- Excess liquidity, falling net issuance and higher correlations among assets complicate the eventual exit that the Federal Reserve and other central banks must make from their extraordinary policies.

- The Bank of Japan’s ideology has completely changed to “tackling deflation” from “tolerating deflation.” The key focus in the coming months will be how private sectors react.

- Investors who depend chiefly upon central bank activism may put themselves at risk. They may need to hedge volatility by ensuring their investments are built more on solid fundamentals and reasonable valuations.

This month, PIMCO’s global central bank watchers discuss the longer-term implications of extraordinary policy measures by the Federal Reserve and the Bank of Japan, and the potential ramifications for central banks across the developed world.

At the gas station, when you notice you’ve got some change left over after filling up your tank, you might wonder how that can be happening at a time when the world’s central banks are printing money at an unprecedented rate. Isn’t money printing supposed to boost prices (of all kinds) and thereby help indebted nations inflate their way out of debt? Yes, but it’s not enough. Other actors on the stage must play their part; central banks can’t do it alone.

To restore growth and competitiveness, national governments must do their part. Until they do, the limitations of monetary policy will be repeatedly exposed, just as we’ve seen over the past month in the commodities markets, where a drop in the price of gold has defied beliefs that inflation would accelerate as a result of central bank activism. The whiffs of deflation remind us that it is fantasy to believe that central bankers can produce such an immaculate recovery in either aggregate demand or prices.

Three takeaways stand out from the decline in the price of gold and commodities more generally:

- Excesses are building in investments premised upon a prolonged period of central bank activism.

- The balance between the benefits, costs and risks of hyperactive monetary policies is weakening because risks to financial stability increase proportionally as central banks push investors ever outward along the risk spectrum.

- The potency of what remains of the central bankers’ medicine kit is weakening.

The underlying message is simple: Investors who depend chiefly upon central bank activism put themselves at risk. The gold market was the first market to demonstrate this and it did so in dramatic fashion, falling about 15% in just a few trading sessions in April. Investors may need to protect themselves against this sort of volatility by ensuring their investments are built more on solid fundamentals and reasonable valuations untarnished by speculative excesses created by easy money.

Into the woods

Dissatisfied with the status quo, central bankers are going ever deeper into the woods in their attempts to revive economic activity. The deeper they go, the greater the unknown perils become and the more the way out gets murkier.

Central bankers would be wise to take lessons from the book and Broadway musical

Into the Woods, which is filled with characters from famous fairy tales whose journey into the unknown has an unhappy ending. In the story, the characters do as today’s central bankers and wander ever deeper into the woods (literally), unsatisfied with the way things are, wanting more, and more, and more. One of these characters is Cinderella, who despite her great turn of fortune has grown bored with Prince Charming, so she takes to the woods in hopes of finding something more. As she along with Little Red Riding Hood, Rapunzel and Jack (of beanstalk fame) go ever deeper into the woods, they face unexpected challenges and, ultimately, tragedy.

The moral of the play carries a lesson for central bankers:

Actions have consequences.

What are the consequences the Federal Reserve must concern itself with? The Fed cites three in particular:

-

Risks to financial stability resulting from prodding investors themselves to go ever deeper into the woods when they move outward along the risk spectrum

-

Risks to market functioning resulting from the Federal

Reserve’s ever-growing securities holdings

-

A reversal of remittances by the Fed to the Treasury and possible losses on the Fed’s balance sheet

While the minutes of the March 20 policy meeting suggest the Fed is worried about these and other risks developing from its ever deeper foray into the woods, weakness in economic data of late is keeping the Fed on a path to continue further.

New York Fed President William Dudley spoke to this idea recently when he said the Fed should take with a grain of salt the better-than-expected economic news seen at the start of the year. “We’ve seen this movie before,” he said, easily mustering a reason to continue the Fed’s bond buying and promptly dismissing any menacing fallout that might lurk.

Investors are going ever deeper into the woods, too

Motivated by money printing, markets and investors have moved measurably, themselves wanting more and more from the world’s central banks. Investors who have thus far benefited from the central bankers’ deep explorations are behooved to remember the lesson of

Into the Woods:Actions have consequences.

For asset prices to stay up, they must depend on far more than the exploits of adventurous central bankers.

Be wary of any fool’s gold that is out there. Guard your capital.

Regime change at the Bank of Japan – Tadashi Kakuchi

Changes in Bank of Japan (BOJ) leadership have brought a regime shift in the BOJ’s monetary policy. Former Asian Development Bank governor Haruhiko Kuroda, who has been vocal against the BOJ on its timid easing in the past, was nominated the next BOJ governor in March and he quickly showed his strong will to tackle deflation, saying he would “do whatever it takes to end deflation” within two years.

Kuroda demonstrated his strong commitment at his first BOJ policy meeting on April 4 by announcing a revolutionary shift in monetary policy, which surpassed already high market expectations: The BOJ introduced “Quantitative and Qualitative Easing (QQE),” and surprised markets with its scale and scope. On scale, the BOJ decided to use base money for its open market operations target, replacing the overnight call rate and aiming to expand the monetary base to JPY 200 trillion at the end of 2013 and JPY 270 trillion for 2014. This target suggests a massive GDP increase of about 14% for 2013, followed by another 14% increase in 2014. In doing so, the BOJ will nearly double the size of its JGB (Japanese government bond) buying operations to about JPY 7.5 trillion per month, and will absorb as much as 70% of total issuance for 2013.

