- The past several years have seen multiple regime changes in financial markets in Europe, each dominated by different factors and requiring a distinct approach to fixed income investing.

- As spreads tighten to pre-2008 levels, it is now time to ask whether a shift in investment style is due.

- Macroeconomic developments and inflation expectations are likely to be key determining factors in whether 2014 will be a good year for European bond investors.

The dynamics of investing resemble a complex mathematical system, characterised by multiple factors contributing to the final outcome. At any given time, asset returns are determined by numerous competing factors: macroeconomic fundamentals, credit conditions, systemic risks, idiosyncratic risks of an issuer, policymakers’ actions and market flows, to name a few.

According to the Pareto principle (also known as the 80-20 rule), usually just one or two of these factors will dominate the others and can explain a large part of the moves in asset prices. However, difficulties arise due to the fact that the dominant factors are not always the same as they change dynamically over time. In Europe in particular, the past several years have seen multiple shifts among the dominant factors. Successful investing therefore means identifying the dominating factors ex ante and correctly analysing them.

Multiple regimes require different investment styles

The last five years have been challenging for investment managers as multiple regimes have dominated the European investment landscape, with each dominated by different factors requiring a different approach to fixed income investing.

At the onset of the debt crisis in 2008, asset prices were dominated by credit conditions affecting all risky assets. A defensive, liquidity-focused investment approach was the key to navigate that initial phase. As the crisis evolved during 2009, however, taking a defensive investment approach was no longer sufficient - credit analysis and idiosyncratic factors became important too. Investors who were able to analyse balance sheets and collateral to identify solid assets (i.e., “safe spreads”) were often able to buy securities at distressed levels and profit from their recovery.

Then, from 2010-2013, an evolving systemic debt crisis gradually came to dominate Europe’s economy. Individual balance sheets mattered less as policymakers’ actions became the key drivers of prices. In 2011–2012, investors able to analyse the reaction function of policymaker and central bank activities and to anticipate the effects on market dynamics were often able to better minimise losses arising from peripheral spread widening and sovereign restructuring. In turn, many of these same investors were able to benefit from the subsequent spread renormalisation that started in July 2012 following European Central Bank (ECB) President Mario Draghi’s “whatever it takes” speech at the Global Investment Conference in London.

Given the broad range of investment approaches required to tackle these numerous and varied regimes, many portfolio managers faced challenges to successfully navigate these different, and often difficult, periods. However, portfolio managers do not need to operate in a vacuum.

At PIMCO, both within our regional investment committees in Europe, Asia and the U.S. and during our quarterly economic forums, we investigate the sources of these dynamic and dominant macro and market factors. Such a disciplined approach enables us to better analyse evolving global scenarios, identify regime shifts and, ultimately, the approach informs our investment decisions. At the same time, from a bottom-up perspective, our investment teams benefit from the daily support of global specialists who continuously seek out opportunities from mispricing that may add value to client portfolios.

Almost back to pre-crisis levels

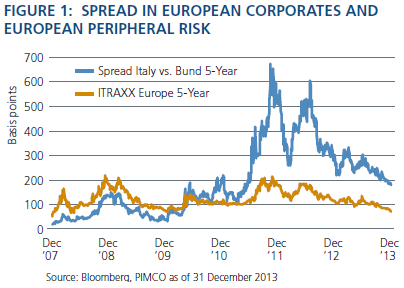

Since 2007, investment risk in European corporate markets and in peripheral sovereigns (such as Italy) has undergone notable shifts (see Figure 1).

After the volatile periods characterised by widening spreads, followed by tightening corrections in 2008-2009, 2011 and 2012, markets experienced a consolidation in 2013, characterised by a slow but continuous tightening in risk spreads. This trend has affected European corporate spreads as well as peripheral government spreads. Corporate risk, represented by the Markit iTraxx Europe index in Figure 1, is now trading at 73 basis points (as of 17 February 2014) – a level last seen before the default of Lehman Brothers in 2008.

While they still have additional room to tighten, spreads in European peripheral risk are also well below the peaks reached in 2011 and 2012. This long and stable regime has been driven by accommodating global central bank policies and, in particular, by the ECB’s implicit support for peripheral risk.

The transition is ongoing

At PIMCO, we have ridden this recent spread tightening wave by investing in short- and medium-term maturities of large peripheral countries, such as Italy and Spain. Although this position was still the main driver for spread carry (i.e., yield) in European portfolios at the beginning of 2014, the relative value of spread versus duration (duration is the sensitivity of a fixed income security to a change in interest rates) diminishes as peripheral spreads continue to tighten. While we expect 2014 to be another year of stability for spreads, it is now time to ask whether the nature of this spread risk has changed, and if therefore a shift in investment style is due.

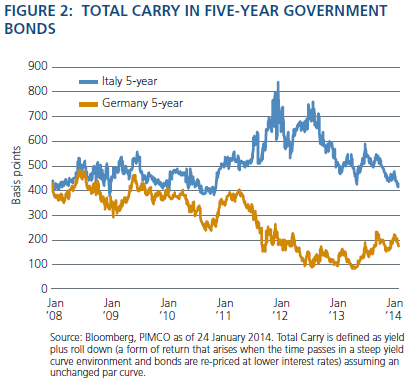

For example, the total carry of investing in five-year Italian government bonds versus the total carry of investing in five-year German government bonds (see Figure 2) illustrates how these spreads have narrowed.

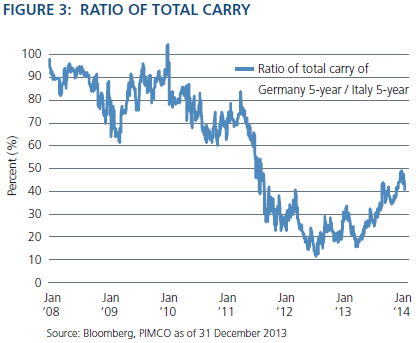

We can think of a position in Italian government bonds as a position in European interest rates plus a premium component due to peripheral risk. Comparing both, the total carry of Italian government bonds and German government bonds can provide a rough estimate of the relative proportion of these two risks, as illustrated in Figure 3.

While up to 80% of total carry was due to peripheral risk twelve months ago, today this proportion has shifted down to 50% of total carry, with the other half directly coming from the interest rate component. This change in relative proportion has been driven not only by spread tightening in the periphery, but also by the increase in interest rates in core countries. This is a key point: As spreads tighten and recede to low levels not seen since before the onset of the global financial crisis in 2008, the nature of carry is also changing. We are now experiencing yet another regime transition.

From the bottom-up perspective, we place an even greater emphasis on analysing potential opportunities to identify where value in peripheral spreads is still available. For example, we recently increased exposures in countries such as Slovenia, where we think the outlook for the country after banking recapitalisation is positive and current prices provide good compensation for liquidity. In the non-sovereign space, we continue to evaluate opportunities in Spanish covered bonds, whose spread is still wide versus Spanish sovereign debt and will likely benefit from the consolidation of the local banking system.

From the top-down perspective, we are structuring our portfolios to take into account a shift from a regime dominated by tightening peripheral spreads driven by supportive central bank action into one dominated by the direction of interest rates driven by the eurozone’s macroeconomic outlook. We expect the macroeconomic view in Europe, and in particular the outlook for inflation, will be the key determining factor in whether 2014 will be a good year for European bond investors.

Expectation for low inflation suggests stable, positive bond returns

Inflation in Europe is lower than expected, both at the headline and core levels. We believe that the economics of internal devaluations will likely maintain very low inflation levels in Europe’s peripheral economies, as well as in France. Recent declines in wage growth and core inflation suggest that Germany will provide insufficient compensation in the year ahead.

Aside from potential price peaks for oil and food, we should therefore expect eurozone inflation to remain comfortably low for the foreseeable future. The absolute return of the Barclays Capital Euro Aggregate Index has been 2.08% year-to-date (as of 24 February 2014), with a yield-to-maturity currently at 1.63%, while its carry is 2.41% (as of 26 February 2014).

The combination of a very low inflation and weak recovery in the eurozone mean that the ECB will likely lag the U.S. Federal Reserve in removing monetary accommodation. It remains unclear how tolerant the ECB would be to low inflation over an extended time period; at a minimum, we would expect the ECB to implement more unconventional easing measures if inflation should decline further. As such, we would expect European bonds to at least earn their carry with the potential for higher returns for the remainder of 2014 if a further fall in inflation induce the ECB to act sooner than later.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

© 2014, PIMCO.