N.B. This is our last report for 2013. The next report will be published January 6, 2014.

As is our custom, we close out the current year with our outlook for the next one. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international situation in the upcoming year. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

Issue #1: America’s Strategic Drift

This issue has dominated our thinking for the past several years. Essentially, the U.S. has struggled with developing a foreign policy strategy since the end of the Cold War. Although terrifying, the Cold War at least led to a consistent strategy; essentially, communism had to be contained and all foreign policy decisions had to face that test. That doesn’t mean there were no policy disagreements during the Cold War. Clearly, significant policy differences existed between Presidents Carter and Reagan. However, the general requirements of defending the Free World offered a strategic constraint that all administrations followed from Truman to G. H. W. Bush.

The West prevailing in the Cold War was one of history’s greatest victories. Not only did the world reduce the odds of nuclear holocaust, the primary competitor for capitalism and democracy, totalitarian communism, was thoroughly discredited. Francis Fukuyama, a political theorist, argued that the end of the Cold War marked the “End of History,” meaning that there was no other system for government and development but democracy and free markets.

However, the loss of the Soviet Union as an adversary meant the U.S. needed a new strategic vision to conduct foreign policy. To date, it hasn’t been able to settle on one. President Bush maintained a traditional superpower stance in policy by creating a broad coalition to remove Saddam Hussein’s forces from Kuwait. He also managed the unification of Germany while assuring European allies that the newly merged country would not be a military threat. He also supported the breakdown of the Soviet Union without triggering a complete collapse of Russia.

However, Bill Clinton was able to campaign against Bush by framing the president as being unconcerned about the domestic economy. The U.S. economy’s recovery from the 1990-91 recession was the first of the so-called “jobless recoveries” of the past two decades. The weak economy became a major political liability for President Bush, and so, despite winning the Gulf War, Bill Clinton won the presidency in 1992. As promised, Clinton did focus on the domestic economy, paying less attention to foreign policy, especially in his first term. Clinton did become more involved in foreign policy in the second term, conducting military operations against Serbia and nearly accomplishing a peace accord with Israel and Palestine.

However, there was no obvious new foreign policy strategy that emerged during Clinton’s presidency.

The G.W. Bush administration began with the concept of operating a “humble” foreign policy, but this aim was quickly overtaken by events. The attacks on the World Trade Center and the Pentagon on 9/11 led to an aggressive, military-oriented foreign policy designed to prevent another major terrorist attack on the U.S. This led to wars in Afghanistan and Iraq resulting in serious opposition from other nations.

The Obama administration’s foreign policy initially began differently from his predecessor. He withdrew American troops from Iraq and the conflict in Afghanistan is winding down. However, he did involve the U.S. in the ouster of Libyan leader Moammar Gaddafi. Perhaps the most controversial of his policies has been the heavy use of drone strikes against suspected terrorists in various parts of South Asia and the Middle East.

However, despite all this activity, there is scant evidence that any of the last three presidents have created a lasting foreign strategy. Because of the lack of strategy, the U.S. has been reactive, not proactive. Presidents have responded to problems without regard to how these actions fit into a broader strategy. The attack on Iraq is a prime example. Clearly, no plans were made on how to address the power vacuum that developed after Saddam Hussein was ousted from power. The same could be said for removing Gaddafi from Libya.

Currently, the U.S., for better or worse, is the only global superpower. It provides the reserve currency and, from a military standpoint, outspends the next 25 highest defense budgets combined. Although China complains about the dollar, it is not prepared to take on the reserve currency role. It does not have an open capital account and is clearly unprepared to play a global leadership role (its paltry initial contribution of $100k to the recent victims of the Philippines typhoon has been roundly criticized—it should be noted that it has increased its donation to $1.4 mm).

Until a workable, sustainable strategy is developed, both adversaries and allies will be unsure of U.S. actions. This will increase the odds of miscommunication and geopolitical accidents.

Issue #2: Chinese Maritime Expansion

As China’s economy reaches large country status, it is trying to expand its influence in its surrounding coastal waters. This has led to persistent tensions with Vietnam, Japan and the Philippines. Although China does not have a true “blue water” navy, it can, in some cases, “bully” its smaller neighbors.

The chances of miscalculation are rising. China has recently implemented an Air Defense Identification Zone which includes the disputed Senkaku/Diaoyu Islands in the East China Sea. The U.S., Japan and South Korea have all sent military aircraft into the airspace without warning to signal to China that they don’t accept this claim. There has been an increase in military incidents between Japan and China over these islands. In addition, China has claimed other islands that Vietnam and the Philippines also claim.

