- While developed market growth in several regions is picking up cyclically from low levels, overall global economic growth should remain subdued over the next several years.

- We believe credit spread tightening and rating upgrades are most likely for specific companies in industries and areas with strong growth.

- We see these “rising star” companies in the U.S. and European auto sector, the gaming, energy and chemical industries and in sectors tied to the U.S. housing market.

PIMCO’s global credit investment process focuses on leveraging our firm’s top-down macroeconomic outlook, bottom-up credit research and relative value analysis to identify attractive investments. Our top-down view suggests that while developed market growth in several regions is picking up cyclically from low levels, overall global economic growth is likely to remain subdued over the next several years. Global aggregate demand is unlikely to pick up materially given structurally high unemployment and elevated public sector debt levels. Meanwhile, emerging markets growth could slow due to tighter U.S. monetary policy over the near term as well as the difficult transition of public-sector-assisted to private-sector-led growth over the medium term.

Nevertheless, we do see a few areas of strength. As we discussed in our November 2012 Global Credit Perspectives, “Go for Growth,” we continue to favor investing in areas of the market that have above-trend growth dynamics. From a bottom-up perspective, we are also finding companies in areas with fast growth that we feel the rating agencies have misrated. Specifically, PIMCO views many of these investments as “rising stars” – credits with improving fundamentals that should see ratings upgrades over time.

Why growth is important

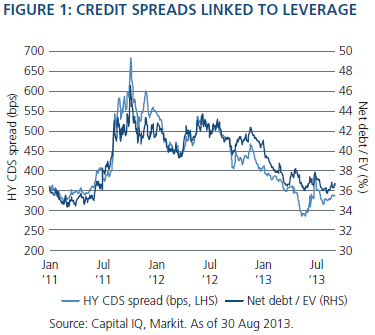

Investors should focus more on growth in their global credit selection. Simply put, growth is a powerful factor in enhancing profits and helping to aid the delevering of a company’s balance sheet. Typically, growth in revenue drives expansion in enterprise value (the market value of a firm’s debt plus equity), and free cash flow generation reduces net debt. As net debt-to-enterprise value falls, the company’s credit fundamentals improve. Over time, there is an increasing likelihood that credit spreads can tighten because the ratio of net debt-to-enterprise value is correlated to credit spreads (see Figure 1), since default risk tends to decline as leverage is reduced. In addition, the likelihood of credit rating upgrades increases as a company’s fundamentals improve.

Not surprisingly, the change in net debt-to-EV over the past year varies dramatically by industry (see Figure 2), with housing-related sectors and energy experiencing much stronger fundamental improvement and organic delevering than metals and mining.

Ratings and looking forward

While PIMCO’s credit ratings are forward-looking and derived independently from credit rating agencies’ ratings, we pay attention to credit rating agencies mainly from the perspective of market technicals. Specifically, credit rating agency upgrades can lead to rating migration, for example from a high yield, or BB+ rated credit, to an investment grade, or BBB- rated credit, which then causes benchmark-oriented or passive investors to buy these “rising stars.”

PIMCO’s investment strategy has always been focused on looking forward and anticipating credit rating upgrades before they occur. We look into the future in our credit selection and model company financials by making projections and forecasts out several years from today. Our strategy is to buy companies that are improving from a credit perspective before the market – and the credit rating agencies – anticipates these developments. Our longer-term, secular approach and forward views are designed to help us to capture many rising stars before other investors, who may have a shorter-term investment horizon or orientation.

Globally, we see a few areas where growth is likely to be sustained over the medium term. In the U.S., autos and housing should continue to grow above trend over a cyclical horizon, mainly due to pent-up demand. In Europe, the auto sector is likely bottoming and a few specific credits should benefit from a gradual recovery. In addition to these more cyclical areas, we see longer-term or secular growth in the U.S. energy and chemical industry, as well as in Asian gaming.

Let’s turn to each of these areas given our view that many rising star investments may be available in these industries.

Autos

The U.S. auto industry is experiencing strong earnings growth as a result of financial and operational restructurings and significant pent-up demand coming out of the recession. Cyclically, autos are rebounding from a depressed level (see Figure 3), which allows for a strong recovery and healthy growth. U.S. light vehicle sales reached a seasonally adjusted annual rate (SAAR) of 16 million units in August 2013, up 10% versus last year. Ford plans to increase production by 7% in the fourth quarter from a year earlier to meet strong demand.

Supply and demand factors help explain the sector’s strong growth profile. On the supply side, American automakers effectively downsized and restructured their business over the past few years to the appropriate level of demand. The industry’s focus on healthier balance sheets, cost control and consolidation allowed companies to invest for the future, resulting in new products, fresh car designs, stronger brands and an expanded lineup of fuel-efficient vehicles.

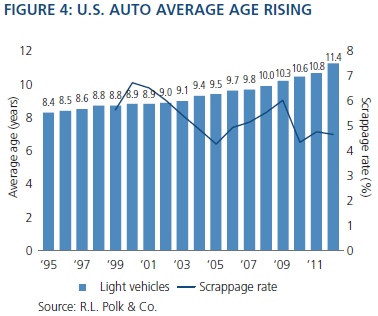

On the demand side, five factors are driving strong top-line auto sales today in America. First, the need to replace older cars and trucks is high, as the average age of the fleet is over 11 years (see Figure 4). Second, consumers are exhibiting a strong preference for fuel efficiency – even within the full-size truck category. Third, credit availability has improved at auto finance companies due to a reduction in credit losses, low interest rates and easier access to credit, which these companies have passed on to consumers. Fourth, consumer confidence has improved due to a gradual decline in the unemployment rate, a rising equity market and higher housing prices. Finally, strong growth in the U.S. residential construction and energy industries is driving healthy demand for new truck sales (Ford sold an amazing 71,115 F-series pickups in August 2013, which the company said worked out to one truck every 42 seconds).

While industry fundamentals have turned in the U.S., the European auto industry remains depressed. For example, car registrations in Europe have dropped by over 25% – and over 50% in some markets – from pre-crisis levels. Nevertheless, we see signs of a modest recovery as Europe stabilizes, and we expect an eventual turnaround for companies that have been able to downsize to today’s lower demand levels and manage their balance sheets. We feel a few European auto and auto parts companies are well positioned to benefit from an improvement in profitability and free cash flow as the European auto cycle turns.

Overall, in the U.S., we continue to favor a group of auto and auto finance companies with improving fundamentals. In Europe, we are targeting a select group of companies that have strong competitive positions through their brands and technology. In both regions, we expect over the medium term to see an increasing number of companies demonstrate the ability to grow top-line and bottom-line results. Importantly, through higher profits and increased cash flow, several auto and auto finance companies have improved their ability to delever, which should ultimately result in more ratings upgrades in the U.S. and the start of an upward rating trend in Europe.

Gaming

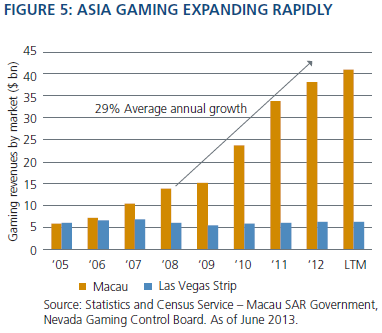

The Asian gaming industry remains an attractive area to invest in given strong secular growth prospects. In Macau, the market should continue to benefit from increased visitation from mainland China as well as significant infrastructure investment. Overall, the Macau gaming market has grown from roughly $6 billion in annual revenues in 2005 to approximately $41 billion today (see Figure 5).

We believe Macau offers investors an attractive way to invest in the growth of the Chinese consumer. Despite exceptional growth over the past 4½ years, the Chinese government is making significant infrastructure investments to improve access to Macau from major cities throughout China. These investments include new bridges, ports, high-speed rail, highway expansions and visitation facilities, which will all help to expand visitation. Several new casino properties are being developed in the emerging Cotai area of Macau, referred to as the Las Vegas Strip of China, to serve growing demand.

We believe a rising middle-class Chinese consumer will lead to significant and sustainable double-digit growth in the mass market in Macau. We similarly believe that growing wealth throughout Asia, combined with improving infrastructure, will lead to increasing demand from Asian consumers for both Macau and Singapore gaming.

