(N.B. This report is the final installment of the series on the 2016 election.)

In the previous report, we discussed the four archetypes of American domestic politics and offered a short history of how these classes interacted politically and created coalitions over time. We also examined the impact of their interaction on policy.

In this final report, we will analyze why we think 2016 may be a pivotal election. We will then examine the potential that the next presidential election could bring about a coalition change similar to the 1932 and the 1980 elections. We will discuss the various methods of addressing the current high level of private sector debt. We will offer what we believe to be the three highest probability scenarios of how the current problems could be addressed and their impact on the domestic political scene and on America’s superpower role. Unlike our last two reports, but common with all other geopolitical reports, we will conclude with market ramifications.

Why 2016 Could Be Pivotal

In Part 1, we examined the current state of the economy. Our analysis suggested that the reason for persistently weak economic growth was an overleveraged private sector. Essentially, the private sector, but especially the household sector, is carrying too much debt. This debt was primarily incurred for two reasons. First, the financial part of the superpower role requires the U.S. to act as the global importer of last resort. This means that consumption levels will tend to be higher than otherwise because every nation in the world has an incentive to run a trade surplus with the U.S. in order to acquire dollars. As imports rise, American consumers are given incentives to lift consumption. Imports keep prices low and the recycling of foreign surplus, an element of the reserve currency role, leads to lower interest rates.

As America’s share of global GDP fell, in part due to the success that the U.S. had in leading the world to recovery after WWII, the dollar’s reserve role forced the U.S. to steadily increase consumption. The U.S. adopted deregulation and globalization policies to quell the inflation crisis that developed during 1965-80.

This chart shows real median family income from 1947 through 2012. Note that income growth began to flatten out as inflation rose and failed to recover to the 1947-69 trend line due mostly to globalization and deregulation.

As a side effect of containing inflation, middle class incomes lagged; these households increased their borrowing to maintain living standards and, unwittingly, to support the dollar’s reserve role.

Herbert Stein, Chairman of Economic Advisors under Nixon and Ford, once said, “If something cannot go on forever, it will stop.” In our opinion, the current economic situation isn’t politically sustainable in the long run. Persistently slow growth, low levels of employment participation and weak real income growth for households is a politically combustible mix. The way to fix this problem is deleveraging the private sector. Unfortunately, fixing this problem will require very difficult political decisions, which we detail below.

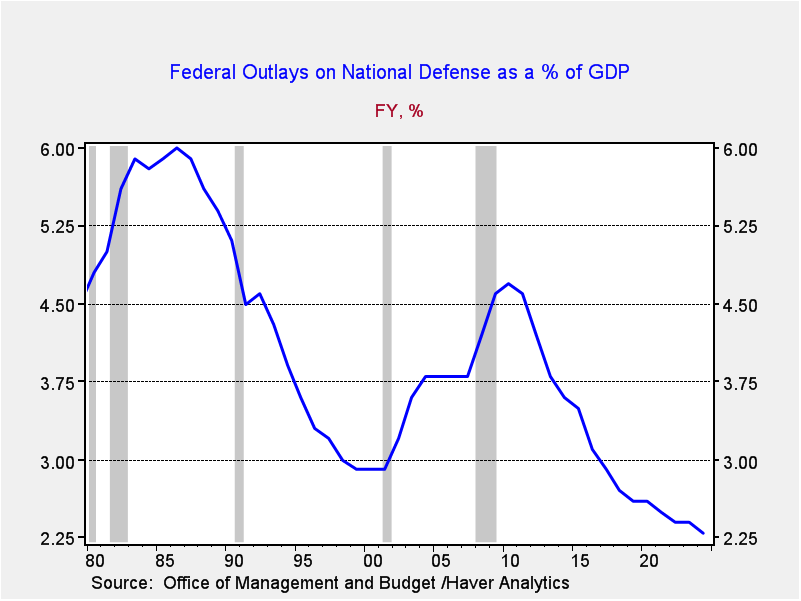

The second reason that 2016 could be pivotal is that the drift in American foreign policy is becoming unstable. After the Cold War ended, there was a general military demobilization as the chart below indicates.

This chart shows defense spending as a percent of GDP. It includes OMB forecasts for 2015-24 which indicate that spending is projected to fall to a mere 2.3% of GDP by 2024. That would be the lowest level of defense spending since America became a superpower.

Although there is great hope of continuing the superpower role with a smaller fiscal commitment, recent developments have seriously undermined confidence that the U.S. can maintain the superpower role with low defense spending and a slow economy. The crisis in Ukraine, the rising belligerence of China and the increasing unrest across the Middle East are all signs that as American influence wanes, the world is becoming an increasingly dangerous place. Sanctions are no substitute for hard power.

It is into this environment that presidential elections will be held in two years. There is no easy path of policy that will allow the U.S. to maintain its superpower role and address the slow growth and debt issue. At the same time, this reality must be framed by political structures. It is within the existing framework that the integration of the superpower role into the economy and society is accomplished. In Part 2, we detailed our analysis of America’s political structure through a series of archetypes. The interaction of these archetypes will determine how the political structure reacts to the rising challenges.

How Does Deleveraging Occur?

There are essentially six methods of private sector deleveraging. All of them bear costs for either the creditor or the debtor.

Ø Pay the debt back under the terms of the loan: This method, obviously supported by creditors, requires the debtor to meet the terms of the loan. Thus, to reduce debt, the debtor usually must refrain from taking on new debt and devote income to paying off current debt. Although this is a reasonable outcome at the micro level, at the macro level it means that economic growth slows dramatically as debtors reduce their spending, which leads to falling consumption and reduced investment. After all, there is little incentive to invest when growth is declining.

Ø Restructure the loan: Creditors realize that the macro effects of high debt are destructive and thus negotiate terms that reduce the cost of debt service. This may include partial principal forgiveness, an extension of the loan’s term or a reduction in the interest rate. Although this is a time-honored method as well, it is difficult to execute quickly on a large scale. In addition, in modern finance, with many loans packaged into debt securities, negotiating becomes almost impossible.

Ø Foreclosure: This method is something of a “nuclear option” in that usually both the creditor and debtor lose. When there are a large number of foreclosures, the assets that back these loans usually fall in value, meaning that creditors do not recover the full value of their loans. Debtors that face foreclosure tend not to become active borrowers in the future, either because they are viewed as poor credit risks or they are scarred by the experience and prefer to remain debt free.

Ø Socialization: The government, in a number of ways, provides liquidity to borrowers, allowing them to repay their loans. The government borrows the money to provide liquidity to debtors and then uses the coercive power of taxation to service public sector debt. If the tax code is progressive, creditors tend to lose out as they pay more of the debt service costs of the government. At the same time, creditors do receive the full value of their private sector debt; since “crowding out” may occur, creditors swap their private bonds for government bonds, which usually would lead to this reinvested capital receiving a lower interest rate. In addition, once this method is deployed, it is hard not to repeat because debtors like being bailed out and creditors like the government guarantee. Variants of this process are seen where the government guarantees debt repayment, e.g., student loans, mortgages, bank deposits, etc.

Ø Repudiation, bankruptcy and forgiveness: Repudiation on a large scale usually occurs through revolution while the latter two are on a micro level. In the case of repudiation, debtors, which usually outnumber creditors, simply refuse to pay or return collateral that backs the loans. If the government loses its coercive power, creditors simply lose out. This method has occurred in nearly all nations that have experienced communist revolutions. Bankruptcy uses the courts to force either debt forgiveness or restructuring. It doesn’t work well on a large scale as it requires intervention by the court system which becomes a major bottleneck. Debt forgiveness usually occurs when a creditor realizes he has no method of continuing to receive debt service or acquiring any valuable collateral. Forgiveness, like bankruptcy, is a small-scale solution.

