Love, Money or Disappointment: What Will Asian Credit Investors Find in Their Red Envelopes?

- Our cyclical economic outlook for Asia in 2013 is unusually dependent on breakthroughs in structural policies.

- Although we continue to favor select opportunities in key sectors, in general Asian credit spreads are trading historically tight.

- Bottom-up research is critical, along with careful top-down views on shifting economic conditions, and investors need adequate compensation for taking credit risk. Some sectors and companies can grow significantly faster than their respective economies.

Investing in Asia’s credit sector is far from simple these days. Although we continue to favor select opportunities in key sectors, in general Asian credit spreads are trading historically tight, largely thanks to liquidity injections from major global central banks. Bottom-up research is critical, along with careful top-down views on shifting economic conditions, and investors need adequate compensation for taking credit risk.

An image that comes to mind this time of year is people in many cultures exchanging red envelopes: Lunar New Year envelopes filled with money, or valentines filled with loving sentiments. Credit investors, however, may find that not all their “red envelopes” carry cash or love, but disappointment instead, in the form of increasing default risk, corporate governance concerns and mispriced risk premia. Credit research is the key to better outcomes.

Macroeconomic outlook linked to policy developments

Our cyclical economic outlook for Asia in 2013 is unusually dependent on breakthroughs in structural policies. For example, our base case for China sees measured policy reform with the potential for moderate upside surprises resulting from China’s new leadership. Meanwhile, we expect Japan’s new government will likely focus on reflating the structurally impaired economy, although policy effectiveness remains questionable. Finally, Australia will be burdened by the policy responses of other nations, in particular the secular rebalancing of the Chinese economy away from an investment-driven model.

Structural policy breakthroughs in the U.S., Europe and China could boost investor animal spirits and prompt businesses to put their large cash stockpiles to work, which could help sustain the current rally in credit spreads. In addition, we are beginning to see a trend of assets reallocating to emerging Asia bond markets in both hard and local currency.

Regional trends support select opportunities in Asian credit

Despite the muted outlook for global economic growth, areas of the Asian credit sector offer attractive opportunities. Some sectors and companies can grow significantly faster than their respective economies. That said, not all companies will be reliable guardians of bondholders’ investments. The quality of corporate governance and accounting disclosures can also vary widely, a fact some investors in marginal companies have learned in recent months. On-the-ground credit research is therefore essential – and this is why PIMCO has doubled its resources in the region in the last two years.

To illustrate, credit from shadow banking channels provided a strong boost for Hong Kong and Chinese property developers in the second half of 2012. However, we focused only on strong, diversified developers with established track records and transparent corporate governance. And in Japan, yen strength during the second half of 2012 accompanied by secular negatives in the economic outlook, significant mergers and acquisitions (M&A) activity and increasing tensions with China allowed us to take advantage of widening spreads and invest in a range of Japanese credits at attractive entry points.

In emerging Asia, investors should consider higher-quality companies in sectors poised to benefit from increasing incomes and urbanization. In China, for example, the number of middle-income households is expected to double from 100 million to 200 million over the supersecular horizon, and the corresponding increase in consumer affluence will spur demand for energy, services, infrastructure and high-end durables. Hence credits we like in China, Korea, Indonesia and India include select companies in utilities, telecom, energy and gaming. In addition, we favor a number of banks in Japan and Korea that have strong state support and manageable funding risk. On the higher-yielding end of the spectrum, we favor exposure to Mongolia, whose mining industry is poised for robust development.

On the other hand, investors should avoid Chinese credits with high financial leverage and outdated business models designed for an investment- and export-driven domestic economy. Examples include high-cost metals producers and select industrials that are losing competitive advantage as excess domestic capacity saps profit growth and margins. The recent rally in credit spreads has encouraged several marginal, lower-rated companies to tap the U.S. dollar offshore bond markets; however, we are hesitant about these lower-rated credits based on our fundamental analysis, which projects inadequate compensation for expected loss in the event of default.

Valuations in the Asian credit sector need careful analysis. They appear fair versus U.S. credit on an absolute basis (see Figure 1), but attractive based on volatility-adjusted returns (see Figure 2). However, valuation in the new issue primary bond markets appears rich as it does not offer adequate compensation for underlying credit risk, so we have been very selective in this area.

Asian oil and gas offer attractive opportunities today

We remain positive on the major state oil companies in China, Korea, Indonesia and Malaysia, and also in the downstream segment in India. Governments are motivated to support this sector to drive and sustain economic growth. For example, as China’s economy continues to expand, it faces a rising energy deficit (note its dependence on imported oil; imports doubled in the last decade – see Figure 3) and its domestic oil and gas reserve life currently stands at 10 years compared with the OECD (Organisation for Economic Co-operation and Development) average of 35 years. Thus we expect Chinese state oil and gas companies to pursue more overseas acquisitions – and with government support. Pricing deregulation in the downstream sector, if successful, could also provide a significant boost to their financial profile. This phenomenon is not unique to China but is prevalent in other emerging Asian countries. Given the strong M&A interest from emerging Asian energy companies, we are also investing in likely acquisition targets in North America.

