- While the Fed’s qualitative guidance may have increased uncertainties over monetary policy, volatility will likely remain contained by powerful short- and long-run forces related to the economic outlook.

- In the UK, we should at least respect the risk of a hike late in the first quarter of 2015, earlier than what is currently priced in.

- In Japan, we believe the BOJ will remain full throttle on its current monetary easing for some time.

Is the sky falling in the bond market? Many last year during the summer turbulence thought so, and after a period of cloudiness last month, fears returned. Yet the fears were again unfounded.

Investors fully reversed the interest rate hikes that they built into market prices after the Federal Reserve’s last meeting on March 19th, when Fed Chair Janet Yellen appeared to suggest that the Fed might raise interest rates sooner than markets previously expected – perhaps as early as the start of the second quarter of 2015. Fed officials since then have done their version of the Michael Jackson “moonwalk,” taking pains to calm markets and make clear that the Fed will be patient with respect to the reduction and eventual removal of its monetary accommodation. Interest rates have fallen and equity prices have generally gained in response to the backtracking.

Recent market volatility in response to Fed communications reminds investors of the challenges the Fed faces as it pivots away from its so-called quantitative forward guidance toward its more nuanced and difficult-to-interpret qualitative guidance. For example, it is more difficult today to judge whether progress is being made toward the Fed’s goal of improving labor market conditions than it was before the Fed dropped its unemployment threshold of 6.5%. It is similarly difficult to make judgments on the timing of future policy actions today versus when the Fed had calendar-based guidance in play.

While uncertainties about what’s next for monetary policy have increased as a result of the Fed’s more nuanced qualitative guidance, this won’t necessarily translate into a sustained increase in market volatility. To be sure, volatility is apt to increase when economic data of interest to the Fed and markets point to potential changes in the policy outlook. Nevertheless, volatility will likely remain contained by very powerful short- and long-run forces related to the economic outlook.

The short-run restraint relates to the continued lack of wage pressure and low inflation. Can you imagine Janet Yellen and the Fed next year – following six years of weak 2% wage growth – saying to Americans, “That’s enough for you! You lagged behind on wages for six years but now you’ve had six months of catch-up, so now we are going to put an end to it!” Doubtful. More likely the Fed moves cautiously and allows some catch-up.

The long-run level of the Fed’s policy rate is informed by many influences. The Fed described five of these influences in the minutes to its March 19th FOMC meeting:

1. Higher precautionary savings behavior by U.S. households

2. Higher global savings rates

3. Demographic changes

4. Slower growth in potential output

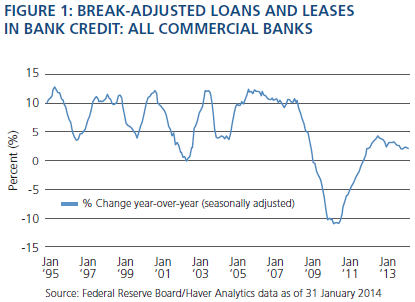

5. Restrained growth in credit creation (Figure 1)

Each of these is a powerful reason to believe that the long-run growth rate for the U.S. economy has fallen compared with recent decades, which therefore means the final resting rate for the Fed’s policy rate is likely lower now than in the past. It is reasonable to believe, for example, that if bank lending grows more slowly than it used to, then the amount of rate hikes needed to rein in credit growth will be less than it used to be because there simply won’t be as much credit to rein in.

Demographic factors also provide powerful reasoning for forecasts on rates. As America’s population ages, fewer people will be working as a percentage of the population. As more Americans retire and spend time golfing, visiting their families or traveling the globe, rather than spend time in a factory, we will be producing less – the economy simply can’t grow as fast. Hence, the need for growth-slowing rate hikes is reduced.

All of this is a way to say, dear investors, don’t let the Fed’s own communications make a Henny Penny out of you. In the Aesop fable, Henny, Chicken Little, and their feathery friends got themselves into trouble worrying that “the sky is falling.” Ultimately, Henny and her worrywart friends, in their effort to warn the world of danger, instead found themselves in a wolf’s den.

