This is the way the world ends…

Not with a bang but a whimper.

T.S. Eliot

They say that time is money.* What they don’t say is that money may be running out of time.

There may be a natural evolution to our fractionally reserved credit system which characterizes modern global finance. Much like the universe, which began with a big bang nearly 14 billion years ago, but is expanding so rapidly that scientists predict it will all end in a “big freeze” trillions of years from now, our current monetary system seems to require perpetual expansion to maintain its existence. And too, the advancing entropy in the physical universe may in fact portend a similar decline of “energy” and “heat” within the credit markets. If so, then the legitimate response of creditors, debtors and investors inextricably intertwined within it, should logically be to ask about the economic and investment implications of its ongoing transition.

But before mimicking T.S. Eliot on the way our monetary system might evolve, let me first describe the “big bang” beginning of credit markets, so that you can more closely recognize its transition. The creation of credit in our modern day fractional reserve banking system began with a deposit and the profitable expansion of that deposit via leverage. Banks and other lenders don’t always keep 100% of their deposits in the “vault” at any one time – in fact they keep very little – thus the term “fractional reserves.” That first deposit then, and the explosion outward of 10x and more of levered lending, is modern day finance’s equivalent of the big bang.

When it began is actually harder to determine than the birth of the physical universe but it certainly accelerated with the invention of central banking – the U.S. in 1913 – and with it the increased confidence that these newly licensed lenders of last resort would provide support to financial and real economies. Banking and central banks

were and

remain essential elements of a productive global economy.

But they carried within them an inherent instability that required the perpetual creation of more and more credit to stay alive. Those initial loans from that first deposit? They were made most certainly at yields close to the rate of real growth and creation of real wealth in the economy. Lenders demanded that yield because of their risk, and borrowers were speculating that the profit on their fledgling enterprises would exceed the interest expense on those loans. In many cases, they succeeded. But the economy as a whole could not logically grow faster than the real interest rates required to pay creditors, in combination with the near double-digit returns that equity holders demanded to support the initial leverage – unless – unless – it was supplied with additional credit to pay the tab. In a sense this was a “Sixteen Tons” metaphor: Another day older and deeper in debt, except few within the credit system itself understood the implications.

Economist Hyman Minsky did. With credit now expanding, the sophisticated economic model provided by Minsky was working its way towards what he called Ponzi finance. First, he claimed the system would borrow in low amounts and be relatively self-sustaining – what he termed “Hedge” finance. Then the system would gain courage, lever more into a “Speculative” finance mode which required more credit to pay back previous borrowings at maturity. Finally, the end phase of “Ponzi” finance would appear when additional credit would be required just to cover increasingly burdensome interest payments, with accelerating inflation the end result.

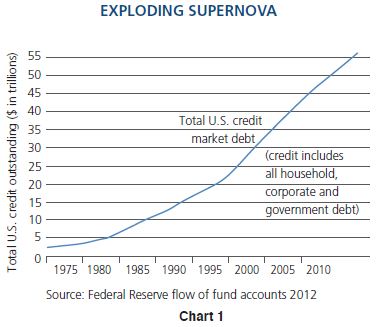

Minsky’s concept, developed nearly a half century ago shortly after the explosive decoupling of the dollar from gold in 1971, was primarily a cyclically contained model which acknowledged recession and then rejuvenation once the system’s leverage had been reduced. That was then. He perhaps could not have imagined the hyperbolic, as opposed to linear, secular rise in U.S. credit creation that has occurred since as shown in Chart 1. (Patterns for other developed economies are similar.) While there has been cyclical delevering, it has always been mild – even during the Volcker era of 1979-81. When Minsky formulated his theory in the early 70s, credit outstanding in the U.S. totaled $3 trillion.† Today, at $56 trillion and counting, it is a monster that requires perpetually increasing amounts of fuel, a supernova star that expands and expands, yet, in the process begins to consume itself.

Each additional dollar of credit seems to create less and less heat. In the 1980s, it took four dollars of new credit to generate $1 of real GDP. Over the last decade, it has taken $10, and since 2006, $20 to produce the same result. Minsky’s Ponzi finance at the 2013 stage goes more and more to creditors and market speculators and less and less to the real economy. This “Credit New Normal” is entropic much like the physical universe and the “heat” or real growth that new credit now generates becomes less and less each year: 2% real growth now instead of an historical 3.5% over the past 50 years; likely even less as the future unfolds.

Not only is more and more anemic credit created by lenders as its “sixteen tons” becomes “thirty-two,” then “sixty-four,” but in the process, today’s near zero bound interest rates cripple savers and business models previously constructed on the basis of positive real yields and wider margins for loans. Net interest margins at banks compress; liabilities at insurance companies threaten their levered equity; and underfunded pension plans require greater contributions from their corporate funders unless regulatory agencies intervene. What has followed has been a gradual erosion of

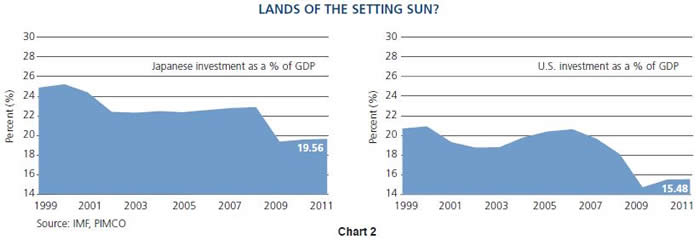

real growth as layoffs, bank branch closings and business consolidations create less of a need for labor and physical plant expansion. In effect, the initial magic of credit creation turns less magical, in some cases even destructive and begins to consume credit markets at the margin as well as portions of the real economy it has created. For readers demanding a more model-driven, historical example of the negative impact of zero based interest rates, they have only to witness the modern day example of Japan. With interest rates close to zero for the last decade or more, a sharply declining rate of investment in productive plants and equipment, shown in Chart 2, is the best evidence. A Japanese credit market supernova, exploding and then contracting onto itself. Money and credit may be losing heat and running out of time in other developed economies as well, including the U.S.

