- Highly expansionary global monetary policies and easier financial conditions are changing the risk and reward tradeoffs within firms’ capital structures.

- Investors should favor companies in industries that can generate solid top-line revenue and free cash flow growth. Strong earnings growth can reward equity holders, while healthy free cash flow can be used to deleverage balance sheets to the benefit of bondholders.

- We expect U.S. housing and energy, Asian and U.S. gaming, Asian gas distribution and U.S. hospital industries will continue to offer credit investors stable or improving balance sheets and solid growth. However, with shareholder activism and re-leveraging risk on the rise, we are becoming increasingly cautious on many other areas and industries.

Investors today have numerous questions about the strength of the global economy and where to invest worldwide when markets are influenced so heavily by policy developments. The U.S. economy’s private sector is picking up some momentum; however, this near-term strength is being offset by higher taxes and spending cuts in the public sector. Japan’s economy could get support from the Bank of Japan (BoJ), which appears to be moving closer to “all in” with more aggressive monetary policy. China’s outlook remains relatively positive, however, its economic outlook is increasingly dependent on policy support, while Europe still faces significant growth headwinds.

Overall, the global economic outlook is mixed, with both strengths and weaknesses. On the positive side, the U.S. private sector is slowly healing and animal spirits are improving. U.S. consumers have made some progress deleveraging and U.S. housing prices finally appear to have bottomed. Corporate profits have been solid and balance sheets are healthy.

Global central banks’ highly accommodative policies have also reduced systemic risks and helped foster easy financial conditions that have allowed many companies to refinance debt at low interest rates and extend the maturity profile of their balance sheets. The gradual pickup in the U.S. private sector, with the help of significant global central bank stimulus, has led to an improvement in risk appetite, particularly in global equity markets.

That said, the broader American economy has yet to achieve escape velocity or a sufficient handoff from the “assisted growth” to genuine private sector led growth – where businesses begin to hire workers more aggressively and invest in capital spending – and from there to the public sector, where balance sheets are stretched. Higher taxes, spending cuts and austerity measures in the U.S. and throughout many developed markets will likely constrain global economic growth. As an example, Europe will likely struggle over the next several years as weakness in its peripheral countries saps the union’s overall growth. Finally, the emerging markets’ (EM) – and especially China’s – transition from an export- and investment-led growth model to greater consumption and more balanced growth remains a secular challenge. As a result, some emerging markets economies may require more aggressive fiscal or monetary policies over a cyclical horizon to support near-term global growth.

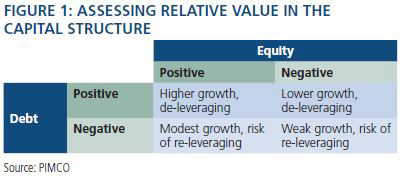

So where is the investment “sweet spot” in today’s global financial markets? The uneven global growth outlook means there are opportunities and risks for both credit and equity investors today. In addition, while highly expansionary global monetary policies have been effective at reducing systemic risks, easier financial conditions are changing the risk and reward tradeoffs in the credit and equity markets and altering value within firms’ capital structure. There are four main categories to describe the relative value in the capital structure for companies in global industries today – positive for credit and positive for equity, positive for credit and negative for equity, negative for credit and positive for equity, and negative for credit and negative for equity (see Figure 1). Let’s take a look at each.

Positive for credit / positive for equity

In our

Global Credit Perspectives November 2012 piece, “

Go for Growth,” we highlighted several sectors around the globe which were likely to experience healthy cyclical and secular growth. Many of these industries remain positive for both credit and equity today as a result of strong fundamentals. Investors should favor companies in industries that can generate solid top-line revenue and free cash flow growth. Strong earnings growth should reward equity holders, while healthy free cash flow can be used to deleverage balance sheets to the benefit of bondholders. Industries likely to see higher growth and yet still offer debt holders stable or improving balance sheets include U.S. housing and related sectors (e.g., building materials), MLPs (master limited partnerships)/pipelines, energy, gaming, Asian gas distribution and hospitals.