Unsuspecting investors will also be snared if they worry too much – about the Fed, in this case – so we suggest considering the list of reasons the Fed has provided as to why its policy rate, and hence market interest rates, are unlikely to rise as much in the next rate hike cycle as they have in past cycles. Bet against high levels of market interest rates and expect continued relatively low interest rate volatility. Take advantage of occasional bouts of fear. Don’t be a Henny Penny!

Will low inflation stay the hand of the Bank of England? – Mike Amey

The current data flow out of the UK is about as good as it gets. GDP growth is running close to a 3% annualised rate (according to the Office for National Statistics), employment is rising, business investment is showing signs of life and inflation is, and will likely remain, below the 2% target. So with growth strong but inflation benign, can the Bank of England (BOE) allow the recovery to run its course without the spectre of future rate rises? While this may well be the case for the Federal Reserve, sadly we do not think this will be the case for the Bank of England.

As of March, CPI (the Consumer Prices Index, the key measure of UK inflation) is at 1.6% and stands a good chance of going a few tenths of a percent lower, thereby remaining comfortably below the 2% target. However, this comes after two years of above-target inflation, a period during which CPI peaked at 5.1% and yet the BOE retained a highly accommodative stance. Having (correctly) argued that the material inflationary overshoot was temporary, the BOE would find it hard to say that a more modest undershoot is a strong argument for leaving the recovery to run its course. We calculate that core CPI has been running at between 1.5% and 2% for the last three years (including the point at which headline CPI hit 5.1%). Our view is that the analysts at the BOE have a similar view of the underlying inflationary dynamics, in which case it is highly likely that the BOE will look through the current prints and highlight the stability of underlying inflation (rather than suggesting a risk of a persistent inflationary undershoot). If there is a benign outcome for UK interest rates, it will not be because of the CPI prints, but because wages fail to gain traction from their current 1% nominal growth. However, most of the early signs suggest wages are gaining some traction.

This leaves the prospect of the Bank of England being the first of the major central banks to hike rates during this cycle, something that looked inconceivable 12 months ago. Since then, the combination of better-than-expected growth and the BOE largely giving up on a sharp recovery in productivity leaves their forecast of spare capacity being used up by the end of next year. If that happens, they expect to be hiking rates by the spring of next year – interestingly close to the UK general election in May 2015. While the BOE is at pains to play down the significance of the general election on monetary policy, it is hard to see the first rate hike coming coincident with the election. So we should at least respect the risk of a hike late in Q1 2015, earlier than what is currently priced in. At a minimum we believe there should be a risk premium embedded into the UK interest rate market, something which does not currently exist. With that as a backdrop, our view is that the UK bond market remains a market best avoided for those who can.

Bank of Japan: one year on – Tadashi Kakuchi

Nearly one year has passed since the BOJ embarked on very aggressive monetary easing (Quantitative and Qualitative monetary Easing, or QQE) under Governor Haruhiko Kuroda in April 2013. Since then, Japan’s economy has shown impressive growth, and core CPI (consumer price index) has moved from negative to 1.3% as of February 2014 (source: Statistics Bureau). Governor Kuroda has also demonstrated his strong commitment to achieving the BOJ’s 2% inflation target. Looking ahead, what do we expect from the BOJ, and how should we consider positioning our portfolios for the cyclical horizon?

What we know for sure is that the BOJ’s balance sheet expansion will continue beyond 2014. When the BOJ introduced QQE last year, the central bank clarified that it would continue current easing until the 2% inflation target is achieved and sustainable. Even under the BOJ’s optimistic economic assessment, 2% inflation likely won’t be achievable until late 2015. Therefore, we expect the BOJ not to slow down but to keep its foot firmly on the gas pedal. Then how about the likelihood of additional monetary easing? Will the BOJ push the gas pedal closer to the floor?

In our view, two factors could be key drivers for further easing: risk market conditions and macro data releases following the value-added tax (VAT) hike this month. By nature, the BOJ’s monetary policy is highly susceptible to domestic risk market fluctuations (in Japanese yen and Japanese equities) as the central bank’s transmission channel is mainly limited to expectation channels. A sharp appreciation of the yen and a fall in Japanese equities would have serious negative effects on Japan’s economy, and the BOJ would do nearly anything to avoid such outcomes – effectively underwriting a “call” on the yen and a “put” on Japanese equities.