On scope, the BOJ decided to take more duration risk out of the market by purchasing longer-maturity JGBs: Expect average maturity of JGB purchases to more than double to seven years from the previous three-year average. Also look for the BOJ to increase purchases of risk assets, such as equity ETFs (exchange-traded funds) and Japan REITs (real estate investment trusts), taking a more aggressive stance in its balance sheet composition.

Along with its bold new “all-in” actions, the BOJ has also strengthened its policy commitment. Governor Kuroda made it clear they will maintain easy monetary conditions as long as is required to achieve the 2% inflation target, which reduces the risk of premature exit of easy monetary policy. He also downplayed potential costs of aggressive easing policy and only referred to its benefits. This is a dramatic U-turn from his predecessors and reinforces our view that the BOJ’s ideology has completely changed to “tackling deflation” from “tolerating deflation.”

We now know with great clarity what the BOJ wants to deliver: 2% inflation. But what are the transmission channels for its actions to result in its objectives? The BOJ expects QQE will lower risk premiums in asset prices to spur borrowing demand, and that large amounts of JGB buying under QQE will crowd out private investors from the JGB market, which in turn promotes portfolio rebalancing into riskier investments such as equities or foreign assets. In addition to these asset market channels, the BOJ also hopes its clear communication on its commitment to end deflation would increase inflation expectations in the private sector. This is a critical and necessary condition to achieve the 2% inflation target, given Japan has been trapped in a deflation equilibrium as expectations of prolonged deflation became prevalent.

Risk markets hailed the aggressive monetary easing announcement as the BOJ had hoped and envisaged. JGB markets, however, responded with heightened volatility. As the BOJ tries to crowd out private investors from the JGB market, participants tried to figure out what all of this means for equilibrium JGB yield levels, and this resulted in a rise in volatility. But thanks to BOJ’s subsequent efforts to stabilize the situation, the JGB market calmed down gradually.

The key focus in the coming months will be how private sectors react to the BOJ’s actions and stated intentions in terms of portfolio rebalancing and inflation expectations.

Into the global woods: a winner’s curse – Ben Emons

St. Louis Fed President James Bullard recently posed a question: “How far do you want to go into the woods, knowing that you are going to have to come out of the woods at some point?” This is a legitimate question given the unprecedented expansion of global central bank balance sheets. There have been several side effects of quantitative easing (QE) – both positive and negative – including negative real interest rates, higher energy prices and higher stock prices. However, another side effect is the strengthening of correlations between sovereign yields.

Correlation is a weaker form of policy coordination, but can also be a measure of how much deeper into the woods global central banks may be. The Federal Reserve has gone the furthest, with large purchases of Treasuries that have benefitted bond markets in the U.K., Japan and Germany. As the correlation with U.S. Treasuries has increased, the Fed’s QE programs promoted looser financial conditions in those countries, with the result that changes in the Fed’s balance sheet are correlated to global monetary policies. That may bring about a “winners’ curse,” as central banks overpay to get results but may end up worse off if one central bank’s success brings an unwelcome surge in yields.

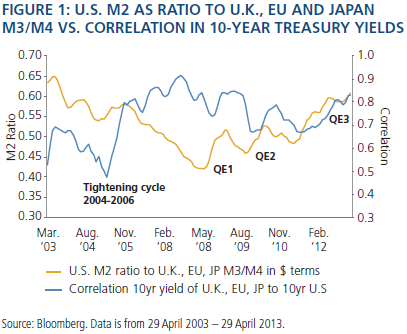

Figure 1 illustrates the degree to which policy correlation has increased when U.S. money supply, as measured by M2, has expanded relatively more than in other countries, thereby strengthening correlations between bond yields.

Central banks in the developed world each aim to end deflation, fragmentation and labor market impairment. Fed Chair Ben Bernanke recently dubbed this a “positive sum exercise.” If all central banks are deploying unconventional measures, collectively everybody is better off, he said.

Increased policy correlation challenges Bernanke’s statement by introducing a few other factors to consider. One factor is capital flows out of the eurozone, which have flowed into neighboring countries such as Sweden and Switzerland. Their foreign exchange reserves have been reinvested back into government bonds where monetary policy is active (e.g., the U.S. and the U.K.) or to where it was not needed (Germany). Higher correlation may lead to a surge in capital in these countries, lowering the base from which bond yields rise when economic conditions improve. It may also provide leeway to central banks to continue with the easing policies Bernanke has dubbed “enrich thy neighbor.”

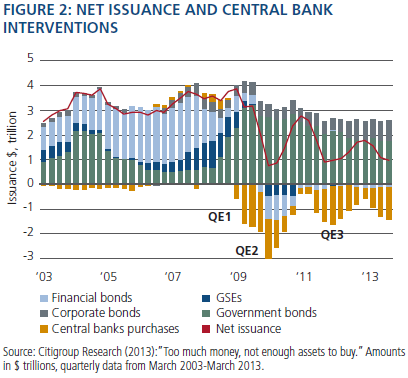

Another problem is the excess of financial liquidity relative to investable assets. In fact, there increasingly is a shortage of investable high-quality assets. Central bank purchases and low rates have facilitated a terming out of debt while also boosting mortgage prepayments and capital gains – all at a time when net issuance has been falling, as shown in Figure 2, providing a strong technical backdrop for markets.

Excess liquidity, falling net issuance, and higher correlations among assets complicate the eventual exit that central banks must make from their extraordinary policies. The deeper that central banks go into the woods, the more difficult it may be to leave. These conditions may keep bond yields low and entice leveraging by investors seeking higher expected returns. In the end, whichever central bank actually wins by virtue of marginal economic success, the victory may be cursed.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

www.pimco.com

© PIMCO

Read more commentaries by PIMCO