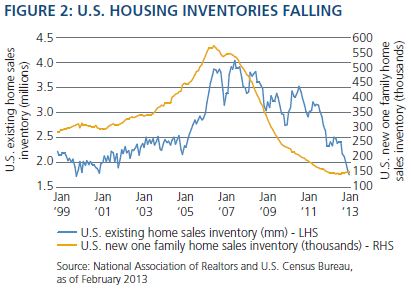

We remain constructive on the U.S. housing market and specifically on select building materials, appliance, lumber and title insurance companies. We expect the U.S. housing market will grow significantly faster than the overall economy for the next few years due to strong residential investment spending. U.S. housing inventories are now at 13-year lows for existing home inventories and near 50-year lows for new home inventories (see Figure 2). Low mortgage rates, rising rents and healthy pent-up demand are leading to a pickup in housing activity and higher housing prices across almost all regions of the U.S.

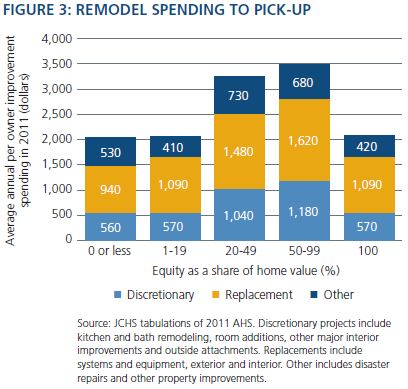

Other factors underlie this trend. A gradually improving labor market, combined with rising equities, has enhanced consumer confidence; U.S. homebuyers will likely find more credit available as banks have recapitalized and repaired their balance sheets. Companies strongly tied to the U.S. housing market should outperform over the next several quarters given the sector’s improving supply and demand outlook and its relatively cheap valuations in comparison to global markets. Building material, appliance and lumber companies all stand to benefit should U.S. housing prices rise as remodel spending should pick up (see Figure 3).

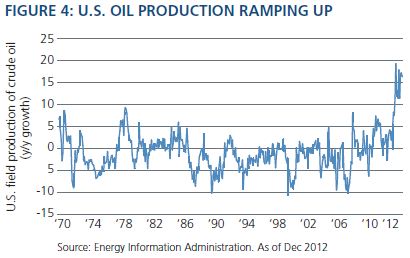

Thanks to continuing healthy growth, the MLP/pipeline and energy sectors in the U.S. remain solid industries for investment. America’s shale oil revolution (described in our

Global Credit Perspectives March 2012 piece, “

Game Changer”) is leading to a significant pickup in production of both U.S. natural gas and oil (see Figure 4). We continue to favor select MLP/pipeline and energy companies that have dominant market positions in the faster-growth U.S. shale regions.

In addition to U.S. housing and energy, we believe that the Asian and U.S. gaming, Asian gas distribution and U.S. hospital industries continue to offer solid growth and investment opportunities.

The Asian gaming sector offers access to emerging markets that are transitioning toward more consumption-based growth economies. Rising wealth and disposable income in Asia as well as significant public sector investments in infrastructure should support casinos, particularly in Macau, along with companies with exposure to Asian gaming. We also find select U.S. gaming companies attractive where management intends to use growing free cash flow to deleverage balance sheets.

Asian gas distribution is another sector we favor given its strong growth outlook as countries like China transition away from coal and toward cleaner-burning and more environmentally friendly fuels such as natural gas. In the U.S., we continue to like select hospital companies as newly enacted legislation will significantly increase healthcare coverage across the nation.

Positive for credit / negative for equity

While our preference in our global credit portfolios is to invest in higher-growth industries, and in companies with solid free cash flow, we also find value selectively in credits in lower-growth areas where management is acting in bondholder interests. For example, in Europe, where growth remains challenged, select companies in metals and mining, telecom and financials may offer solid financial flexibility, asset quality and free cash flow. In some cases, these companies have chosen to issue equity, cut dividends and sell assets in order to deleverage and improve their credit profiles and balance sheets. While negative for equity holders, this focus on repairing balance sheets makes these credits still attractive from a bondholder’s perspective.

Another area that remains attractive for bondholders is a select group of quasi-sovereigns in emerging markets and sovereigns in Europe. A few EM quasi-sovereign credits in the energy sector remain strongly supported by the sovereign: We have seen examples of large equity injections into companies where the sovereign owns a large or majority stake in the credit. We continue to invest in select EM credits where both sovereign support and fundamentals are strong. Finally, we favor some peripheral eurozone government bond markets where the combination of European Central Bank (ECB) support and fiscal reforms are improving these countries’ profiles.

