- Recent data suggest that mining investment is tapering, with the sector detracting from real growth in the first half of 2013.

- We see three possible growth scenarios: a handoff to the corporate sector; no handoff, with demand continuing to slow; or a handoff to the highly levered household sector, which would create long-term risks.

- Until we see meaningful signs of a growth handoff from the mining sector to a new balance sheet that has the capacity to expand, our base case calls for sub-trend growth and low interest rates, supporting bond prices over the cyclical horizon.

While the Federal Reserve gets to choose when to slow the pace of balance sheet expansion in the U.S., or when to “taper,” Australia does not have the luxury of controlling the balance sheet for the mining sector. Over the past 12 years, mining investment as a share of GDP has risen sixfold to nearly 7% (Figure 1), but recent data suggest that this balance sheet is tapering, with the sector detracting from real growth in the first half of 2013. To encourage a new balance sheet to step forward, the Reserve Bank of Australia (RBA) will have to keep interest rates low for an extended period, in our view, and likely lower them further to help smooth the transition away from mining-assisted growth over the cyclical horizon.

Which balance sheet, if any, will step up? We believe Australia faces three growth options over the next year, all with distinctly different policy and financial market outcomes − scenarios that could be called the good, the bad and the ugly.

Growth and taper of the mining sector

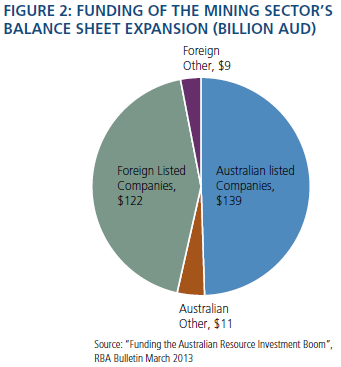

Between 2003 and 2012, the global mining sector is estimated to have invested A$284 billion in new projects or expansions of existing capacity in Australia. (See “Funding the Australian Resource Investment Boom”, RBA Bulletin, March 2013.) Importantly, a significant portion of this investment has been funded by foreign entities. As Figure 2 shows, there has been close to a 50/50 split between domestic and foreign entities, with 46% of this investment financed from offshore.

And as figure 3 shows, since 2011, the balance sheet expansion by the global mining sector in Australia has supported domestic demand when much of the rest of the economy was growing below trend.

However, the first half of 2013 has been a different story, with growing evidence that this balance sheet has begun to taper its support. In the six months to June 2013, mining investment actually detracted 0.5% from growth. With no new balance sheet stepping forward to drive growth, Australia grew by just 1.1% in real terms in the first half of 2013. Excluding the first and second quarters of 2011, which were impacted by the floods in Queensland, this is the slowest six months of growth since the financial crisis ended in 2009.

Growth options – the good, the bad and the ugly

The question now is what will happen as mining investment tapers and the RBA’s interest rate cuts filter through to the economy. We see three possible scenarios.

First, the good growth outcome the RBA is shooting for: Companies outside the mining sector begin to invest in their businesses again, allowing for a smooth handoff of growth from the mining sector. Unfortunately, we have yet to see this process take place, with real growth in non-mining business investment actually contracting over the year to June 2013 (Figure 4). Could the recent uptick in business confidence after the federal election be a sign of stronger investment intentions going forward (Figure 5)? Perhaps, but we remain skeptical. Survey measures of hiring intentions and capacity utilization remain at subdued levels, and we would need to see some sustained improvements in these measures before we would expect to see an increase in business investment. Additionally, the percentage of earnings that listed companies are paying out as dividends has continued to rise over the past 12 to 18 months, suggesting firms continue to prefer paying earnings back to owners rather than reinvesting in their own businesses.

Second, a bad growth outcome could eventuate in which demand continues to slow as the global mining sector tapers and no new domestic balance sheet steps forward to drive future growth. The first half of 2013 falls into this category, with the RBA responding by lowering the cash rate by 0.50% so far this year.

And finally, an ugly growth outcome could transpire where an unintended balance sheet steps forward attracted by low interest rates. In Australia, this would be the household sector, which remains highly levered by global comparisons. This ugly growth outcome would involve a temporary near-term boost to growth, but the increased leverage on household balance sheets from already elevated levels would create longer-term risks to the outlook.

The RBA would face a very difficult policy dilemma in this environment, constrained from providing the policy support required in other parts of the economy due to fears of creating imbalances in the household sector. This would prove a challenging policy environment not only over the cyclical horizon, but also over the secular horizon as growing imbalances in the household sector would also create growth risks and potentially ugly growth outcomes.

As we have expected in the New Normal deleveraging environment, there are no clear signs of this yet. In fact, real household consumption growth actually decelerated in June to its slowest year-over-year pace since the third quarter of 2009, and retail sales have grown just 1.9% over the 12 months to July, well below the 30-year average of around 6%. However, the potential for the household sector to expand its balance sheet is still real, particularly in light of the recent recovery in house prices. The Australian house price index rose 3.2% in the first six months of 2013, its quickest pace since the first half of 2010.

Investment Implications

What does this complicated outlook mean for investors? Until we see some meaningful signs of a growth handoff from the mining sector to a new balance sheet that has the capacity to expand, our base case calls for sub-trend growth outcomes in Australia. In this environment, we expect that the RBA will have to keep interest rates low for an extended period, and likely lower them further, supporting bond prices over the cyclical horizon.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market

This material contains the opinions of the authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO