Feasting in a Time of Famine: The South African Consumer

- For all the challenges that have faced the South African economy, most listed consumer companies have enjoyed a great run since 2008.

- However, a combination of factors – strong growth in retail sales and credit along with the rise in consumer debt levels and weak employment growth – suggest the South African consumer sector may have pulled consumption forward in a way that could prove ultimately unsustainable.

- Recent labour unrest in the mining sector has many mining companies taking the opportunity to restructure and cut costs. We may have seen the end of the great profit transfer from the mining industry to the consumer.

Emerging market (EM) consumer stocks over the past five years have significantly outperformed broader EM equities (according to the MSCI EM index), attracting investors’ attention with the apparent resilience of their businesses. Since December 2007, the EM consumer staples sub-index returned 82% in U.S. dollar terms and the discretionary sub-index returned 43%, while the broad EM equity index declined by 4%. Given the current striking divergence in valuation terms between defensive and cyclical stocks in EM there has been much debate as to how long this trend can persist. In South Africa we are beginning to see the resilience of these consumer profits and their premium valuations come into question.

South Africa’s consumer sector has been on a strong run for the past several years. The combination of falling interest rates, strong consumer credit growth and rising social grants (i.e., government assistance spending) has underpinned a strong consumer environment and allowed most listed players to flourish.

However, there are signs the consumer is coming under pressure. This situation is exacerbated by recent labour unrest in the mining sector. Many mining companies are taking this as an opportunity to restructure and cut costs, and the tense situation has sharpened focus on South Africa’s anaemic employment growth. We may have seen the end of the great profit transfer from the mining industry to the consumer. As a consequence, the consumer space in South Africa risks disappointment after a period of great performance and heightened expectations. We recognise that many of these companies have been high-returning, consistent earners. However, we believe the current expectations embedded in their share prices may simply be too high. After a period of margin expansion for many consumer companies, we fear that the market no longer prices in any cyclicality to their profits, despite signs that their customers are under increasing stress. We see limited upside for many of these consumer stocks at this point.

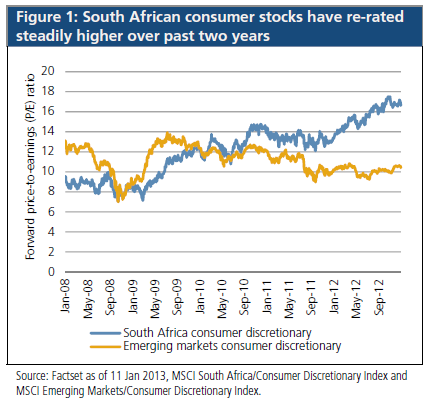

For all the challenges that have faced the South African economy, most listed consumer companies have enjoyed a great run since 2008, outpacing even the broader EM consumer universe, and their price-to-earnings (P/E) ratios have re-rated higher – see Figure 1. From the end of 2007 to the end of 2012, the FTSE/JSE African General Retailers Index returned 163% in U.S. dollars, compared with −3.8% for the MSCI Emerging Market Equity index and −2.7% for the MSCI World.

The combination of high returns on equity (ROEs) and strong sales growth has proved compelling for South African retail stocks. ROEs averaged 47% in 2012 (up from 27% a decade earlier but down slightly from 2011), while retail sales growth reached 12% in 2012 (up from 8% in 2010, the lowest point of the past decade), according to Deutsche Bank. Many of these businesses are formidable franchises and have historically been consistent earners with a good track record of returning cash to shareholders, and international investors have recognised this trend over time. Expectations have risen as well, with sales growth for South African retailers expected to be around 14% annually over the next three years, according to Bloomberg consensus.

We are seeing strong growth in retail sales and credit along with the rise in consumer debt levels and weak employment growth. In combination, these factors suggest the South African consumer sector may have pulled consumption forward in a way that could prove ultimately unsustainable.

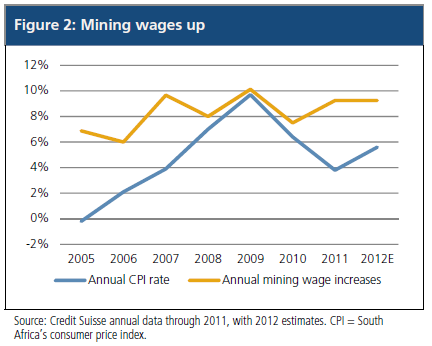

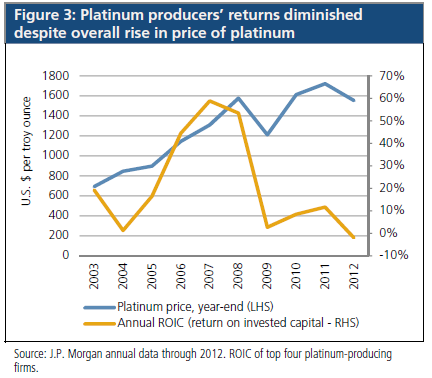

In contrast, the performance of the broader economy has been much more subdued. In mining, the impact of labour cost inflation (see Figure 2) has been exacerbated by aging reserves and challenging geology. The sector remains a significant employer, and each worker typically supports a number of dependents. Mining returns are diminished despite record-high commodity prices (see Figure 3).

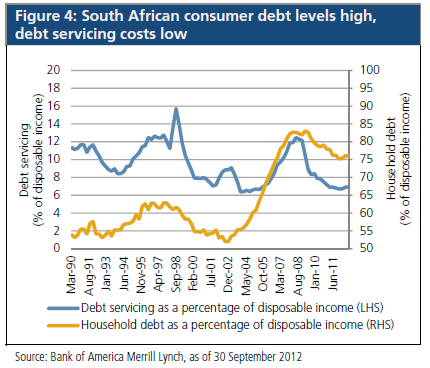

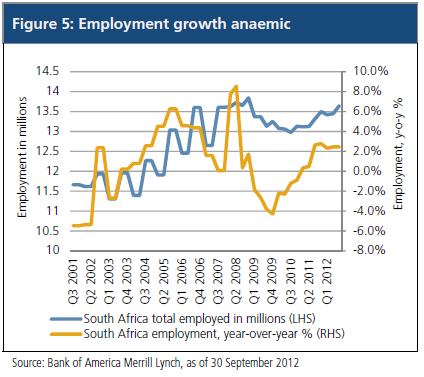

Other tailwinds for South African consumers have been accommodative monetary policy and significant social grants. Lower interest rates have allowed debt servicing levels to fall to historic lows while the ratio of debt to disposable income remains close to all-time highs (see Figure 4). And despite a period of relatively robust sales growth, employment growth has remained anaemic (see Figure 5), another factor adding uncertainty to the overall outlook.

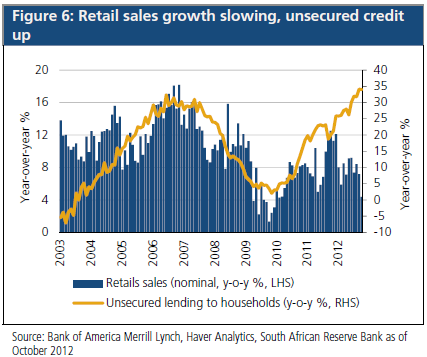

South Africa’s consumers have shown little hesitation to borrow. Though mortgage credit growth has been lacklustre, unsecured credit growth has exploded (see Figure 6). However, the percentage of delinquencies above 90 days has begun to drift up in the past few quarters to just above 12% (as of 30 September 2012, according to Deutsche Bank and the National Credit Regulator), which might suggest credit quality issues are beginning to appear – here is one more sign consumers may be overstretched.

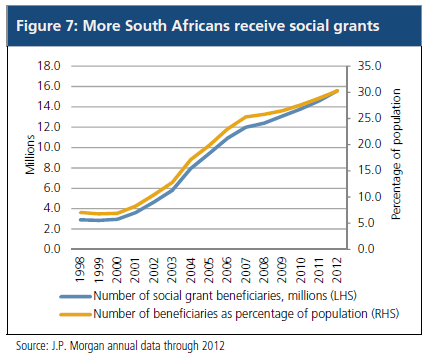

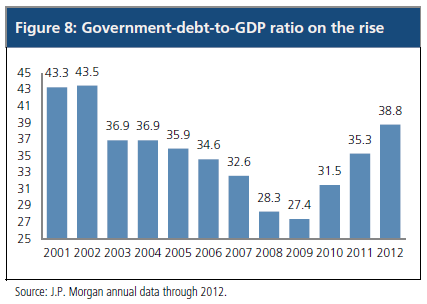

For the past decade, public spending has also buoyed South Africa’s consumer sector. Government policy has focused on social grants that now reach nearly 30% of the population (see Figure 7). One consequence has been a deterioration of the public sector balance, albeit from a strong position (see Figure 8).

In an environment of such low interest rates and a relatively benign starting public sector balance sheet, this policy mix could in theory be sustained for an extended period of time. In the end, however, we believe equity valuations and expectations are likely to be disappointed as consumers recognise their limits and begins to retrench. The early evidence from 2012 year-end holiday trading suggests we may have reached that point.

Past performance is not a guarantee or a reliable indicator of future results . All investments contain risk and may lose value. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. It is not possible to invest directly in an unmanaged index. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 24 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. The FTSE/JSE Africa General Retailers Index is a sub-index of the FTSE/JSE Africa All Shares Index, which is a market capitalization weighted index of companies that make up the top 99% of the total pre-free float market capitalization of all listed companies on the Johannesburg Stock Exchange. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO