(N.B. In this report, we are tackling the geopolitical impact of the 2016 elections. Given the size of the topic, it will be discussed over a three-part series. Due to business travel, the follow-on reports will not be consecutive.)

American presidential elections are important events, although not all are equally critical. Some elections occur during periods of relative tranquility, and elections with an incumbent running tend to have less drama.

However, as we survey the political landscape for 2016, the next presidential election could be historic. In our opinion, the last three presidents have been unable to create a consistent foreign policy that reflects America’s role as the unipolar superpower. The next president will probably not have the luxury of this lack of policy focus.

History suggests that, geopolitically, unipolar worlds don’t last indefinitely. Eventually, the burdens of global leadership become too great, or other powers combine to contain the dominant nation.

The Great Financial Crisis (GFC) in 2008 severely weakened America’s ability to sustain one of the key responsibilities of the reserve currency nation, the ability to act as the global consumer of last resort. Global growth is difficult to sustain when the reserve currency nation is less able to buy the world’s exports and supply global liquidity.

The second role, the military role, is also coming into question. One of the jobs of the superpower is to act, at least in part, as a “global policeman.” That doesn’t necessarily mean that the U.S. must intervene militarily everywhere when bad things happen. But, it does mean the U.S. should protect the sea lanes and maintain general global order. Maintaining order requires the U.S. to have a credible military deterrent, which means America has the military prowess to intervene virtually anywhere and a leadership that knows how to prioritize where to act.

Syria’s use of chemical weapons against civilians violated a self-imposed “red line” by President Obama. He failed to act on that violation.

Understandably, Arab nations in the Middle East are now unsure about America’s position in the region. The Arab Kingdoms have tended to rely on the American military for protection against unstable neighbors; in return, the Arab states generally provided stable oil supplies. After Syria (and, to a lesser extent, Egypt) and with negotiations underway with Iran, the Arab states fear that this protection, provided since Roosevelt, may be ending.

Russia’s military takeover of the Crimea did not respect Ukraine’s borders despite the fact that the U.S. signed an agreement in 1994 with Ukraine to protect the country’s borders in return for Ukraine giving up Soviet-era nuclear weapons.

Not only has Russia annexed part of Ukraine, but it still has troops mobilized on the Ukrainian frontier and appears to be sponsoring unrest in the eastern portions of Ukraine, the home of many ethnic Russians. Russian President Putin’s government has suggested that the protection of ethnic Russian minorities in the Baltics, Moldova and Ukraine are paramount and discrimination against these Russians will not be tolerated. Whether this means Russia will respond militarily is unclear. However, it does appear that Putin is quite comfortable creating regional ambiguity on this issue which may extend further into the former Eastern Bloc.

Meanwhile, in the Far East, China is becoming a restive power, trying to project influence into the South and East China Seas. It regularly threatens the Senkaku Islands, which are claimed by China but have been under Japanese control since 1895. China has also been claiming islands under the control of Vietnam and the Philippines.

In this report, we will begin by examining the economic challenges the next president will face, with a broad analysis of the issues of inequality and economic growth. In future segments, we will detail our view on American politics and how these divisions affect the economy and the superpower role (Part 2). In the last segment, we will analyze how this election season could bolster or end America’s superpower function depending upon how the politically powerful elites create coalitions to resolve the economic problem described in Part 1. We believe these can be solved in such a way as to support the superpower role or end it. If our analysis is correct, it should offer insights as to how the candidates are positioning themselves in terms of maintaining or ending the superpower role. As always, we will conclude with market ramifications.

The Economic Problem

Slow economic growth is plaguing the developed world.

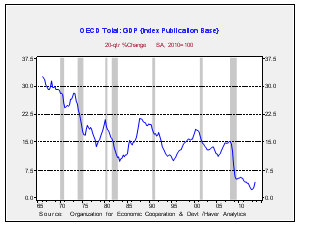

This chart shows the five-year growth rate for inflation-adjusted GDP for the OECD nations as a group. This growth rate fell sharply during the GFC and has essentially not recovered.

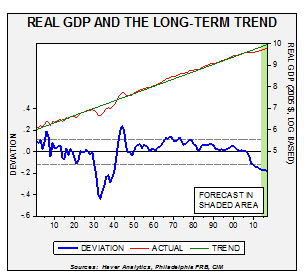

Taking a longer term look, detrended U.S. GDP growth shows profound weakness.