Macroeconomic data releases in the second and third quarter of 2014 could also trigger further BOJ easing. The central bank expects the Japanese economy to rebound strongly after a temporary slowdown in April 2014 due to the VAT hike, and its growth projection (+1.4% for fiscal year 2014) is well above market consensus. This optimistic growth scenario helps explain the bank’s forecast for 2% inflation in the latter part of 2015 via a shrinking output gap. However, we expect the BOJ will be disappointed by the recovery in the domestic economy post VAT hike. With real disposable income decreased due to higher inflation and the tax hike, private demand will likely be more lackluster.

In our view, barring a sharp adverse move in asset markets, the BOJ is likely to wait until actual post-hike macro data are published (late summer at the earliest), and if the data suggest weakness only then would it embark on further easing.

When positioning portfolios in light of this analysis, we may look to short Japanese yen given the policy divergence between the U.S. Federal Reserve and the BOJ. Irrespective of the likelihood of further easing, we believe the BOJ will remain full throttle on its current monetary easing for some time, in clear contrast to the Fed, where tapering has already started. Given some market participants still expect pre-emptive BOJ actions, we could see some short-term market retracement, but the likely medium-term trend is continued weakening of the yen.

The third mandate – Ben Emons

In recent years, many global central banks have included financial stability as an objective when setting policy. Dubbed the “third mandate,” financial stability is playing a greater role in central banks’ reaction functions (i.e., policy adjustments in light of changes in macroeconomic developments). However, this third mandate may conflict with other mandates such as unemployment or inflation.

In highly levered financial systems (therefore, in most major economies in the world today), financial stability and interest rates are closely linked. An adverse change in the policy rate may increase risks to financial stability and negatively affect the economy. By focusing on increased regulation while maintaining forward guidance on policy rates, central banks attempt to loosen this linkage between financial stability and monetary policy.

Central banks in the major economies as well as Sweden, New Zealand, Australia and Switzerland face a significant challenge: By hiking interest rates in response to more robust economic activity, these nations may attract additional foreign capital, potentially leading to further overheating of housing and other asset markets. Alternatively, if these banks respond by hiking slowly or not at all, investors may continue to seek higher-yielding assets, further fueling financial instability risks.

Compounding the issue, major advanced economies also suffer from too-low inflation and could face pressure to maintain a chronic zero-bound rate environment even as unemployment rates fall. In order to escape this situation, economies need sustained high asset prices that reduce indebtedness and support economic growth.

All this poses a major dilemma to central banks: either experience subdued inflation or add to financial instability risks. To address the latter, central banks would have to ponder using their most blunt tool: interest rate hikes. This would be a difficult choice.

So far, most central banks have opted for other approaches to financial instability risks. In particular, they have tightened regulations and increased oversight on mortgages and leveraged credit. There have also been increases in capital requirements for banks. At the same time, central banks have shifted to more qualitative forward guidance to provide some sense of timing with respect to their eventual exits from today’s highly accommodative monetary policy regimes.

Although there is optimism for higher growth in most developed economies, it remains highly questionable whether interest rates can be used to address financial stability concerns. Rather than following a more rules-based monetary policy when inflation and unemployment are near mandate-consistent levels, central banks need to manage interest rate expectations more carefully to balance financial instability risks.

For investors, this means that aggressive rate hikes are less likely in an environment of low inflation where financial stability has to be guarded delicately. Therefore, expect central banks in the major developed markets to embark on a shallower interest rate tightening cycle than in the past.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Investors should consult their investment professional prior to making an investment decision.

The U.K. Consumer Price Index (CPI) measures the change in prices for retail goods and services, including food and gas. The CPI is the key measure of inflation for the UK and is used by the Bank of England in making interest rate decisions. The report tracks changes in the price of a basket of goods and services that a typical British household might purchase. An increase in the index indicates that it takes more Sterling to purchase this same set of basic consumer items. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2014, PIMCO.

© PIMCO