- Given the market’s newfound risk appetite for credit and less attractive valuations, we are taking advantage of global credit market liquidity in an effort to reduce our overall risk posture.

- In our selective offense approach, we continue to favor U.S. housing and housing-related areas, in addition to select investments in the energy, pipeline, specialty finance, gaming, hospitals, and airline and auto industries, given the more positive fundamental outlook for these sectors.

The global credit markets have become increasingly influenced by central banks and their massive liquidity injections. Companies have been taking advantage of low interest rates and tighter credit spreads to ramp up issuance of new corporate bonds and bank loans. Unfortunately, they’ve often used the majority of the proceeds to refinance and term out their balance sheets, not to increase hiring and capital spending. In addition, companies are starting to become more shareholder-friendly, rewarding equity holders through increased share buybacks and dividend payments.

Despite heightened new issuance, releveraging risk and lingering economic headwinds, investors have shown a continued willingness to “reach for yield.” New issue concessions are falling for corporate bonds while “covenant-lite” bank loan deals are rising. In addition, the all-in yield levels for both investment-grade corporate and high-yield bonds are approaching all-time lows. Yet, the low yield levels and cheap money available for companies, in the face of reflationary global monetary policies and massive central bank stimulus, should encourage them to issue more debt, which will likely result in deteriorating market technicals for credit investors.

Given the market’s newfound risk appetite for credit, we are taking advantage of global credit market liquidity to reduce our overall risk posture given less attractive valuations. Despite the unprecedented global central bank expansion of balance sheets, global aggregate demand remains soft in numerous countries around the world. While areas of strength remain in the global economy where we are maintaining credit exposure in companies in select sectors with stable-to-improving fundamentals, today’s market liquidity provides investors with a unique opportunity to potentially reduce credit risk in portfolios. In this global credit environment, investors should focus on playing defense and selective offense.

Defense

Global monetary policy is increasingly influencing asset prices in today’s financial markets. This is a consequence of relatively weak global aggregate demand and increasing fiscal austerity in many developed economies. Despite softer economic growth in emerging markets and below-trend economic growth in developed markets, equity and real estate prices have risen across most regions around the world.

Why are asset prices rising? First, highly expansionary global monetary policies have reduced left-tail and deflationary risks and increased some right-tail risks, in our opinion. Second, global central banks have significantly altered fixed income market technicals, or the supply and demand of bonds, by purchasing many higher-quality bonds and effectively taking them out of the market. Due to lower yields on government and other higher-quality bonds, many investors have been forced out the risk spectrum into investment-grade corporate bonds, high-yield bonds, equities and real estate. Third, lower interest rates have revalued risky assets such as stocks and real estate upward.

Rising asset prices have at least modestly increased confidence and “animal spirits” and have had a positive wealth effect on consumers in general. In the case of housing, higher prices are encouraging more rebuilding, a pick-up in hiring for new construction and an increase in sales activity due to healthy pent-up demand. With rising equity in homes, consumers may also be more inclined to do some remodeling. Also, while credit has remained tight for some homebuyers, credit availability has gradually improved, particularly for consumers interested in buying new autos, as banks and other mortgage and specialty finance companies are starting to ease lending standards in the face of improving demand and consumer confidence.

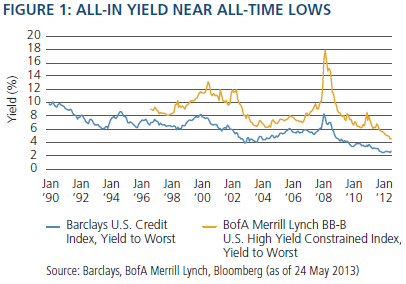

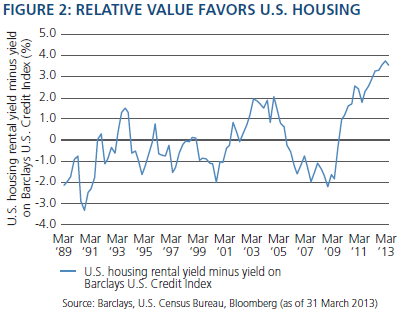

So why reduce credit risk when global monetary policy has been effective in helping to raise asset prices? Valuations! The yield levels for investment-grade corporate bonds and high-yield bonds are near all-time lows (Figure 1). In addition, the relative value of credit compared with other risk assets like real estate is less compelling (Figure 2). For investors who believe central banks like the Fed will ultimately help create a successful handoff to the private sector, the risk/reward today is arguably more attractive in select equities and real estate assets that offer the potential for positive real returns and price appreciation.

In addition to less attractive relative and absolute valuations, we believe credit investors have three main risks today: higher interest rates, wider credit spreads and deteriorating market liquidity. Investors should not underestimate higher interest rate risks over time, particularly if economic conditions improve due to increased hiring and lower unemployment, as this would lead to an eventual “tapering” of asset purchases by central banks. In the U.S., the Federal Reserve is led and heavily influenced by Fed Chairman Bernanke, who remains in a more dovish camp. Nevertheless, the U.S. economy is gradually healing and the housing market is picking up at the same time that rising equity prices are causing confidence and animal spirits to strengthen for both businesses and consumers. In addition, right-tail risks could materialize should Japan’s economy rebound or if Washington is able to move forward with much needed tax policy and fiscal reforms.

Left-tail risks should also not be ignored. If the U.S. and global economies don’t achieve “escape velocity” via an effective handoff from government-assisted, and particularly central bank-assisted, growth to the private sector, then credit spreads could widen and market liquidity deteriorate. Credit spreads are a function of default, volatility and liquidity risk. All of these risk premiums are being suppressed by central banks in the face of relatively weak global aggregate demand. While we believe near-term default risk for most global companies should remain relatively benign, many investors in the credit markets have become increasingly complacent about medium to longer-run default risk, as evidenced by the narrowing in credit spreads for longer-maturity investment-grade corporate and high-yield bonds. Default risk, volatility and the market’s liquidity tend to be highly correlated to economic growth and dependent on the continued presence and support of global central banks. Given the low risk premiums in today’s global credit markets, investors should consider a more defensive overall positioning.

Selective offense

While investors in the global credit markets should seek to reduce their overall risk profile, there are still select opportunities that we believe remain attractive due to stable-to-improving fundamentals. Credit market investors should consider focusing on companies in industries that have the potential to generate solid top-line revenue and free cash flow growth, which can be used to deleverage balance sheets to the benefit of bondholders. As we wrote in our March 2013 Global Credit Perspectives, “Finding the Sweet Spot,” investors should seek companies where the outlook for both equity and credit is favorable.

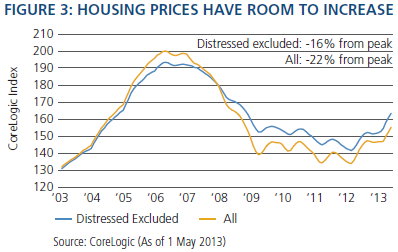

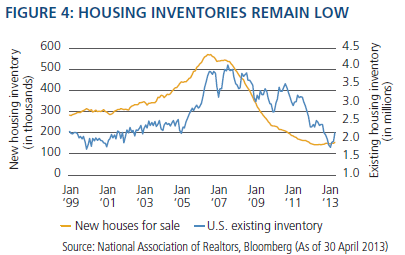

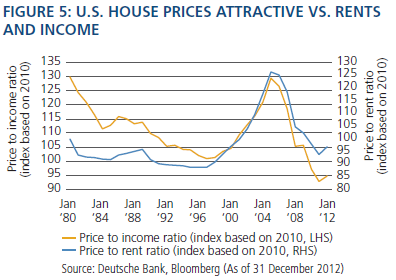

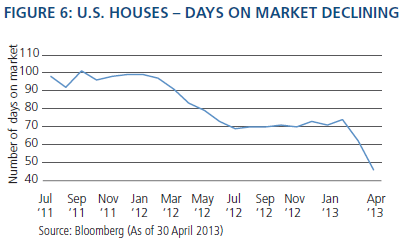

Today, one area where we continue to find select value in the credit market is U.S. housing, where the outlook for the market has brightened and continues to look attractive. Home prices have increased over the past year (Figure 3) due to pent-up demand, improved affordability and low mortgage rates. Inventories remain low (Figure 4) and as a result a pickup in housing starts is well underway, which should remain supportive for U.S. economic growth. Bank lending standards are gradually easing while the labor market is recovering. These trends are supportive for U.S. housing. Overall, we believe home prices are likely to head higher given rising demand, tight supply and the fact that housing price levels remain increasingly attractive versus both rental prices and incomes (Figure 5). As evidence, homes that are put on the market are selling considerably faster than they were even a year ago (Figure 6), which suggests confidence in the U.S. housing market is improving and animal spirits are indeed on the rise.

Investors who have a more positive outlook on U.S. housing can still seek value in the credit market today through investments in select non-agency mortgages, homebuilders, lumber and building materials, real estate investment trusts (REITs), appliance manufacturers and U.S. banks. We continue to favor U.S. housing and housing-related areas, as well as select investments in the energy, pipeline, specialty finance, gaming, hospitals, and airline and auto industries, given these sectors’ positive fundamental outlook. A selective offense approach, in the context of an overall more defensive strategy, makes sense given the risk/reward tradeoff and valuations in today’s global credit markets.

Strategies for the road ahead

Investors in the global credit markets have benefited over the years from global central banks that have increasingly gone “all in” in their use of unconventional monetary policies and balance sheet expansion. Their collective actions have suppressed both default and liquidity risk premiums. Nevertheless, valuations in the global credit markets are now approaching levels that we believe support a strategy of overall risk reduction while focusing credit exposure in select companies in areas of the world with healthy fundamentals.

The outlook for the global economy remains mixed, with many areas of the world facing soft or slowing aggregate demand and economic growth. At the same time, the pendulum in many companies’ capital structures is swinging away from bondholders and toward equity holders as management in these companies increasingly take advantage of the market’s liquidity and “cheap” money to issue debt and use the proceeds to reward equity investors.

In this environment, we favor reducing our overall credit risk in portfolios while focusing on select areas that may offer investors the prospect to invest in companies with both a solid growth outlook and management that is still acting in bondholders’ interests. In our opinion, a more conservative strategy of defense and selective offense is warranted and a necessity today.

Mark Kiesel

Managing Director

29 May 2013

Past performance is not a guarantee or a reliable indicator of future results. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, and inflation risk. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Barclays U.S. Credit Index is an unmanaged index comprised of publicly issued U.S. corporate and specified non-U.S. debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. BofA Merrill Lynch U.S. High Yield, BB-B Rated, Constrained Index tracks the performance of BB-B Rated US Dollar-denominated corporate bonds publicly issued in the US domestic market. Qualifying bonds are capitalization-weighted provided the total allocation to an individual issuer (defined by Bloomberg tickers) does not exceed 2%. Issuers that exceed the limit are reduced to 2% and the face value of each of their bonds is adjusted on a pro-rata basis. Similarly, the face value of bonds of all other issuers that fall below the 2% cap are increased on a pro-rata basis. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

© PIMCO