- We believe the recent rise in real rates and fall in inflation expectations could jeopardize the U.S. economic recovery. We also believe these are a direct result of uncertainty about the Federal Reserve’s ultimate goal.

- Low real yields accompanied by sufficient nominal growth are the necessary prescription for a still ailing economy.

Since the end of March, 10-year real yields, as measured by U.S. Treasury Inflation-Protected Securities (TIPS), have risen from deeply negative territory to around 0.1%. Real interest rates can rise for one of three reasons: The creditworthiness of a country is worsening, economic growth is improving, or inflation expectations are falling. S&P just revised its credit outlook on the U.S. government to stable from negative, so we can rule out the first reason. And while we would welcome the second reason, we believe the rise in real yields had more to do with a drop in inflation expectations. Indeed, 10-year inflation expectations, as measured by the difference between nominal and real yields, fell from 2.52% at the end of March to around 2.05% now.

We think this rise in real rates and fall in inflation expectations could jeopardize the few glimmers of strength in the U.S. economy, particularly the nascent housing recovery. We also think they are a direct result of uncertainty about the Federal Reserve’s ultimate goal.

One of the arguments of PIMCO’s “New Normal” view is that excessive debt and leverage need to be dealt with before private demand accelerates enough to generate economic growth without assistance from the monetary or fiscal authorities. Low real yields accompanied by sufficient nominal growth (though real growth would be better) are the necessary prescription for a still ailing economy.

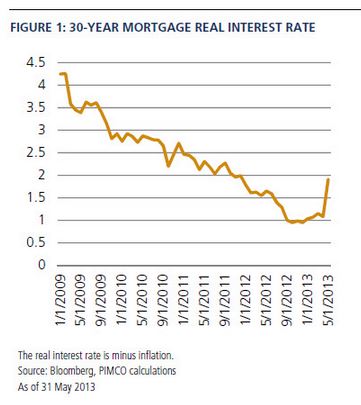

Housing prices are sensitive to real rates

One reason to be concerned about the recent rise in real yields comes from the potential impact on the housing market and its spillover. Real mortgage rates are 100 basis points higher now than they were at the end of the year (see Figure 1).

Higher house prices help the deleveraging process and boost consumption, and housing has been a job-intensive sector with large spillovers into the real economy. But house prices are very sensitive to real rates, even more than to nominal rates. House prices benefit from lower real yields and higher inflation expectations, which feed into higher rents. As a result, owning a home is more attractive if you anticipate inflation and rents to move up. Conversely, if you are worried about deflation, then it makes more sense to hang on to your cash and rent. The Fed has been trying to push investors and consumers out of cash through repressed real yields. But when real yields rise too soon, it threatens to erase the progress the housing market has made so far.

Higher inflation expectations are part of the solution, not the problem

The 2008 recession brought the U.S. economy into a liquidity trap. Excessive debt and the largest economic contraction in the country since World War II forced the Fed to push interest rates all the way to their zero lower bound. When you hit the zero bound for nominal interest rates, the only way to increase monetary accommodation by lowering real interest rates is to increase inflation expectations.

Central bankers should be eager to leave the zero bound as quickly as possible. To do so, they need to bring the nominal GDP back to where it was before the crisis. Until then, debt ratios will remain elevated and real demand will be anemic because of the ongoing deleveraging. Hitting the zero bound is costly and has happened too often because nominal interest rates and inflation expectations were too low to begin with.

At the zero nominal interest rate bound, the Fed should be asymmetric and prefer inflation to be well above target rather than below. This would help the economy escape the liquidity trap, allowing nominal rates to ultimately normalize and rise.

Consistency is key

One could easily make the case that the Fed is still expanding its balance sheet four years into the quantitative easing (QE) program because it has been reluctant to fully commit to its intention to kick-start the deleveraging process by maintaining low real interest rates and higher inflation expectations.

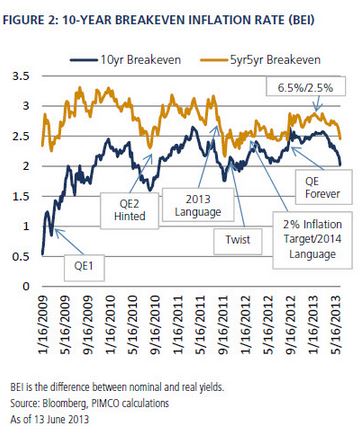

The first QE program in 2009 caused long-term inflation expectations, as measured by the 10-year breakeven inflation rate (BEI), to recover from nearly 0% to 2% (see Figure 2). Since then, the Fed has not really been consistent, and has rushed to exit QE as soon as 10-year inflation expectations reached 2.5%.

Every year since then, the Federal Open Market Committee (FOMC) has talked about exiting and reducing its balance sheet at the end of the first quarter in response to the perception of improving data and rising inflation expectations. In 2010, 2011, 2012 and now 2013, the Fed backpedaled as 10-year breakevens rose above 2.5%. There is seasonality in the economic data, in the oil market and in the flow of funds into inflation protection mandates at the beginning of every year. The Fed has been reacting hawkishly to this, pushing 10-year inflation expectations down and real interest rates up. This in turn slows the U.S. economy, forcing the Fed to ease again and increase its balance sheet even more.

To lower real interest rates and ignite animal spirits by pushing up inflation expectations, the Fed needs to “promise to be irresponsible” until the U.S. economy is well in the clear – and everyone needs to believe it. The Fed attempted this when it announced that rates would stay at zero for as long as inflation was below 2.5% and the unemployment rate was above 6.5%, and that it would continue its commitment to asset purchases. The economy then started to show some signs of improvement. But with core personal consumption expenditures (PCE, the Fed’s favorite measure of inflation) at a record low 1.1% year-over-year rate and with modest growth and employment improvements, the market did not expect the Fed to once again talk about tightening monetary policy. Despite fiscal tightening and record low inflation, it looks like stability in the housing and stock markets was enough for the Fed to start thinking about reducing accommodation.

The argument that it is the size of – and not the change in – the balance sheet that matters is seriously challenged by the recent move in both mortgage and real interest rates. It’s just arithmetic, as President Clinton once said. Less accommodation is a de-facto tightening.

The market may now be at the stage where it has started to challenge the will of the Fed to reflate the economy out of the liquidity trap. This could lead to negative consequences for the real economy, resulting in a malaise like we’ve seen in Japan.

The Fed’s dilemma

As the economy improves, the Fed has fewer incentives to maintain the promised excessive accommodation and has to fight the perception that it will pull back too soon. But to push investors out into taking more risk, the Fed’s commitment has to be credible.

When rates are already at the zero lower bound, there is no time for mistakes. Bernanke should be comfortable with high inflation expectations and very uncomfortable with dropping inflation and nominal growth. Tapering too soon, if it ends up being reversed later, could be a very costly mistake that would lead to a larger, not leaner, Fed balance sheet.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

www.pimco.com

© PIMCO

Read more commentaries by PIMCO