- We believe that given challenging prospects for attractive investment returns, the value premium could become even more important in the years ahead.

- Even in an uncertain environment like we are currently experiencing, we believe the merit in owning equities for the long term is unchanged: We want to participate as an owner in a growing, profitable business.

- By using an active manager who works to identify select opportunities wherever they may exist – and then holds those opportunities for the long term – investors have the potential to both earn attractive returns and avoid selling into volatility.

Ever since Benjamin Graham defined and began advocating value investing nine decades ago at Columbia University, investors have been searching for the value premium – that is, the additional returns that value stocks, or stocks that are perceived to be undervalued compared to their fundamentals, can potentially earn over broad equity market index1returns. Even in today’s low-yielding marketplace, we at PIMCO believe there are still stocks offering attractive value premia.

One explanation for the existence of this opportunity is that value investors generally look at companies that seemingly few others want - these beaten-down shares are not the stuff of good cocktail party chatter (the famous one word of advice imparted to a young Dustin Hoffman inThe Graduatewas not “value”). We believe the greatest opportunity is often when the most pessimism is priced into a security. After all, this is when most of the “sellers” presumably have come to market and have sold the stock down to what some may consider a bargain price.

And yet another possible explanation for the success of value investing is the willingness – indeed, even what we at PIMCO would see as the requirement – for value investors to hold their positions for a longer holding period. We believe, of course, that stock selection is critical to successful value investing, and we advocate a disciplined approach that combines a forward-looking macro outlook with rigorous bottom-up company analysis.

We aim to make the case for a long investment horizon here. But first it's worth reviewing why some people still miss the value opportunity. Princeton psychologist and Nobel Prize winner Daniel Kahneman in his wonderful book "Thinking Fast and Slow" offers systemic, convincing evidence that investors are generally hardwired to think they can outsmart the crowd – that they consistently make decisions based on "known knowns," but fail to consider the "known unknowns" or "unknown unknowns." Other explanations include the incentives of those investing on their behalf. Portfolio managers, especially those who may be less established or may have been underperforming for some time, often feel pressured to see their investment ideas work out during the course of the calendar year. Although it is impossible for anyone to foretell when, or even if, an investment will work out and perform as anticipated, these portfolio managers may not feel that they can wait for the investment to appreciate because they do not have the benefit of time on their side. It is hard to be alone and wrong. This short-term focus, somewhat driven by the performance derby, and somewhat driven by a portfolio manager’s one-year bonus incentive, is often detrimental to the returns of the manager’s portfolio.

Many studies have demonstrated that “value” can outperform over the long term. One of the most famous, “Value versus Growth: The International Evidence,” was by a pair of University of Chicago School of Business professors, Eugene Fama and Kenneth French, who showed that value outperformed "growth" stocks in 12 of 13 developed markets during a 20-year run from 1975 to 1995. The margin of outperformance was as much as 7.6% per year, the professors found – a magnitude that could have a stunning effect on how much wealth an investor accumulates over the course of a life.

Of course, the outlook for returns is not what it was, in our opinion. As Bill Gross argued in an August 2012

Investment Outlook, most asset classes should not be expected to appreciate at the same rate as they did for much of the last century.

So what does this all mean for investors? We believe that given challenging prospects for attractive investment returns, the value premium could become even more important in the years ahead.

What about now?

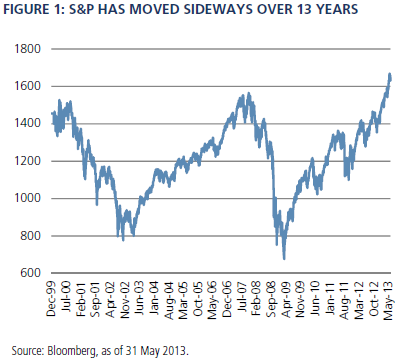

Many investors are shell-shocked by what has happened over the past 13 years in equity markets. It has been a tough period to be an equity investor. For example, one representative sample would be the S&P 500 (shown in Figure 1). Not only has this index ended up more or less unchanged over the last 13 years, but there also have been two horrible drawdowns and some shocking events during the period, including the dot com bubble collapse, the 9/11 terrorist attacks, two recessions, the financial crisis of 2008-2009, the first United States ratings downgrade ever, and ensuing deleveraging that continues to unfold. Understandably, no one wants to go through that pain again.

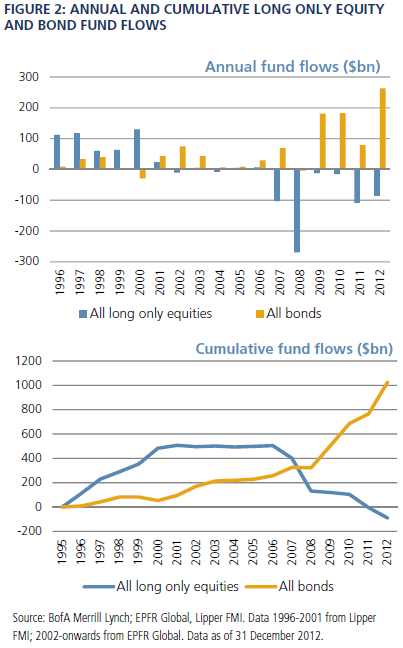

Even in an uncertain environment like we are currently experiencing, we believe the merit in owning equities for the long term is unchanged: We want to participate as an owner in a growing, profitable business. Unfortunately, some investors continue to try to time the market. Others have avoided the asset class entirely because of the pain it makes them feel. A quick scan of the charts nearby (Figure 2) shows the annual asset flows out of long-only equities and into bonds. Indeed, flows into equities have been negative now for six straight years including this year and cumulatively have been negative by $50 billion since 1996.

What to do?

Obviously we do not believe avoiding equities altogether is a good solution for most investors, especially when investing for the long-term such as funding a college education or a retirement.

Rather, by using an active manager who works to identify select opportunities wherever they may exist – and then holds those opportunities for the long term – investors have the potential to both earn attractive returns and avoid selling into volatility. But, make no mistake, part of this process is being willing to go against the crowd – often for long periods.

An additional possible benefit to this approach, is we may have less competition. We are often not competing for the same ideas with the majority because we prefer to buy temporarily out of favor companies with a longer time horizon. We may avoid paying the premium that others pay due to this lack of competition and because of the increased focus on index funds, ETFs, or funds that have low active share, or a smaller percentage of its portfolio in stocks that are different than the benchmark.

What if one is nervous about the macro events at present and wants to wait until those macro fears have subsided before investing in equities? Maybe an investor buys two-year Treasury notes right now with the intent of selling the Treasuries and buying stocks when she becomes more comfortable with the outlook. This is a form of market timing or speculation.

If an investor were to stay in t-bills (earning returns from t-bills –.06% as of April 3, 2013) vs. remaining invested in value equities (and earning value equity returns) for an extended period of time the investor faces the risk of losing out to what Albert Einstein called the most powerful force in the universe – “compound interest.” What is nearly an imperceptible difference over very short periods becomes significant as the time horizon lengthens. Going from 1% to 5%, for example, would result in additional gains of over 50% more in 10 years, and a total wealth of more than 3 times higher if one were to continue this for 30 years. So theoretically, could similar results be achieved with shorter time horizons? Possibly, but we believe the cost of the overconfidence of market timers who believe they can come back to equities when the coast is clear is potentially large and could be very damaging to their wealth.

Finally, how easy is it to define when it would be time to jump back into equities? No one rings a bell at that time. At the end of long secular bear markets few really want to invest in equities. In the late 1970s and early 1980s the popular press certainly would not have helped. At that time, we were finishing over a decade of flat prices. Inflation was high and the Cold War was still raging. We had hostages in Iran and a tough election coming. Was it obvious then to jump back into equities? We don’t think so.

Yes, stocks tend to be more volatile in a mark to market sense, but we believe that the potential of having higher terminal wealth can help compensate for this risk for pensions, endowments, and retirement allocations that have a 5 year or longer horizon. Our suggestion is to figure out what percentage you want to allocate to equities due to your personal risk profile and stay invested for the long term.

Conclusion

The demand for the perceived safety of cash or short-term government securities in the short run can come at a huge cost in the long run. Investors should demand that their long-term assets are truly being managed in their best interests. Consider investing long term because we believe it is an effective way to provide attractive risk-adjusted return potential that can help meet objectives. In the midst of a 13-year bear market for stocks, now may be a good time to consider selectively adding exposure to companies with value characteristics and investing for the long-term.

1This is in addition to the equity risk premium, which is what stocks earn above perceived “risk free” assets such as Treasury bills.

A "risk free" asset refers to an asset which in theory has a certain future return. U.S. Treasuries are typically perceived to be the "risk free" asset because they are backed by the U.S. government. All investments contain risk and may lose value.

Past performance is not a guarantee or a reliable indicator of future results. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investments in value securities involve the risk the market’s value assessment may differ from the manager and the performance of the securities may decline. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government; portfolios that invest in such securities are not guaranteed and will fluctuate in value. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

www.pimco.com

© PIMCO

Read more commentaries by PIMCO