- In our opinion, the ECB will be most effective if it can design a programme that helps banks deleverage more quickly to stimulate growth in the real economy.

- To have a meaningful impact on Europe’s broken transmission mechanism, any ECB programme needs to not only lower the cost of credit, but also be regionally tailored or big enough to be effective.

- Long-term investors should remain focused on the quality of issuers’ balance sheets rather than simply taking more risk because of lower prospective returns.

The U.S. Federal Reserve (Fed), Bank of Japan (BoJ) and Bank of England (BoE) have all been heavily engaged in asset purchases. The European Central Bank (ECB), in comparison, looks like a shrinking violet. As of 13 May 2013, the Fed’s and BoJ’s balance sheets have grown year-to-date by 14% and 10% respectively; the ECB’s balance sheet actually fell by 14%.

How central banks use their balance sheet is also important: Asset purchases are 10% of the ECB’s balance sheet, but 97% of the Fed’s. The ECB has provided funding support but, in contrast to the Fed, has transferred much less risk from investors’ balance sheets. The result is that it has done less to help banks deleverage, improve their capital ratios and hence increase their willingness to lend.

Investors should be wary of extrapolating this status quo – Europe’s weak economic outlook means that we should expect the ECB to become more, not less, engaged. The response is likely to remain fitful, switching from “Whatever It Takes” (WIT) to conditional support. We have already seen this with the ECB’s Outright Monetary Transaction (OMT) programme which was conceived as unlimited support to tackle “convertibility risk” but has been diluted to a conditional programme as sovereign spreads have tightened.

Macro outlook suggests the ECB will need to act on the basis of “price stability”

The mid-point of the ECB’s GDP forecast, -0.5% in 2013 and +1% in 2014, is in line with consensus. And this implies that the eurozone will return to trend growth toward the end of 2014.

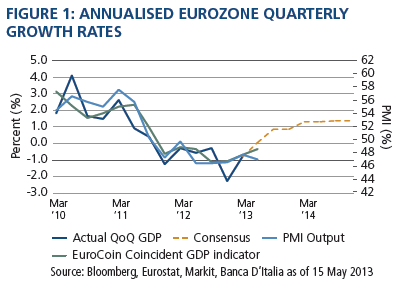

The macro data suggests that more needs to be done to boost confidence to secure the forecast economic recovery. Figure 1 shows that, despite improving financial conditions in the eurozone, Banca D’Italia’s EuroCoin estimate of GDP and the Markit Eurozone PMI survey remain consistent with recession in Q2 2013.

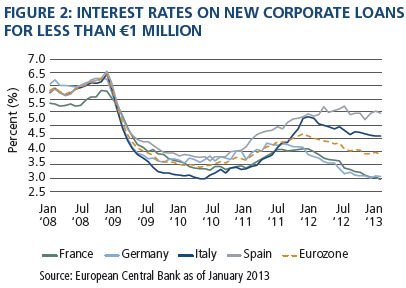

The ECB’s own assessment is that growth will strengthen as exports grow and ECB monetary policy supports eurozone domestic demand. But it is difficult to see how monetary policy can work when the transmission mechanism remains broken. Figure 2, which shows the divergence in the cost of credit for eurozone small companies, reminds us that the eurozone policy response has still not fixed the monetary transmission mechanism.

Without much needed growth, the risk that inflation under-shoots the ECB’s definition of its price stability mandate, “close to but below 2% inflation”, rises. The eurozone’s annual Consumer Price Index (CPI) fell from 1.7% to 1.2% in April 2013 (according to Eurostat). While some of this may reflect the timing of Easter, it is also worth noting that the ECB’s own forecast is for low inflation: 2014 mid-point is 1.3%.

The macro data suggests that the ECB may now start to use its balance sheet more proactively to target growth and inflation. With that in mind, what might the ECB do next?

Further rate cuts are highly likely

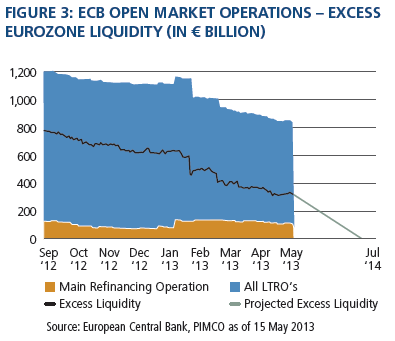

European banks have been repaying ECB long-term refinancing operation (LTRO) borrowings at a €6.5 billion weekly pace since April 2013. At this rate, excess liquidity will be below €200 billion this October 2013 (see Figure 3), a level that in the past coincided with overnight money market rates beginning to move away from the ECB’s 0% deposit rate and towards the ECB’s 0.5% main refinancing rate.

Fixing the transmission mechanism

Mr. Draghi has stated that the fragmented transmission mechanism started with the sovereign debt crisis. He has asserted that some of this fragmentation reflects issues beyond the ECB’s control, specifically the lack of bank capital. But this is a weak argument for why the ECB should not address parts of the problem that reside within its realm of influence.

First best solution: A political non-starter

As recently as March 2013, Mr. Draghi asserted that credit is expensive in Europe’s periphery because local banks “…buy [high yielding] government bonds, or lend to the private sector at a much higher rate than the yields on government bonds.” He went on to say that normally, banks in other parts of the eurozone “…would take the opportunity to either buy other countries’ government bonds themselves, so that the yields on those bonds would go down, and the domestic banks would then have more incentives to lend to the private sector… .”