There are two factors that make a military accident more likely. First, there appears to be little formal military contact between China and these other nations. There are no easy ways to contact the other side in a dispute to assure both parties of the non-aggressive intentions of the other. Thus, a rogue event could escalate into an unwanted military confrontation. Second, relating to the first issue, U.S. allies in the region are not confident of American backing. U.S. policymakers are reluctant to offer these nations full support, fearful they will use this alliance as an excuse to aggressively react to Chinese incursions. At the same time, if the support appears too tepid, these nations may be inclined to accommodate China, undermining U.S. influence in the region. Although the U.S. is signaling a “pivot” to Asia, the degree of commitment is under question and the more opaque the support, the greater the odds of a military mistake.

Issue #3: The Rise of the Populists

Income and wealth inequality is growing.

This chart shows the share of income captured by the top 10% of income earners for the U.S. At just over 50%, this is the highest income disparity on record since the inception of the income tax in 1913.

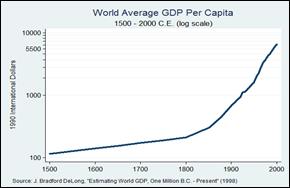

Interestingly enough, this isn’t just a U.S. problem and income inequality has increased over time.

This chart shows the Gini Ratio1 for the world for various years, starting in 1820. Note the jump from 1820 to 1850. This period represented the First Industrial Revolution (harnessing steam) and led to rapidly expanding incomes from those able to use the new technology. It was in 1848 that Karl Marx wrote his Communist Manifesto during a period of high civil unrest. Rising income disparities along with the disruptive effects of new industrial technology fostered riots across Europe. Marx assumed, in 1848, that capitalists would further impoverish workers and that, eventually, workers would rebel. What he didn’t foresee was the tremendous growth that capitalism fostered.

However, it should be noted that inequality rose steadily until the 1950s when disparities stabilized. They rose again in the 1980s as deregulation and globalization expanded, peaking in 2002. Although the latest data available is from 2007, when disparities did shrink, we suspect they have widened again.

Soon after 1848, global GDP growth soared to levels never seen in human history. One reason capitalism triumphed over communism, despite growing income inequality, was that the former delivered exceptional growth. Envy tends to be contained when growth is rising.

However, as we examined earlier (see WGR, The Gordon Dilemma, 8/12/2013), there is growing evidence showing that slower growth may not just be a cyclical problem. Larry Summers spelled out in a recent short speech that this slow growth may be with us for a long time. When growth stalls, income inequality becomes a political problem.

Over the past three decades, there has been a general policy consensus that deregulation and globalization (which includes both free trade and generally open immigration) will lift growth, subdue inflation and relieve geopolitical tensions. The fall of the Berlin Wall, as noted above, confirmed this position. That isn’t to say that there wasn’t opposition to these policies. However, as long as growth remained robust, most voters were willing to accept the policies. It should also be noted that these policies rely on the U.S. as the global military and financial superpower. Without this power, international order is likely to disintegrate, and with it the risks of war and other calamities increase.2

We are seeing in numerous countries and across the political spectrum a growing opposition to the status quo. The anti-globalization, anti-capitalist left wing has been in place for years despite the fall of the Berlin Wall. The Occupy movement is the latest expression of this trend. At the same time, there have been anti-globalization rumblings from the right. The National Front party in France is better known for its anti-immigration position but the party also wants to leave the Eurozone and restrict trade as well. Right-wing, anti-euro and anti-immigrant parties are rising across Europe. In the U.S, there has been a strain of anti-immigration on the right since the “know-nothings” of the 1850s. However, among libertarians (who are usually labeled on the right although that characterization can be disputed), there is an anti-globalization bent. Rand Paul and his father, standard bearers for the movement, have opposed American military activities, which are integral not just to America’s superpower status but also to globalization.

Weak global growth tends to support anti-trade, anti-immigrant and anti-globalization movements. Globalization has provided significant benefits to the world. Inflation has been lower due to the efficiencies that come from trade (along with deregulation, which supports the rapid integration of new technology). Emerging economies have enjoyed historic growth—the rise of China is clear evidence of this factor. However, perhaps the best argument for globalization comes from history; from 1920 into the Great Depression, globalization retreated because Britain did not have the economic capacity to maintain its superpower role and the U.S. was unwilling to accept the mantle. The rise of authoritarianism and WWII were a direct result. Essentially, globalization reduces the risk of major war.

The populists on both sides of the aisle feel they are the losers in globalization. Historically, their anger has been quelled on expectations of rising growth. However, as growth stalls, calls to restrict trade and immigration are rising. A recent Pew poll indicates a rather remarkable rise in isolationist sentiment. In response to the statement, “the U.S. should mind its own business internationally and let other countries get along the best they can on their own,” 52% of those polled agreed, the highest on record dating back to 1964.3 If the political classes cannot resolve these pressures without succumbing to the temptation to reverse globalization, the world will be at much greater risk for major regional conflicts, further declines in economic growth and rising inflation.

Issue #4: The Remaking of the Middle East

The current boundaries in northern Africa and the Middle East were mostly drawn by colonial powers. The borders were best suited for these European nations to maintain control. Ethnic and religious groups were often divided and minorities tended to be put in power by colonialists to ensure loyalty. As independence emerged, the new rulers tended to keep the same borders in place, fearing that allowing them to reach their natural state would be chaotic. However, to maintain these artificial states, most of the governments became authoritarian. That was the only way to maintain order.

The Arab Spring has unleashed a wave of democracy movements that have, thus far, been fraught with risk. In Egypt, the military has reasserted control after an Islamic government was ousted in a coup. Civil conflict has emerged in Syria; violence in Iraq is escalating. Libya may devolve into at least two, and perhaps three, separate nations.

In the long run, a shifting of borders to better reflect ethnic and religious differences would likely create a more stable situation. However, getting to that point is fraught with risk. The potential for conflict and oil supply disruptions are high. To some extent, the Obama administration’s decision to begin the process of normalizing relations with Iran is likely based on the idea that an Iran that is no longer an enemy would be more likely to assist in stabilizing the region.

There is still great potential for ongoing insurgencies and civil conflicts that are, essentially, Sunni versus Shia, Arab versus Persian, etc. As U.S. influence declines in the area, the odds of conflict will likely rise.

Issue #5: The Rise of Kim Jong-un

North Korea is always a tough country to understand. It is a closed society run by a heredity dynasty. The latest leader from the ruling family, Kim Jong-un, took power in December 2011 after his father, Kim Jong-il, died. Given his young age (he is thought to be around 30 years old) and lack of formal grooming for power (unlike Kim Jong-il, who was prepared for the role by his father, Kim Jong-un’s dad waited until he was very sick before selecting one of his younger sons for succession), it was expected that his uncle, Jang Song Thaek (who was married to Kim Jong-il’s sister), would act as regent until the new leader became established.

Over the past two years, Kim Jong-un has been steadily creating his own power base, gradually purging leaders loyal to his father. Last week, this purge continued with the reported execution of the regent, his uncle.

At present, we believe that the North Korean leader’s decision to execute his regent is nothing more than another part of the process in establishing his own control. Jang’s career had been rocky; neither Kim Jong-il nor his father, Kim il-Sung, trusted Jang, and worried that he was trying to create his own power base. Over the past year, Kim Jong-un had been steadily undermining Jang’s power. The decision to execute his uncle follows a decision earlier this month to purge him from office.

North Korea still faces two major tasks. First, the young leader needs to enhance the role of the party at the expense of the military. During his father’s reign, the military’s power rose and now represents a risk to the regime. Second, the North Korean economy needs to grow, which is only possible with outside investment. Kim likely wants to have complete control of the country before he embarks on opening the economy to outside influences. His uncle had close ties to China. It is possible that the young leader decided that these ties were a threat to his leadership and control. In addition, North Korea has a love/hate relationship with the Chinese. Although China is critical to the North Korean economy, the Kims have traditionally resented outside influences on their regime. Thus, Kim Jong-un may have decided it was necessary to remove Jang from the scene in order to control the relationship with China and to discourage other power centers in North Korea from developing close ties to the Chinese.

North Korea makes the list because the opaque nature of the regime means we are never completely sure of what is actually occurring. If the execution of Jang represents the beginning of leadership uncertainty, North Korea could destabilize the northern Pacific Rim.

Ramifications

In our opinion, these five issues are the most geopolitically important for the upcoming year. In general, geopolitical events tend to be bearish for risk assets and so, if these concerns become critical, they will tend to weigh on equities and higher credit risk debt. On the other hand, if any of these conditions were to worsen significantly, it would tend to boost Treasuries and, in some situations, commodities. Although gold has clearly fallen out of favor this year as deflation worries increase, deglobalization would tend to support reflation and commodity prices.

Policymakers are facing difficult conditions. We expect monetary policy to remain universally accommodative, if for no other reason than to run a tight policy now would trigger a rapidly appreciating currency and weakening competitiveness. The risk that policymakers will succumb to protectionism and reregulation remain high as well.

At present, as long as these issues remain relatively dormant, continued easy monetary policy should support risk assets. Investors should remain vigilant to the above detailed risks as the year progresses.

Bill O’Grady

December 16, 2013

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

1 The Gini Ratio is a ratio of income inequality. A reading of 0 indicates perfect equality and 1 indicates perfect inequality; thus, the higher the reading, the more unequal the income distribution.

2“Democracy and open markets have spread so widely in part because they have been defended by U.S. aircraft carriers.”—Charles Kupchan.

“International order is not an evolution, it is an imposition.”—Robert Kagan.

© Confluence Investment Management

© Confluence Investment Management