Investment Strategy

If so then the legitimate question is: how much time does money/credit have left and what are the investment consequences between now and then?

Well, first I will admit that my supernova metaphor is more instructive than literal. The end of the global monetary system is not nigh. But the entropic characterization is most illustrative. Credit is now funneled increasingly into market speculation as opposed to productive innovation. Asset price appreciation as opposed to simple yield or “carry” is now critical to maintain the system’s momentum and longevity. Investment banking, which only a decade ago promoted small business development and transition to public markets, now is dominated by leveraged speculation and the Ponzi finance Minsky once warned against.

So our credit-based financial markets and the economy it supports are levered, fragile and increasingly entropic – it is running out of energy and time. When does money run out of time?

The countdown begins when investable assets pose too much risk for too little return; when lenders desert credit markets for other alternatives such as cash or real assets.

REPEAT: THE COUNTDOWN BEGINS WHEN INVESTABLE ASSETSPOSE TOO MUCH RISK FOR TOO LITTLE RETURN.

Visible first signs for creditors would logically be 1) long-term bond yields too low relative to duration risk, 2) credit spreads too tight relative to default risk and 3) PE ratios too high relative to growth risks. Not immediately, but over time, credit is exchanged figuratively or sometimes literally for cash in a mattress or conversely for real assets (gold, diamonds) in a vault. It also may move to other credit markets denominated in alternative currencies. As it does, domestic systems delever as credit and its supernova heat is abandoned for alternative assets.

Unless central banks and credit extending private banks can generate real or at second best, nominal growth with their trillions of dollars, euros, and yen, then the risk of credit market entropy will increase.

The element of time is critical because investors and speculators that support the system may not necessarily fully participate in it for perpetuity. We ask ourselves frequently at PIMCO, what else could we do, what else could we invest in to avoid the consequences of financial repression and negative real interest rates approaching minus 2%? The choices are varied: cash to help protect against an inflationary expansion or just the opposite – long Treasuries to take advantage of a deflationary bust; real assets; emerging market equities, etc. One of our Investment Committee members swears he would buy land in New Zealand and set sail. Most of us can’t do that, nor can you. The fact is that PIMCO and almost all professional investors are in many cases index constrained, and thus duration and risk constrained. We operate in a world that is primarily credit based and as credit loses energy we and our clients should acknowledge its entropy, which means accepting lower returns on bonds, stocks, real estate and derivative strategies that likely will produce less than double-digit returns.

Still, investors cannot simply surrender to their entropic destiny. Time may be running out, but time is still money as the original saying goes. How can you make some?

(1) Position for eventual inflation: the end stage of a supernova credit explosion is likely to produce more inflation than growth, and more chances of inflation as opposed to deflation. In bonds, buy inflation protection via TIPS; shorten maturities and durations; don’t fight central banks – anticipate them by buying what they buy first; look as well for offshore sovereign bonds with positive real interest rates (Mexico, Italy, Brazil, for example).

(2) Get used to slower real growth: QEs and zero-based interest rates have negative consequences. Move money to currencies and asset markets in countries with less debt and less hyperbolic credit systems. Australia, Brazil, Mexico and Canada are candidates.

(3) Invest in global equities with stable cash flows that should provide historically lower but relatively attractive returns.

(4) Transition from financial to real assets if possible

at the margin: buy something you can sink your teeth into – gold, other commodities, anything that can’t be reproduced as fast as credit. Think of PIMCO in this transition. We hope to be

“Your Global Investment Authority.” We have a product menu to assist.

(5) Be cognizant of property rights and confiscatory policies in all governments.

(6) Appreciate the supernova characterization of our current credit system. At some point it will transition to something else.

We may be running out of time, but time will always be money.

Speed Read for Credit Supernova

1) Why is our credit market running out of heat or fuel?

a) As it expands at a rate of trillions per year, real growth in the economy has failed to respond. More credit goes to pay interest than future investment.

b) Zero-based interest rates, which are the result of QE and credit creation, have negative as well as positive effects. Historic business models may be negatively affected and investment spending may be dampened.

c) Look to the Japanese historical example.

2) What options should an investor consider?

a) Seek inflation protection in credit market assets/ shorten durations.

b) Increase real assets/commodities/stable cash flow equities at the margin.

c) Accept lower future returns in portfolio planning.

William H. Gross

Managing Director

* The terms “money” and “credit” are used interchangeably in this IO. Purists would dispute the usage and I would agree with them, arguing for the usage for simplicity’s sake and the evolving homogeneity of the two.

† Outstanding credit includes all government debt as well as corporate, household and personal debt. Does not include “shadow” debt estimated at $20-30 trillion.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing inforeign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets.Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government; portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Commoditiescontain heightened risk including market, political, regulatory and natural conditions, and may not be suitable for all investors.

The views and strategies described herein are for illustrative purposes only and may not be suitable for all investors. The information is not based on any particularized financial situation, or need, and is not intended to be, and should not be construed as investment advice or a recommendation for any specific PIMCO or other strategy, product or service. Investors should consult their financial advisor prior to making an investment decision. There is no guarantee that these investment strategies will work under all market conditions and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

www.pimco.com

© PIMCO

Read more commentaries by PIMCO