Aside from sleeping, Bob loved nothing more than to follow me from room to room making sure I was OK. It got to be a little much at times, especially when entering and exiting the shower. I’m not a particularly shy guy, but then why was a female cat named Bob checking me out all the time? Her obsession carried over to the TV, sensing when I was on CNBC and paying apt attention no less. I often asked her about her recommendations for pet food stocks, and she frequently responded – one meow for “no,” two meows for a “you bet.” She was less certain about interest rates, but then it never hurt to ask.

But before Bob, there were a number of loving pets in the Gross household. Most of you have had some as well; loved, and then lost them. For the Grosses there was Honey the golden retriever of all time, or at least the 20th century champion. She roamed the neighborhood in the more relaxed 1980s, bringing home stale loaves of bread like they were floating ducks on a pond. It wasn’t the bread so much (although it was that), as it was the praise for a good “find” and a pat on the head. Honey also loved rocks, some so big that it seemed her jaws would crack from the weight. Retrievers love retrieving, even if they’re loaves of bread or rocks. And then there was Wiggles and Daisy and Budgie – lovable pets every one of them and perhaps just as importantly – pets that loved us. I know you’ve had some too. So here’s to them and here’s to Bob. We buried her ashes in the backyard. Her gravestone reads just – “Bob”. What a girl, what a kitty girl that Bob.

Stanford’s Professor Emeritus William Sharpe was one of the originators of the capital asset pricing model, a class I took on the way out the door at UCLA’s Anderson School of Management and barely passed. A “C-” in business school is really an “F.” Guess I flunked it. He had another idea later known as the “Sharpe ratio” or, as amended, the “information ratio.” His logic said that higher returns from riskier assets such as stocks or high yield bonds must in some way be measured against their up and down volatility, and his ratio tries to do that for entire asset classes measured against Treasury Bills as well as individual portfolios measured against various indices. The higher the Sharpe ratio the better in general, and a ratio of .5 was generally considered an acceptable measure of an asset’s expected return vs. Treasury Bills or a manager’s ability to outperform an index over time via the “information ratio” hybrid.

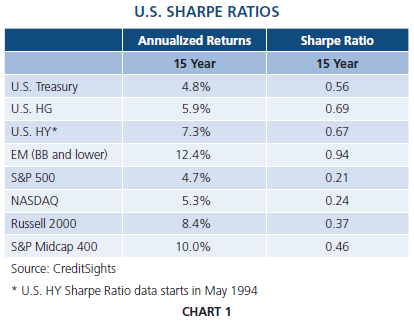

Chart 1, courtesy of an exhaustive study by CreditSights, shows Sharpe ratios for various asset classes over the past 15 years. All assets shown in the chart exhibited positive Sharpe ratios. In a sense this is just a history lesson. The chart says that even when volatility (risk as commonly accepted) is accounted for, when those sleepless nights during 2000’s dotcoms or the panic of 2009 is factored into the wrinkles on your aging face, that you were better off holding anything but cash. Well yes, such is the long-term history of capital markets as we know them. “Assets for the long run” would make for a thin but rather informative book. Write one!

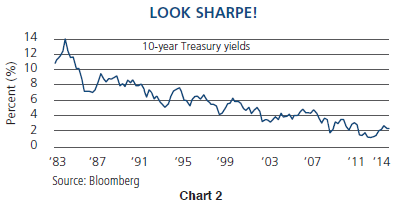

But on one of those thin pages the prospective author should introduce the caveat that the past 15 or even 30 years have been a rather remarkably short and non-volatile period of time, and future Sharpe ratios or other measures of risk/return may not exceed Treasury Bills in the same amount as before. A rather familiar graph of 10-year Treasury yields as shown in Chart 2 would hint at this. What I hope the reader will note is not only the dramatic decline in yields since the early 1990’s but the relative linear (non-volatile) path that they followed. Granted, for other asset classes such as stocks, there was 1987 and the aforementioned dotcoms and subprimes, but the linear path is clear: higher asset prices over long periods of time generated in part by the steady decline of 10-year Treasury yields to a 2012 bottom of 1.39%. A Bull Market almost guarantees good looking Sharpe ratios and makes risk takers compared to their indices (or Treasury Bills) look good as well. The lesson to be learned from this longer-term history is that risk was rewarded even when volatility or sleepless nights were factored into the equation. But that was then, and now is now.

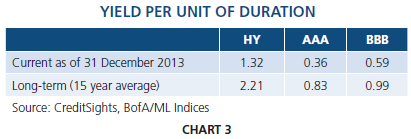

What Chart 3 implies is that today’s reward relative to risk – yield per unit of duration is more or less half of what it has been for the past 15–20 years. In order to get the same yield today for a single unit of duration for AAA, BBB, and HY bonds, an investor has to take twice the price risk! Since duration and correlated maturities are simply measures of interest rate risk, that may simply be pointing out that yields are historically low, and yes – they still are. But in order to capture other elements of return such as credit, curve, volatility and currency, the average bond investor must generally attach those elements of “carry” to a bond with a duration. Swaps, CDS, and FRN’s provide a partial escape but for the cash investor, today’s yield per unit of duration is only half of the markets’ 15–20 year historical measure, and that is very, very low dear reader.

How to confront this? There are at least two ways at the extreme, I suppose. Either double your position – double your duration – and maintain the same yield as historically noted or maintain or even lower your duration as a concession to an overpriced market that may continue to suffer increasing yields and lower prices. Do you want to “double up to catch up” as Vegas blackjack dealers used to encourage me, or are you willing to suffer the lower yields, wait for “mean reversion” as do some of our competitors, and hope that the client cash outflows don’t cash you out before you have a chance to play another game? Future Sharpe ratios and investment management firms hang in the balance.

Well, as Bill Sharpe’s contemporary Harry Markowitz pointed out long ago, investing is a process of compromises involving diversification, and many times the compromise provides a return relative to risk that is more “efficient” than any other. If a portfolio were to seek a high Sharpe ratio using a Markowitz efficient portfolio, what might it look like today?

PIMCO recommends overweighting credit and to a lesser extent volatility and curve. Underweight duration. Although credit spreads are tight, they are not as compressed as interest rates, which are now in the process of normalization. While PIMCO agrees with Janet Yellen that such normalization will be a long time coming (the 12th of Never?), probabilities suggest that as the Fed completes its Taper, the 5–30 year bonds that it has been buying will have to be sold at higher yields to entice the private sector back in. The 1–5 year portion of the curve, beaten up recently due to Fed “blue dot” forecasts and Yellen’s “six months after” comments, should hold current levels if inflation stays low, but 5–30 year maturities are at risk. Overall, because 2014 should be a relatively positive growth environment, carry trades in credit, curve and volatility should produce attractive Sharpe/information ratios. Return expectations however, for all unlevered assets and Markowitz generated portfolios will be in the low- to mid-single digits.

And what would Bob have meowed? Well, like I wrote, she was always more certain about pet food stocks, but then maybe kitty heaven has given her some additional insight. I shall have to ask her in my dreams. Sometimes dreams come true you know.

“Bob” Speed Read

1) High Sharpe ratios have been due to a long-term bull market. They will be lower in future years, as will asset returns.

2) Yields per unit of duration are historically low – half of their 15–20 year averages as shown by CreditSights.

3) Favor credit spreads and to a lesser extent, curve and volatility carry trades.

4) Treasure your pets and all living things. Eventually we all stop living.

William H. Gross

Managing Director

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2014, PIMCO.

© PIMCO