Ø Inflation: Governments and their central banks may decide that increasing the money supply in a bid to trigger inflation is the least painful way of deleveraging. Creditors have their debt serviced but receive less valuable currency over time. This method is often attractive to governments because it is a “stealth” method of restructuring debt. However, it carries significant risks. Debtors, seeing that real assets are holding their value, tend to ramp up their borrowing even more, undermining the deleveraging process. Creditors will usually begin demanding ever higher interest rates to compensate for current and expected inflation. This method is usually not a long-term solution to deleveraging.

When large scale private sector deleveraging occurs, the political system tends to become deeply involved. Thus, there is great incentive for the four archetypes to gain power to influence how the deleveraging occurs.

The Alternatives

Although not exhaustive, we see three alternatives that are the most probable.

Status Quo: Although it is possible that the public will continue to live with weak economic growth, stagnant income growth and weak employment markets, we doubt this outcome will be accepted indefinitely. In fact, the longer these conditions remain in place, the greater the likelihood of a reaction that undermines the status quo. The rise of the Tea Party, the Occupy Wall Street movement and the Libertarian wing of the GOP all suggest that there is great dissatisfaction with current conditions. It appears to us that the only way the status quo could be maintained would be by keeping these political movements isolated and disenfranchised. It is rather obvious that the above movements and their members probably don’t meet together—the Occupy members would not feel welcome among the Tea Party groups and vice versa. However, they do share a clear belief that the political system isn’t working for their interests.

The ruling coalition (i.e., the rentier/professional and entrepreneurial classes) faces a “prisoner’s dilemma” situation in selecting presidential candidates. The coalition generally dominates the electoral process through campaign financing, meaning that most of the selecting is done by the rentier/professional and the entrepreneurial groups. These classes usually try to nominate a reliable “establishment” candidate. However, such candidates generally fail to excite populist voters. So, there is a great incentive to run a mainstream candidate that appeals to the populist classes on either wing. There is always great hope among the populists that getting a sympathetic candidate in the White House improves the odds that some of their political goals will be met. In reality, they rarely are.

For example, Bill Clinton was able to speak the language of left-wing populism but ran his government with policies that favored the ruling coalition. The 2000 election had two candidates that tried to portray themselves as speaking to populist concerns. Al Gore ran on his environmental record but could not shake the fact that he was seen as a member of an administration that was not supportive of left-wing populism. George W. Bush spoke the language of the socially conservative right-wing populists and offered a retreat from the Wilsonian foreign policy of the late Clinton administration. Instead, after winning the election, he aggressively cut taxes, which boosted the prospects for the members of the ruling coalition, and fought two inconclusive wars that were mostly fought by right-wing populists. He expanded Medicare, disenchanting the right-wing populists who didn’t appreciate the expansion of government. He also greatly expanded the national security apparatus, which was neither appreciated by the populist group nor elements of the entrepreneurial class.

President Obama’s first campaign offered hope to the left-wing populists as he promised to support their goals for health care and an end to the Bush wars. However, Obama, who is often characterized as a left-wing populist by the right-wing media, is considered a major disappointment by his left-wing populist supporters. At heart, he is more of a center-left member of the rentier/professional class than a populist.

The formula for winning elections has been for a candidate to convince the populists “that you are one of them” but raise campaign funds by comforting the ruling coalition members that nothing much is going to change. Of course, the more credible a candidate is to either wing of the populists, the greater the likelihood that they really are “one of them.” Thus, there is always a worry among the ruling coalition that they could inadvertently support a candidate that undermines their position.

It should be acknowledged that the American political system is designed to avoid radical changes. The fact that we do not directly elect presidents is part of this structure; so is the method of funding elections. Usually, those making large campaign contributions are not interested in a wholesale upending of the established order. And so, the most likely outcome is the status quo. In fact, history does suggest that major shifts are quite rare and it usually takes extraordinary situations to bring about a major change in the ruling coalition.

The status quo president would, almost by definition, try to maintain the ruling coalition’s goals, which include a deleveraging process that favors creditors and maintenance of America’s superpower status. The challenge for such a candidate would be his/her ability to maintain the current situation while facing rising threats.

Although the above description is about “type” rather than a specific candidate, the classic “status quo” election would be Hillary Clinton versus Jeb Bush. Both would represent political “dynasties” and both would be major disappointments to either of the populist wings. As we saw in the 2008 Democratic Party primary season, the known quantity of Hillary Clinton was rejected for the promise of Barak Obama. At present, we expect Mrs. Clinton to run but would not be surprised to see a challenger with left-wing populist credentials. On the GOP side, we still view Jeb Bush as a long shot and would expect a plethora of candidates trying to vie for the right-wing populist vote. On the other hand, odds still favor a GOP candidate that, in the end, maintains the status quo.

The Strong Man: America appears to be in retreat. It seems that respect for America is waning. There are concerns that allies are unsure whether America will support them and enemies are relishing the fact that they can finally achieve their “rightful” place in the world, no longer impeded by American restraint. If the U.S. continues its withdrawal, the world will likely evolve into a Hobbesian dystopia of constant regional wars.

A political figure that promises to reverse these trends would find strong support among the center-right of the rentier/professional and right-wing populist classes. Running on a platform to restore America’s military superpower role and honor would create a workable coalition. It should be noted that this candidate would face strong opposition from the libertarian elements of the entrepreneurial class and left-wing populists.

However, there is an intriguing element to such a candidate in that he/she may have a politically effective way to socialize private sector debt. As WWII showed, it is possible to use military spending as a fiscal expansion program which would create jobs and lift incomes.

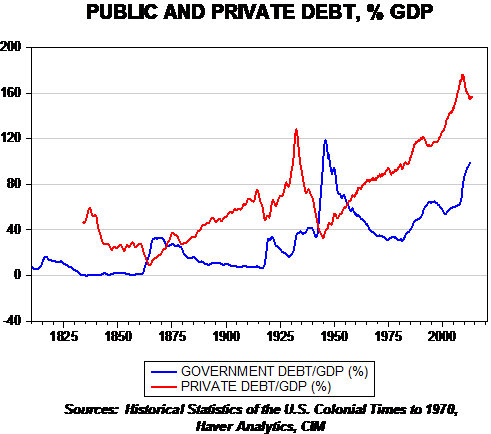

The Great Depression led to a massive debt liquidation that slowed economic growth. Note that the mobilization for WWII, which led to a massive rise in government debt, boosted economic growth and supported further private sector debt liquidation. For example, in 1940, private sector debt was still 65% of GDP. As defense spending ramped up after 1940, the expansion of public sector debt facilitated the final leg of private sector deleveraging. By 1945, the private sector debt/GDP ratio had declined to 34%. Public sector debt ballooned to 118% of GDP. Private sector deleveraging was accomplished by creating jobs and restraining consumption through wartime rationing. The large government debt that was accumulated by the war was steadily reduced via financial repression as households were “nudged” into government bonds that yielded less than the yearly change in GDP growth, a key element in reducing the debt relative to the economy.

A modern version of this program would generally require the defense industry to become an autarky,[1] which would mean that defense spending would become purely domestic stimulus. That way, the creation of low-skilled, high-paying jobs would not be outsourced. Geopolitically, the defense buildup would trigger a global arms race that the rest of the world could probably not win. And, the increase in military spending would signal to the world that the U.S. has the capability to enforce its will if it so chooses.

In addition, it is very possible that government non-defense spending could be hidden in the defense budget. President Eisenhower argued that America needed an interstate highway system for national defense purposes, suggesting that the system would be necessary for emergency evacuations and the movement of troops if America was ever attacked. Based on that idea, the U.S. embarked on what was, in the mid-1950s, the nation’s largest public works project. It would not be a shock to see public spending on airports (to improve security and for the Air National Guard) and cyber infrastructure (to protect the electrical grid and the internet). In effect, under the cover of defense spending, a massive fiscal expansion could be implemented to, ostensibly, boost national defense.