This chart shows U.S. GDP, log-transformed, regressed with a time trend. The lower line on the chart shows the deviation from trend. Note that there are two periods when GDP fell well below trend, the Great Depression and the GFC. Following the Great Depression, after a catastrophic decline in economic activity, the economy rebounded. The reason the economy declined so rapidly was that policymakers allowed asset values to drop sharply. Although this led to massive bank failures and asset liquidation, it did allow for new buyers to purchase these assets at deeply depressed prices. This supported the strong recovery. However, not all the recovery can be attributed to the “natural” process of letting asset values fall. The Roosevelt administration took aggressive steps to reflate the economy by devaluing the dollar against gold, and the increase in military spending before and during WWII clearly bolstered the recovery.

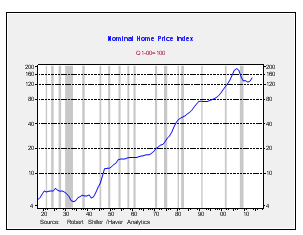

The current downturn has not been as deep as the Great Depression because policymakers took aggressive steps to prevent a wholesale decline in asset prices. Still, despite these efforts, the declines in both periods for housing were about equal.

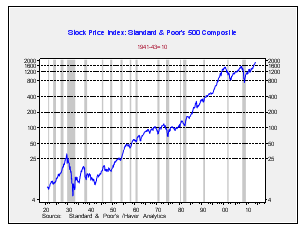

The peak-to-trough home price decline from 1925 to 1933 was 30.5% compared to a similar decline from 2006 to 2011 of 31.8%. On the other hand, the peak-to-trough decline in the S&P 500[1] was 84.8% from September 1929 to June 1932; this compares with the 50.8% decline from October 2007 to March 2009. Monetary and fiscal policy prevented a repeat of the Great Depression’s stock market crash during the GFC.

What is disconcerting about the current situation is that there appears to be no end in sight to below-trend GDP. On the GDP trend chart, we use the consensus forecast for real GDP from the Philadelphia FRB Survey of Professional Forecasters for the years 2015-17. These forecasts show no signs that the economy is recovering toward trend.

The current slow growth has been dubbed “the New Normal.”[2] Slow growth has caused significant distortions in the economy, especially in the labor markets. It has created a class of long-term unemployed that may prevent them from ever returning to meaningful work.

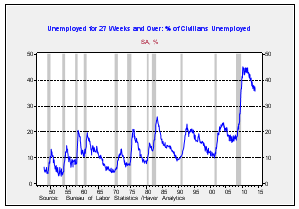

The chart below shows the percentage of workers who have been unemployed for more than 27 weeks. It currently represents 37.0% of all unemployed, peaking in April 2010 at 45.3%. As the chart indicates, as we approach the five-year anniversary of the end of the recession triggered by the GFC, long-term unemployment remains well above anything we have seen in the postwar economy.

What Causes these Economic Calamities?

Essentially, the primary cause of these events is leverage.

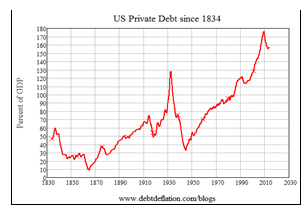

This chart, from Steven Keen, shows the private debt/GDP ratio from 1832 through 2011. Note how debt peaked in the early 1930s, declined sharply in the Great Depression and WWII, then steadily grew, accelerating rapidly after 1980.

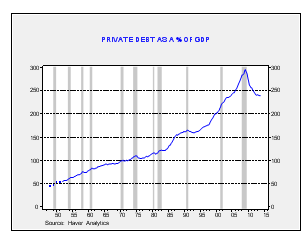

This updated chart shows that progress on deleveraging has actually slowed since 2011, meaning we are probably further away from achieving sustainable debt levels.

What causes this excessive borrowing? Income inequality appears to be the common element in both the Great Depression and the GFC.

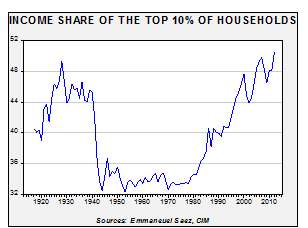

This chart shows the income share of the top 10% of American households, derived from IRS data. Note that in the 1920s, the top 10% was earning a high and rising share of total household income. The combination of high marginal tax rates, low global economic integration and regulation cut the top ten percent’s share from the early 1940s into 1980. The drop in marginal tax rates, along with deregulation and globalization, has led to a swing back to wider income distributions.

Why does income inequality lead to higher debt levels? There are two reasons. First, lower income households, striving to maintain their lifestyles, will take on debt to accomplish that goal. Second, income inequality tends to boost savings levels among the better off. These funds find their way into the banking system, which triggers banks to lend. Although there is an argument that moral failings are a key component of these debt increases, it should be noted that banks are in the business of lending money. That is where their profits come from. They will lower lending standards to meet their profit goals without other constraints and the savings from the wealthy will fund that activity.

In fact, as Marx suggested, if the less affluent households decide not to borrow, and refrain from profligate spending, the savings of the wealthy will scramble to find profitable investments, eventually causing the return on capital to decline to zero. If the less affluent don’t borrow, the savings of the wealthy become a drag on growth, triggering the “paradox of thrift.”[3]

So, if inequality can trigger debt crises, why does society tolerate it? We believe there are periods in which an economy needs to boost its productive capacity and needs a higher level of income inequality to meet that goal.

(Source: Peter Turchin, “Secular Cycles”)

This chart shows a long-term measure of inequality and wellbeing. The red line (the inequality line) on the chart measures inequality as the ratio of the nation’s largest fortune divided by median wealth. The blue line (the wellbeing line) is a detrended measure of the age of the first marriage, the ratio of production worker wages to per capita GDP, life expectancy and average height.

There is a clear inverse correlation between the two numbers. The tradeoff society makes to improve productive capacity and efficiency comes at the cost of reducing wellbeing for the masses. To encourage entrepreneurs to take risks, build companies and deploy new technologies, society will allow these people to become wealthy.

There are two clear cycles on the above graph. Wellbeing began to decline and inequality began to rise as America embarked on building the nation, expanding into the West and, since 1870, joining the industrial revolution. To encourage people to strike out into new territories, society had to allow those risk takers the possibility of becoming wealthy.[4] Similarly, during the industrial revolution, society had to incentivize people to take the risk involved in developing new technologies and production methods, allowing the potential for great wealth.

The cycle turned for various reasons. As discussed above, concentrations of wealth led to a debt crisis in the 1930s. Communism offered an alternative to democratic capitalism and was a threat to the established order. But, perhaps the most important reason was that widespread global development had led to a world with ample productive capacity; in fact, the world in the 1930s was bereft of aggregate demand.

WWII, at least in terms of debt and productive capacity, created a “reset.” Outside the U.S., global industrial capacity was mostly destroyed. And, America’s private debt was liquidated to a sustainable level as wartime government spending and rationing led households (and businesses as well) to higher incomes with little to buy. The extra income was used to boost savings and pay down debt.

The postwar administrations, from Truman to Carter, generally followed a plan to restrain productive capacity and support consumption. Disruptive technologies were mostly contained in the defense industry or the large industrial laboratories. High marginal tax rates discouraged entrepreneurship. Who would take the risk of starting a business with an untried technology only to face peak marginal tax rates that averaged over 80% during 1950-80? These policies created oligopolies and monopolies and supported organized labor. The market power that companies held allowed them to raise prices when labor costs rose; the rise in labor costs, of course, increased household income and supported demand. These policies, along with broader government income support (Social Security, Welfare, Medicare and Medicaid, etc.), also boosted demand.

By the 1970s, there was growing evidence that aggregate supply, the productive capacity of the U.S. economy, was becoming constrained. Inflation was becoming a persistent problem. In the middle of President Carter’s term, he appointed Paul Volcker to address the inflation issue and began the process of deregulating transportation and the financial service industries. These policies of deregulation, along with a general openness to globalization, effectively boosted capacity and slayed inflation. However, the cost of reducing inflation led to widening income differences and the subsequent explosion in private debt levels, which culminated in the GFC.

Ramifications

This report basically lays out the roots of the current situation of stagnant growth. We will take up the evolution of the political situation when we write Part 2 of this series, which is scheduled for April 14.

Bill O’Grady

March 31, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[1]Using monthly average index values.

[2]A term dubbed by Mohamed el-Erian, former CEO and co-CIO of PIMCO.

[3]First discussed in a book by Bernard Mandeville, The Parable of the Bees in 1714. He noted that privately moral behavior, like saving, can have a perverse effect of lowering growth. In logic, this is known as “the error of composition.”

[4]In 1833, Horace Greeley, an American author, was quoted as saying, “go West, young man.”

© Confluence Investment Management