PIMCO is invested in several gaming companies with a significant presence in Asia, and we remain constructive on the industry. We believe that the above-trend growth will continue for many companies in the sector, leading to ratings upgrades for bond investors.

Energy and chemicals

PIMCO has been focused on the U.S. energy revolution for years. As we described in our March 2012 Global Credit Perspectives, “Game Changer,” we see significant opportunities to invest in energy companies that offer superior growth profiles.

U.S. crude oil production is now growing at 15% or more annually, the fastest growth rate in over 40 years (see Figure 6). This growth rate is the catalyst for further credit ratings upgrades for companies in the exploration and production (E&P), gathering and processing, oil field service and pipeline sectors.

We continue to find numerous opportunities across the broad energy and chemicals sector and believe above-trend growth is likely, particularly for the many companies we have identified through our bottom-up research.

Housing

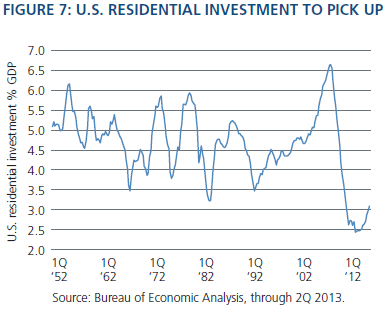

While gaming and energy are experiencing solid secular growth, the U.S. housing market is growing because it is recovering cyclically. U.S. residential investment spending remains at relatively depressed levels (see Figure 7). While U.S. housing prices have moved up over the past 18 months, housing starts have picked up only moderately as new construction of single-family homes has been held back due to builders exercising caution, as well as land constraints in some areas of the country. Thus, U.S. housing inventories remain very low (see Figure 8) and household formation should pick up over the next several years given an improving labor market and supportive population growth. As a result, U.S. housing and residential investment spending should grow faster than the overall U.S. economy, absent a significant and unexpected rise in mortgage rates from current levels.

We believe the pace of U.S. housing price appreciation should moderate to a level of mid-single-digit gains over the next two years. While that pace will be much slower than the double-digit gains over the past 12-18 months, tight supply, continued pent-up demand, gradually improving credit availability and strong long-term fundamentals should continue to support the market.

While new construction activity is an important driver of housing, we would also highlight that new homes sales have represented less than 10% of total housing sales over the past 5 years, with the remainder comprising existing homes that require repair or replacement (e.g., a new roof or a new washer/dryer) or are under consideration for remodeling by the homeowner. We believe stabilizing home prices and higher U.S. home equity should encourage more remodeling activity (see Figure 9) given that consumers tend to be more willing to reinvest in their home when household equity has increased and their expectation is that housing prices will go up over time.

Our investments in the U.S. housing market have focused on non-agency mortgages, banks and homebuilders that stand to benefit over time from rising U.S. housing and land prices. In addition, we continue to find select opportunities in building materials, home improvement, lumber and appliance companies that benefit from an improved outlook for new housing construction and remodel activity.

Growth and rising stars

PIMCO’s longer-term approach to investing in global credit leverages our top-down and bottom-up analysis, as well as our valuation skills to identify rising stars through independent research in specific companies that have above-trend growth profiles. While the global economy’s overall growth rate will likely be moderate, several industries and regions may experience healthy growth. Today, we believe credit spread tightening and rating upgrades are most likely for specific companies in these industries and areas with strong growth.

The future remains encouraging for investors who have the ability to find rising stars since these companies have strong growth profiles and, importantly, a greater ability to organically delever. Our secular and longer-term approach to investing in companies allows us to look forward and be anticipatory in our search for growth and future rising stars. In terms of specifics, we believe rising stars are likely in the U.S. and European auto sector, the gaming, energy and chemical industries and in sectors tied to the U.S. housing market.

Mark Kiesel

Managing Director

September 10, 2013

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Investors should consult their investment professional prior to making an investment decision.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. A rising star is a corporate credit issuer viewed as improving in credit quality across the investment grade/high yield divide.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

© PIMCO