To some extent, the “strong man” candidate would be attempting to restore much of the 1930-80 coalition of the rentier/professional class with the right-wing populists. The right-wing populists have tended to become supporters of small government as they have concluded that government activities no longer support their class. However, this group also leans toward a Jacksonian foreign policy and would tend to support a strong defense, especially one that would create a significant number of high-paying, low-skilled jobs. In essence, defense spending is one of the few areas that the right-wing populists tend to view as a legitimate function of government and so they would likely approve of this approach even though it would lift deficit spending.

At the same time, the strong man model would allow globalization to remain in place. This would appeal to the current ruling coalition. Although the entrepreneurial class would be uncomfortable with the expansion of government that would come from higher defense spending, the maintenance of the superpower role would be appealing. Clearly, the loser in this alternative would be the left-wing populists.

Although the strong man alternative, as a type, carries a certain appeal, the problem is that there are no obvious candidates to fill this role. However, a Colin Powell, David Petraeus or Stanley McChrystal are conceivable choices. We do believe that it would take a “real” soldier to fill this role. On the GOP side, the neoconservatives mostly discredited themselves in the Iraq War, and on the Democratic Party side, the performance of the current administration in managing the Iraqi, Libyan, Syrian, Ukrainian and Afghan situations undermines any potential candidate without credible military experience.

The Isolationist: It may simply be the case that the American economy can no longer bear the burdens of the superpower role. This role distorts the U.S. economy, forcing it to consume more than the ideal and be open to trade even to the detriment of domestic industries. There is a deep affinity for the isolationist position in American history. George Washington warned against foreign entanglements. America has been populated with waves of immigrants who came here to begin a new life. Being involved in foreign affairs isn’t why people immigrated to America. Geography helps as well. America is surrounded by two oceans and has mostly pacified its neighbors. It faces few direct threats; in fact, there are basically only two foreign threats the U.S. faces, terrorism and nuclear missile strikes. As such, America is more secure than most nations and can afford to be isolationist.

If the U.S. abandons the superpower role, trade protection could be deployed. Since the world would likely become dominated by regional powers, the U.S. could dominate North America and create perhaps the world’s most powerful and stable trading bloc. By giving up the reserve currency role, the U.S. would no longer be obligated to act as importer of last resort. Military spending could be scaled back. The drop in military spending could be offset by more spending on social programs (a left-wing populist goal) or by smaller government and tax cuts (a right-wing populist and entrepreneurial goal).

It should be noted that taking an isolationist stance, by itself, would not necessarily end the private sector debt problem. However, the ability to regionalize the economy and reduce foreign competition could increase the number of high-paying, low-skilled jobs that are currently outsourced. Such a change would certainly support managing the private debt problem as it would boost incomes of the populist classes which, according to some research, carry the bulk of household debt.[2]

The current ruling coalition would be a clear loser in this alternative. Without globalization, labor costs would rise, capital returns would fall and income differences would almost certainly narrow.

This alternative does carry some significant caveats. Part of the reason the U.S. did not revert to isolationism after WWII was that the leadership of the country was worried that doing so would almost guarantee that America would fight WWIII. It should be noted, however, that there was opposition to an interventionist foreign policy. The GOP had an active isolationist wing in the early 1950s which was led by Sen. Robert Taft (R-OH), the eldest son of President William H. Taft. A world without U.S. leadership would likely be less stable and a globalized, integrated economy would likely cease to exist. The supply constraints caused by deglobalization would also certainly lead to higher inflation. Capital flight is also a risk, although in an isolationist world, it isn’t clear where it could go to be safe other than the U.S.

Interestingly enough, at least for a while, the U.S. would likely prosper. As the world became more dangerous, the U.S. would become the recipient of capital flight and talented foreigners would strive to come to North America to escape the unrest that would almost certainly occur if the U.S were to relinquish its superpower role.

