- While commodity price appreciation won’t likely mirror the supercycle, this shouldn’t necessarily imply a negative view on commodity returns going forward.

- We believe commodity prices are at reasonable levels from a long-term valuation perspective. In addition, the roll yield from investing in commodities is the highest it’s been since 2005.

- The outlook for commodity returns today seems broadly consistent with historical returns, and commodities remain an important tool for hedging inflation risk.

From the late 1990s until the 2008 financial crisis, most commodities experienced double-digit annual real (i.e., inflation-adjusted) price growth, a period known as the commodity “supercycle.” The price of oil rose 1,062%, copper rose 487% and corn rose 240% as growing emerging market demand finally caught up with years of underinvestment in various commodity markets (source: Bloomberg, 31 December 1998 to 30 June 2008). But poor relative performance of commodities to equities year to date has led to some media reports that read like an obituary for the commodity markets. The Economist has even suggested that it is oil demand, rather than oil production, that has peaked and will decline, particularly now that shale has emerged as a viable source of supplies.

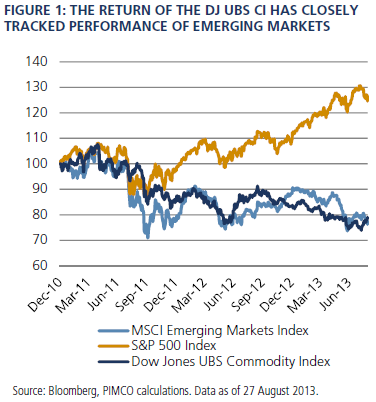

We believe the deceleration in emerging market growth relative to the U.S. has also helped strengthen the U.S. dollar at a time when the prospect for reduced stimulus from the Federal Reserve was already a tailwind for the dollar. With commodities largely priced in dollars, a stronger dollar depresses those prices, which is particularly true for commodities with large production costs in non-dollar currencies.

What drives commodity returns?

Let’s say a typical portfolio is dominated by equities and nominal bonds, which tend to respond poorly to unanticipated inflation. Adding commodities to such a portfolio may serve as a hedge during inflationary periods. While some recent studies have questioned the diversification that commodities can provide, we believe that these studies are overly focused on very short periods of time when inflation was stable. Amid stable inflation, commodity performance is typically driven primarily by changes in growth expectations, and in particular those of emerging markets. In such an environment, commodity performance will likely show a higher correlation with equities. The potential benefits of commodities become clearer, however, when inflation rises because the prices of commodities also tend to rise, while the impact on the present value of future corporate earnings is much less clear.

Even if commodities have diversification benefits, to understand how much to allocate to commodities in a portfolio requires some estimate of forward-looking returns. To do this, we need to understand the three components that make up commodity returns and determine some baseline for what investors could expect going forward. The return from investing in commodities via futures contracts is a function of

- The changes in price of the underlying commodity (spot return);

- The “roll yield” return from rolling from one futures contract to the next (for example, if the price of an oil futures contract is $110 for the front (prompt) month and $109 for the next (deferred) month, then the investor will realize a profit of $1 if there is no change in the spot price over the month); and

- The return of the underlying collateral that backs the futures contracts.

In the long run, commodity spot prices have historically tended to increase on average at roughly the rate of inflation, with commodities like oil and those found in the ground generally increasing at a slightly faster rate than inflation, and those that can be grown in the ground increasing at a slightly slower rate than inflation. We think it is reasonable for commodity investors to expect spot prices to continue to increase on average at roughly the rate of inflation over the secular horizon.

The second component, the roll yield return, was negative during the supercycle. Part of the reason for this was the market expected rising oil prices during this period, causing the futures curve to slope upward. Today shale output has helped improve roll yields in oil, the largest component of most commodity indexes, by anchoring future price expectations for the first time in a decade. We believe this anchoring effect has contributed to downward-sloping price curves, where the prompt prices are a premium to deferred prices to reflect near-term imbalances created by production outages (see Figure 2).

As long as Saudi Arabia maintains the ability to manage imbalances in the market and shale extraction prospects remain good, we expect the oil market roll yield to look similar to that in the 1990s, when backwardation (when prompt futures contracts are priced higher than deferred contracts) was common as the back end of oil remained anchored. These improved roll yields in oil will likely be an important source of returns to commodity investors – and yet the shift from negative to positive roll yield seems to have gone unnoticed (see Figure 3). Positive roll yields imply a commodity index investor is getting paid to purchase a diversifying asset that may also hedge against unexpected inflation. In fact, annualizing current roll yields could lead to the best roll yield contribution to returns since 2005.

In summary, we see spot commodity prices in aggregate increasing 2%–2.5% per year, in line with the current market-expected inflation. There could be additional return potential if the roll yield remains persistently positive, which we think is reasonably likely.

Investors also need to add in the potential return from collateral – the third component – to get the total return of a commodity investment via futures. While some might use Treasury bills (T-bills) to back their commodity investments, commodities can be overlaid on top of almost any portion of an investor’s fixed income portfolio, and we believe it will be important for investors to take advantage of this to help maximize future returns. Indeed, this may negate the notion of their being an “opportunity cost” to investing in commodities.

Commodities should remain attractive on a historical basis

Overall, while the supercycle may be dead, the outlook for commodity returns today seems broadly consistent with historical returns, and commodities remain an important tool for hedging inflation risk. Since 1970 – a period that includes the ending of the gold standard and severe inflationary shocks – commodities have added an average annual return of 3.59% (source: Bloomberg, PIMCO calculations) on top of the return on collateral. Investing in a commodity index, which includes the return from collateral as well, may result in returns in excess of inflation. Even with the end of the supercycle, it doesn’t seem that today the future of commodity returns looks that much different than the past.

Past performance is not a guarantee or reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Derivatives and commodity-linked derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Commodity-linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Investing in derivatives could lose more than the amount invested. The value of most bond strategies and fixed income securities are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and more volatile than securities with shorter durations; bond prices generally fall as interest rates rise.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

The Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics. There can be no guarantee that the CPI or other indexes will reflect the exact level of inflation at any given time. The Dow Jones UBS Commodity Total Return Index is an unmanaged index composed of futures contracts on 20 physical commodities. The index is designed to be a highly liquid and diversified benchmark for commodities as an asset class. Prior to May 7, 2009, this index was known as the Dow Jones AIG Commodity Total Return Index. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

© PIMCO