Negative for credit / positive for equity

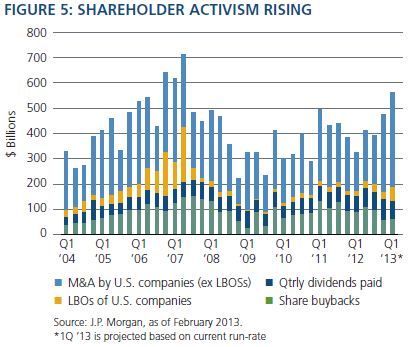

Bondholders are finally starting to wake up to the fact that easy monetary policy for an extended period can also have adverse consequences. Companies are increasingly taking advantage of low interest rates and tighter credit spreads to issue debt to re-leverage balance sheets, increase share buybacks and pay out more dividends to shareholders (see Figure 5). Investors’ strong demand for income and yield has improved both companies’ access to credit and the environment for leveraged buyouts (LBOs) and mergers and acquisitions (M&A). The rise in covenant-lite bank loan deals and pickup in new corporate bond issuance suggests some credit market participants may be becoming less disciplined. This trend has helped reignite shareholder activism and corporate animal spirits. While potentially positive for equity holders, the re-leveraging of less leveraged or underleveraged companies tends to be unfriendly for bondholders.

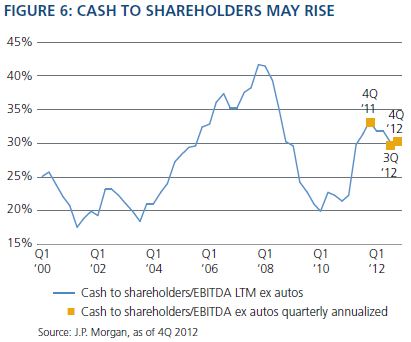

At PIMCO, we have been cautious on the credit side in industries where we see increasing risk of management re-leveraging balance sheets or paying out more cash to shareholders; these sectors include technology, consumer staples, beverages, pharmaceuticals, industrials and retail. While the overall level of non-financial cash returned to shareholders is near its 13-year average (see Figure 6), we believe market conditions indicate risks toward higher shareholder activism going forward. For this reason, we remain underweight some of these non-financial sectors in the credit markets.

Negative for credit / negative for equity

Fundamentals remain weak in many industries around the globe due to stretched public sector balance sheets and soft economic growth in numerous developed markets. We remain cautious on many companies in the defense (see Figure 7), telecom (wireline), gold mining, coal and supermarket sectors. In addition to weak growth, several of these industries face large underfunded pension obligations. Despite these headwinds, some companies are still willing to reward shareholders through increasing dividends and share buybacks. While these measures may provide temporary support for equity values, the stocks and corporate bonds in many of these companies face too many hurdles. We are avoiding most of these credits given their weak fundamental outlook.

Finding the sweet spot

Investors in the global markets face an uneven economic growth outlook, with many regions supported by aggressive policy actions. While mostly helpful for growth, highly accommodative monetary policy is now leading to a less bondholder-friendly environment in many credit sectors. With shareholder activism and re-leveraging risk on the rise, we are becoming increasingly cautious on many areas and industries in the global credit markets and are maintaining a more selective approach that harnesses our bottom-up credit expertise and global resources.

At PIMCO, portfolio managers and credit analysts are focused on finding the sweet spot – the most attractive bottom-up investments given today’s opportunities and risks that are also consistent with our top-down outlook. In our global credit portfolios, we continue to focus on regions and sectors that we feel can deliver strong growth and where bondholders may benefit from solid free cash flow to deleverage balance sheets. Regionally, our largest credit over-weights remain in the U.S. and in emerging markets given our more positive economic outlook in these areas. From a sector perspective, we favor industries and areas that have the ability to grow faster than the economies in which they operate. We remain positive on U.S. housing-related sectors, building materials, MLPs/pipelines, energy, gaming, Asia gas distribution and hospitals.

While re-leveraging risk has us more cautious overall, we believe our selective and targeted approach makes sense given the evolution of the global economy and today’s markets.

Mark Kiesel

Managing Director

March 2013

A word about risk: Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. All investments contain risk and may lose value.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

www.pimco.com

© PIMCO

Read more commentaries by PIMCO