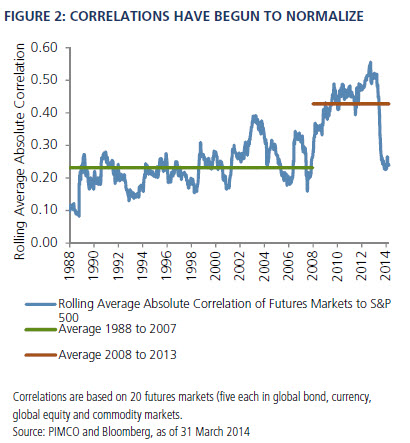

Despite exceptional performance in the 2008 financial crisis, trend-following strategies were less successful in subsequent years, in part because massive central bank interventions increased market correlations, suppressed volatility and curtailed left-tail events.

These dynamics seem set to dissipate with the onset of Federal Reserve tapering and the possibility of heightened volatility. We believe PIMCO’s strategy, which employs a number of modifications to the classic trend-following approach, could be especially valuable in coming years.

Trend-following, the primary approach used in managed futures strategies, seeks positive returns by capturing momentum across major asset classes. While trend-following has generally delivered strong returns over multiple decades, its history of diversifying equity-dominated portfolios, especially in left-tail market events, has been its most prized quality. It is one of the few strategies to have excelled in the dotcom bust and financial crisis. In recent years, though, trend-following strategies have been less successful, partly, we believe, due to massive central bank interventions that have served to increase market correlations, suppress volatility and curtail left-tail events.

- Risk management bias: The strategy is designed to maximize its risk management role by constraining exposures that may add to traditional portfolio risks while leaving unconstrained the strategy’s ability to scale up rapidly in sell-offs.

- Scaling rules: We do not target a constant risk level, but rather scale up volatility as opportunities develop and scale down when market trends are few.

- Drag reduction: Optimization of carry in portfolios is a core PIMCO theme. The strength of a trend is weighed against potential drag from negative carry and roll-down.

- Execution and market knowledge: The specific markets and contracts PIMCO trades are influenced by our bottom-up and top-down research into numerous asset classes. PIMCO specialist desks execute trades, seeking to optimize transaction costs.

- Active collateral management: In an era of low “risk-free” returns, maximizing the potential from investing collateral through PIMCO’s active fixed income management can add a significant boost.

Trending back

The likely tapering of the Fed’s asset-purchase program this year may mark the beginning of the end of a monetary policy regime that has weakened trend-following strategies. We expect correlations among asset classes will decrease while market volatility, returns and diversification potential will increase. In short, the trends are positive.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Absolute return portfolios may not fully participate in strong positive market rallies. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Derivatives and commodity-linked derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Commodity-linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Investing in derivatives could lose more than the amount invested. The models evaluate securities or securities markets based on certain assumptions concerning the interplay of market factors. Models used may not adequately take into account certain factors, may not perform as intended, and may result in a decline in the value of your investment, which could be substantial. Diversification does not ensure against loss. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2014, PIMCO.

© PIMCO