In India, we favor downstream refining companies, which may offer higher relative value given the greater level of dependence on and support from the government and the recent efforts to raise fuel oil prices to reduce the public subsidy burden. We have invested in several high quality state-owned energy companies in the region.

Key strengths in Japanese consumer electronics

The legacy pillars of growth for Japanese consumer electronics companies have matured as their products have become commoditized. Consequently, the greater investments in research and development and capital expenditures (capex) to develop new products have kept profitability low, especially during times of stress like the global financial crisis and the 2011 earthquake. However, many Japanese electronics companies have undertaken restructuring measures and streamlined their cost structures as a response. Also, many major companies also maintain strong product bases outside the usual audio-video, computer and camera businesses, including home appliances, infrastructure and IT solutions, and these businesses continue to be competitive and should generate stable earnings.

Over time we expect leverage to improve as operating cash flow slowly recovers, capex decelerates (due to reduced exposure to digital products that require more investment), and assets are disposed. Recent announcements of lackluster earnings and ratings downgrades have prompted spreads to widen in several electronics companies, presenting attractive investment opportunities provided the fundamentals are sound (see Figure 4).

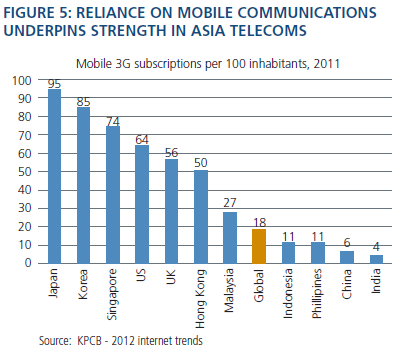

Momentum in Asia telecom

Telecom companies in Asia tend to offer strong growth momentum and solid balance sheets. Demand for cellular service is high; many Asian consumers use mobile devices as the primary means of communication. The proliferation of smartphones and demand for mobile internet (see Figure 5) adds fuel to this sector’s growth. While voice and SMS (text message) usage is declining, mobile data usage in many Asian countries is still developing and will likely be the key growth driver for the next few years. The ability to monetize opportunities in mobile data is crucial to staying ahead of competition.

Across Asia, government is a dominant player in the telecom sector. Regulations are heavy, and companies with significant government ownership often hold the great majority of market share. However, certain countries do pose more regulatory risk, whether via frequent intervention in markets or less transparent dealing in spectrum and license allocation. Our bottom-up credit analysis favors companies with greater government ownership and leadership in diversified markets .

Key investment implications

The Asian credit market continues to evolve. We expect more Asian companies to access the bond markets to refinance shorter tenor bank debt and to fund their overseas capex and M&A capital needs. This presents attractive opportunities to invest in select companies in high growth sectors. We also expect the new issue market to be quite robust in 2013 as credit spreads compress, but here investors should adhere to strict bottom-up credit analysis – or they may find only disappointment when they open those red envelopes hoping for money or love.

The authors thank Taosha Wang, Yishan Cao and Maiko Tamura for their contributions to this article.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Credit default swap (CDS) is an over-the-counter (OTC) agreement between two parties to transfer the credit exposure of fixed income securities; CDS is the most widely used credit derivative instrument. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested.

Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The Quality ratings of individual issues/issuers are provided to indicate the credit worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

The Libor Option Adjusted Spread (L OAS) measures the spread (to Libor index) over a variety of possible interest rate paths. LIBOR (London Interbank Offered Rate) is the rate banks charge each other for short-term Eurodollar loans.

The BofA Merrill Lynch Asia Investment Grade Corporate Index tracks the performance of publicly issued securities within the investment grade universe in major Asia markets. The BofA Merrill Lynch Asia High Yield Index tracks the performance of below investment grade corporate debt publicly issued in the major Asia markets. The Citigroup US Broad Investment Grade Credit Index is the credit portion of the Citigroup U.S. Broad Investment Grade (US BIG) Bond index. The Citigroup US BIG Credit index is an unmanaged index comprised of US and non-US corporate securities, US Government Guaranteed securities, and non-US sovereign and provincial securities. The Citigroup High Yield Market Index captures the performance of below investment-grade debt issued by corporations domiciled in the United States or Canada. This index includes cash-pay and deferred-interest securities. iTraxx Japan Index consists of 50 equally-weighted credit default swaps on Japanese entities. The TOPIX (Tokyo Stock Price Index) is a capitalization-weighted composite of all stocks trading on the first section of the Tokyo Stock Exchange ("TSE"), supplemented by size groups that classify first section companies as small, medium, and large and by sub-indices for each of the 33 industry groups. iTraxx Asia ex-Japan consists of 50 equally-weighted investment grade CDS index of Asian entities excluding Japan. The Markit iBoxx bond indices track investible investment grade and high yield fixed income markets. The U.S. Investment Grade CDX is an index comprised of 125 credit default swaps on individual investment grade credits. Tranches on this index are structured by order of loss from defaults among the underlying components of the index. The On-the-Run Investment Grade CDX index refers to the most recent series available at a point in time. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO