- Determining the optimal allocation to cash is as challenging as ever in today’s unusually uncertain markets.

- When allocating to cash, investors should consider a multi-dimensional framework to assess the liquidity of the underlying cash instruments.

- In our view, the most attractive risk-adjusted opportunities for cash investors lie just outside the traditional money market space.

“What should be my portfolio’s allocation to cash?” Investors wrestle with this question, and of course, there is no clear-cut answer. Determining optimal portfolio allocations to cash requires a holistic analysis of liquidity needs and risk tolerance, as well as prevailing and future investment opportunities. Given that today’s markets remain unusually uncertain and are increasingly driven by policymakers’ decisions, finding an answer to this question is as challenging as ever. We believe understanding the multiple roles cash can play in investment portfolios and having a general framework can help investors make this important allocation decision.

Defining cash allocations and liquidity

Cash can be thought of as a store of value, a medium of exchange and a unit of account. Often, “cash equivalents” are considered current fixed income assets with maturities or durations of about one year or less that can help investors meet their needs for liquidity. However, during the financial crisis several instruments deemed by some as “cash equivalents,” such as municipal variable-rate demand notes, became highly illiquid and suffered large losses. Therefore, we believe investors should consider and differentiate the concepts of cash equivalents and liquidity.

Liquidity is a multi-dimensional concept, largely captured by four parameters:

-

Immediacy: How quickly can a position be established or exited?

-

Width: How wide is the bid/ask spread?

-

Depth: What volume can be transacted at prevailing prices?

-

Price impact: Does the market move, and for how long is the

price reset, as a result of your transaction?

These metrics are a function of other variables in the market, such as transparency, market sentiment and seasonality. Thus, the liquidity profile of various asset classes is constantly in flux. A common error in liquidity analysis is interpreting volume traded as a proxy for liquidity. Volume alone doesn’t pass the test in our multi-dimensional framework. For example, during the liquidity crisis of October 2008, the S&P 500 Index dropped precipitously while short-term funding markets froze; yet, S&P 500 Index trading volume remained robust as swarms of investors panicked to sell their equity exposures, as shown in Figure 1.

The role of cash equivalents within a multi-asset portfolio

Liquidity in the form of cash equivalent investments can serve several roles in portfolio construction. First, a liquidity profile can be established to sterilize known liabilities, such as future capital expenditures. To the extent these liabilities are known, liquidity can be “tiered” to match these liabilities so that at least a portion of the cash portfolio can be invested in short-term instruments that can potentially generate a return above bank deposits or money market funds. Second, holding cash equivalents can hedge against adverse events that trigger unforeseen liquidity needs, thereby providing defensive diversification benefits. Third, cash equivalents can serve as “dry powder” in a portfolio during periods of market overvaluation, allowing investors to both avoid the negative impact of downturns and take advantage of future opportunities. (See Figure 2.)

At first glance, these roles may seem distinct, but they are closely intertwined and self-reinforcing. The need for liquidity is often highest when correlations among assets are spiking, diversification is failing and forced deleveraging is occurring. In these situations, valuations become distorted due to forced selling and investor panic, which can be just the right time to put dry powder to work and acquire assets at discounted valuations. We therefore believe when deciding on cash allocations, investors need to consider the delicate interplay between these factors.

Cash equivalents as a diversifier

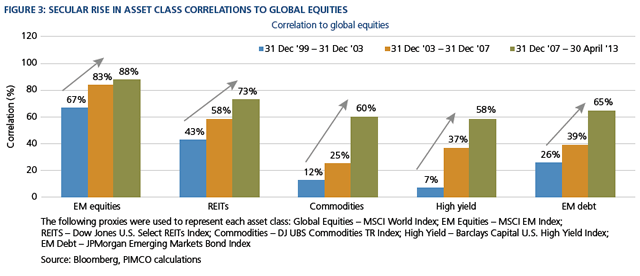

Over the past decade, an important trend has emerged and even strengthened: Correlations of most risk assets to global equities have risen steadily, as Figure 3 shows. It’s a well-known fact that during market crises, spikes in cross-correlations become more pronounced, exacerbated by risk-on, risk-off trading and high capital mobility. As a result, asset class diversification, which aims to help mitigate portfolio losses, has tended to fail exactly when needed the most.

Amid this secular rise in correlations, cash and short-term bonds are the only asset classes that havereliably delivered low to negative correlations with risk assets, especially during times of market stress. An analysis of equity and cash performance supports the “safe haven” status of cash: Since 1978,in every single month that the S&P 500 Index experienced a negative total return, an allocation to U.S. Treasury bills provided a positive total return, illustrated in Figure 4. Therefore, as a stand-alone investment, or in combination with explicit hedges against tail risk, cash equivalents can be an effective way to mitigate portfolio losses during “black swan” events.

Treasury bills aren’t the only cash-like investments that have remained robust during equity market sell-offs: Short-dated investment grade corporate bonds, often utilized in short-term bond strategies, also tend to provide attractive risk-adjusted returns and can be an effective way to pick up yield.

There is, of course, a tradeoff regarding the level of cash equivalents in a multi-asset portfolio: reduced carry. During this financially repressive period of zero interest rates and positive inflation, liquidity is indeed very dear. Still, we believe that asset allocation decisions should be made through a valuation-driven framework, by carefully assessing the prospective valuation levels of other assets and determining how far they are from fair value. If valuations of risk assets appear extremely rich, we argue it is better to hold some cash and potentially accept temporary purchasing power erosion from inflation than to hold overvalued assets and risk substantial losses in an attempt to earn a higher portfolio yield. Moreover, it’s possible for investors to preserve their portfolio carry, increase diversification and maintain a high liquidity profile within their defensive allocations by utilizing short-term bond strategies, which aim to provide higher yields than money market instruments by investing in assets with slightly longer durations or slightly higher credit risk.

Finally, cash is a very resilient asset and can withstand a wide range of economic regimes and act as an effective hedge against both inflation and deflation. In inflationary regimes, cash equivalent instruments, which have very low durations, tend to do much better than higher duration intermediate bonds as nominal yields rise. Conversely, during deflationary regimes, cash equivalents gain in real value and tend to do much better than equities, which suffer as earnings fall and the equity risk premium turns negative.

Cash to play offense

In addition to their roles as a liquidity source and a diversifier in a portfolio, cash equivalents allow investors to play offense. Cash is dry powder to deploy when attractive investment opportunities present themselves. This role is not as well understood, as it speaks to the “shadow” value of cash.

When most investors think about allocating to cash instruments, they typically consider the instruments’ yields, liquidity and risk profiles. However, cash also has a built-in call option with an infinite maturity – a “real” option of waiting – to allocate capital to any asset class. The premium associated with this option (the typical lower yield on cash instruments) varies over time, just like any other option premium; but if risk asset valuations appear high, this option can be very well priced. Also, just like any real option, precisely estimating the option’s value is difficult because it depends on the investor’s views on current valuations and future investment opportunities. A general rule of thumb is when volatility of risk assets is low, the potential for adding returns or mitigating portfolio risk through a tactical asset allocation to cash is higher, and the real option value of having some cash on hand goes up.

Figure 6 compares the levels of implied volatility, using the VIX Index, to cumulative S&P 500 Index returns, to demonstrate how investor risk appetite has a high correlation to equity returns. As levels in the VIX spike, equities tend to sell off amid heightened risk aversion. An investor would have earned superior total returns by simply allocating more to cash when the VIX was low and rebalancing to equities when the VIX was elevated rather than taking a constant passive exposure to either equities or cash. This demonstrates the “real” option of principal preservation that cash can offer.

Conclusion

Rising risk-asset correlations, rich valuations, unprecedented uncertainty and a strong dose of financial repression: What’s an investor to do? We believe a dynamic and intellectually curious approach to cash and liquidity management can offer attractive risk/return profiles on a forward-looking basis. In our view, the most attractive risk-adjusted opportunities for cash investors lie just outside the traditional money market space, where supply and regulatory constraints do not artificially alter the investment selection process. Thus, when allocating to cash, investors should consider a multi-dimensional framework, taking into account immediacy, width and depth to assess the liquidity of the underlying cash instruments. In this low-yield environment, broadening the cash investment opportunity set to include short-term bond strategies that invest in potentially higher-yielding instruments outside of the money market universe may be an optimal way for a market contrarian to express defensive views within a broader asset mix.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Money Markets are not insured or guaranteed by the FDIC or any other government agency and although they seek to preserve the value of your investment at $1.00 per share, it is possible to lose money. Equities may decline in value due to both real and perceived general market, economic and industry conditions.

The correlation of various indices or securities against one another or against inflation is based upon data over a certain time period. These correlations may vary substantially in the future or over different time periods that can result in greater volatility. The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. The Barclays Short-Term Index represents securities that have fallen out of the U.S. Government/Corporate Index because of the standard minimum one year to maturity constraint. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. The Dow Jones UBS Commodity Total Return Index is an unmanaged index composed of futures contracts on 20 physical commodities. The index is designed to be a highly liquid and diversified benchmark for commodities as an asset class. Prior to May 7, 2009, this index was known as the Dow Jones AIG Commodity Total Return Index. The Dow Jones U.S. Select Real Estate Investment Trust (REIT) IndexSM is an unmanaged index subset of the Dow Jones Americas U.S. Select Real Estate Securities (RESI) IndexSM. This index is a market capitalization weighted index of publicly traded Real Estate Investment Trusts (REITs) and only includes only REITs and REIT-like securities. The Barclays High Yield Index is an unmanaged market-weighted index including only SEC registered and 144(a) securities with fixed (non-variable) coupons. All bonds must have an outstanding principal of $100 million or greater, a remaining maturity of at least one year, a rating of below investment grade and a U.S. Dollar denomination. The JPMorgan Emerging Markets Bond Index Global is an unmanaged index which tracks the total return of U.S.-dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady Bonds, loans, Eurobonds, and local market instruments. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. The Citigroup 3-Month Treasury Bill Index is an unmanaged index representing monthly return equivalents of yield averages of the last 3 month Treasury Bill issues. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

© PIMCO