The great unknown is whether North America could avoid the regional conflicts that would almost certainly develop. It isn’t hard to imagine that these would eventually find our doorstep. However, this process may take some time, and given the short attention span of democracies, the lure of isolationism may increase in 2016.

In terms of actual candidates, on the right, Rand Paul is the most obvious leader holding isolationist positions. Another is Pat Buchanan. However, we would expect that Elizabeth Warren would likely lean this way as well. Although polls do suggest a rising tide of isolationist attitudes among voters, there does not appear to be a convincing national leader that could win a nomination at present. Of course, if a military operation over the next year were to go horribly wrong, an isolationist may become more popular.

What Are the Odds?

The “safe money” would still expect the status quo to continue. There are no clear cut candidates that could be the standard bearer for either of the non-status quo outcomes. Most campaign funding comes from the current ruling coalition, meaning that representing the other alternatives would make it difficult for a potential candidate to finance a campaign. If the center-left and center-right were to offer clear “establishment” candidates (e.g., Hillary Clinton v. Jeb Bush) which made it through the primary process, voter turnout would probably be very low. Most likely, the GOP candidate would win simply because the right-wing populists would prefer a Republican to another Democratic administration. The thought of another eight years of a Democrat in the White House would likely prompt votes for a status quo Republican.

On the other hand, conditions seem to favor a third-party candidate that would represent the populist wings. Without a single candidate that could unify these two groups, which is probably a long shot, these candidates would swing the overall election but have little chance of winning outright. Of course, if two extra-party candidates ran, which isn’t out of the question given the degree of dissatisfaction with the ruling coalition, we could see an election outcome similar to 1860.

Although this point was mentioned in Part 2, it should be reiterated that populists on both sides have been made promises by the ruling coalition during elections only to be mostly ignored once the election is over. The anger at being ignored is palpable; the rise of Occupy Wall Street and the Tea Party, though clearly not the same, are indicative of the same phenomenon—the populists see a political system and economy that is, in their view, aligned against their interests.

In our judgment, the “dark horse” is a strong man candidate who would promise to maintain globalization but also restore America’s honor. Such a candidate would likely carry the ruling coalition and the right-wing populists. A strong dose of fiscal spending may go a long way to lift economic growth and reduce private sector debt. If one of the major parties begins to court retired military figures, this outcome is quite possible.

The isolationist candidate probably can’t win either major party’s nomination. But, it could be a viable third-party candidate that could disrupt the election.

In general, if the status quo is the alternative, nothing much would be different going forward. The strong man would represent a situation similar to the Progressive Movement or Richard Nixon’s presidency. It would be a shift within the current power structure to accommodate the goals of the ruling coalition but also offer support to right-wing populists. Moving to an isolationist stance would be a major change, similar in impact to the presidencies of Roosevelt or Reagan. Although the isolationists are different than these two, the change would be the political equivalent to “tectonic plates” shifting as the world would see a withdrawal of American leadership.

Ramifications

The market concerns about 2016 will likely begin to develop later next year. Any hints that a viable candidate could emerge from outside the status quo would probably be a negative factor for risk assets. Although there is nothing that currently signals a recession over the next 12 months, a major economic downturn into 2016 would increase the odds that the status quo would be overturned.

Although the next presidential election is rather far off, we wanted to offer our thoughts on what could bring about a significant change in government. And we wanted to escape the usual Republican/ Democrat framework to highlight differences that may emerge which may not be captured by a more traditional way of looking at the election. As the election draws nearer, we intend to update this research as needed.

Bill O’Grady

April 21, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

[1]An autarky is an economy that is completely self-sufficient, an economy closed to the outside world. The closest the world has to a working autarky is North Korea and even this economy has some contact with the outside world. Although autarky is rare, it is not unusual for a nation to try to attain self-sufficiency in specific industries, such as defense or agriculture.

[2]See Cynamon, Barry and Fazzari, Steven, “Inequality, the Great Recession and Slow Recovery,” January 2014.

© Confluence Investment Management