The direct way for the ECB to address this problem would be to intervene and lower the relevant government bond yields. Legal arguments are probably overblown: European Union (EU) treaties have not prevented the ECB from buying government bonds. The key political constraint is that large scale ECB purchases would represent a form of eurozone debt mutualisation. Germany, as the largest and most creditworthy ECB shareholder, would likely become more engaged in under-writing peripheral credit risk elsewhere. This has implications for ECB political independence, something the Fed does not have to worry about. It is also something Germany is resistant to unless accompanied with greater controls over the conduct of peripheral fiscal policy.

Second best-solution: Lower banks’ funding costs to reduce the cost of credit

The ECB has initiated discussions with other European institutions to promote a functioning asset-backed securities (ABS) market, raising the prospect of ECB credit easing. While quantitative easing (QE) seeks to encourage more risk-taking by lowering the potential return from owning perceived “safe assets”, credit easing is an attempt to lower the cost and increase the provision of credit directly.

However, unlike the U.S., European credit is intermediated by the banking system and remains on banks’ balance sheets. Without an active securitisation market, there are few “risky” instruments that the ECB can buy.

Developing the ABS market will likely take some time. Gross public ABS issuance is running at €20 billion in 2013, down from €325 billion in 2007. Even in the “good old days”, ABS was only common in some national markets: Spain, Netherlands and UK accounted for 53% of 2007 publically distributed ABS issuance (Source: J. P. Morgan, 13 May 2013). Creating a harmonized set of ABS regulations and transparent data for different national markets will involve difficult negotiations with a variety of national and regional bodies.

We should not expect rapid progress and should not be surprised if the ECB changes tack and buys other private assets, such as banks’ loans, or allows national central banks to create national schemes. Even making it easier for banks to repo a wider variety of ABS at a lower hair-cut should help by reducing peripheral banks’ dependence on more expensive senior unsecured bond market funding.

Details matter, but a well-designed asset purchase programme could help banks deleverage

To have a meaningful impact on the broken transmission mechanism, any ECB programme needs to lower the cost of credit in the most affected economies: peripheral Europe. This could potentially be achieved by creating a programme that is regionally tailored or big enough if assets are purchased on a prorate basis.

Purchasing private assets could directly lower the cost of credit for borrowers in peripheral economies and have significant positive indirect effects. Banks could either use the proceeds from asset sales to buy other high yielding assets, such as peripheral government bonds, or reduce their reliance on wholesale financing, i.e., reduce the supply of high yielding senior bank bonds.

More importantly, purchasing private assets could help the European banking system to further deleverage. To do this, the ECB, or some other European institution, must go beyond simply providing funding support that occurs when banks repo bonds at the ECB or sell super-senior ABS tranches. Instead they must engage in some form of risk transfer. For example, if banks sold whole loans or the subordinated part of the ABS capital structure, they could reduce their risk-weighted assets and hence raise capital ratios. This could be the most powerful way to increase banks’ willingness and ability to lend.

Negative interest rates: A less effective form of QE with greater risks

Mr. Draghi has raised the possibility of cutting the ECB’s 0% deposit rate. Such action would probably push short-dated market rates into negative territory, effectively charging global investors for holding euros. Consequently, we’d expect a weaker euro, which would be stimulatory for the entire eurozone.

Negative ECB deposit rates could at the margin make peripheral assets relatively more attractive to investors. But it would be a surprise if a 0.25% penalty were enough to fix the transmission mechanism. A broken transmission mechanism implies that investors have become unresponsive to small changes in relative prices. This suggests policymakers need to do more than simply tweak relative prices further.

Negative interest rates could also have significant unintended consequences. The negative impact on the eurozone’s money market, pension, insurance and repo industries are difficult to quantify but could be potentially significant. Core country banks’ net interest margins would also be depressed by negative interest rates, although we believe a negative 25 basis points penalty would probably be manageable.

Super-long LTROs not a game changer

Given the technical difficulties of an ABS purchase program and uncertain consequences of negative interest rates, the ECB may opt for doing more of the same. A super-long, for example 5-year, repo operation, or regular 3-year LTROs, would be technically much easier to implement than asset purchases.

A more regular provision of multi-year ECB liquidity might encourage some banks to increase their leverage and seek to earn more carry from buying longer-dated and risky assets. But it would likely be difficult to sustain this given the deleveraging demands of both markets and regulators.

The recent fall in risk spreads suggest that the market’s perception of liquidity risks is currently relatively low. So it’s not clear that risk premiums would fall much if the ECB sought to lower liquidity risks further by implementing a regular multi-year ECB repo operation.

Conclusion

The technical difficulties in creating an asset purchase programme and the consequences of cutting deposit rates into negative territory suggest that designing new non-standard measures will take some time. But without a pick-up in business confidence, the likelihood of more ECB action will increase.

In our opinion, the ECB will be most effective if it can design a programme that helps banks deleverage more quickly rather than simply providing cheaper funding. Unfortunately, the political obstacles suggest that the ECB’s response will probably continue to be “too slow or not quite enough” to tackle the low growth outlook.

More unconventional ECB measures may help maintain the wedge that has developed between the valuation on risky assets and the economic growth prospects. But we believe long-term investors should remain focused on the quality of issuers’ balance sheets rather than simply taking more risk because of lower prospective returns.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, and inflation risk. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government; portfolios that invest in such securities are not guaranteed and will fluctuate in value. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

© PIMCO