It was Milton Friedman, not Ben Bernanke, who first made reference to dropping money from helicopters in order to prevent deflation. Bernanke’s now famous “helicopter speech” in 2002, however, was no less enthusiastically supportive of the concept. In it, he boldly previewed the almost unimaginable policy solutions that would follow the black swan financial meltdown in 2008: policy rates at zero for an extended period of time; expanding the menu of assets that the Fed buys beyond Treasuries; and of course quantitative easing purchases of an almost unlimited amount should they be needed. These weren’t Bernanke innovations – nor was the term QE. Many of them had been applied by policy authorities in the late 1930s and ‘40s as well as Japan in recent years. Yet the then Fed Governor’s rather blatant support of monetary policy to come should have been a signal to investors that he would be willing to pilot a helicopter should the takeoff be necessary. “Like gold,” he said, “U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Mr. Bernanke never provided additional clarity as to what he meant by “ no cost. ” Perhaps he was referring to zero-bound interest rates, although at the time in 2002, 10-year Treasuries were at 4%. Or perhaps he knew something that American citizens, their political representatives, and almost all investors still don’t know: that quantitative easing – the purchase of Treasury and Agency mortgage obligations from the private sector – IS essentially costless in a number of ways. That might strike almost all of us as rather incredible – writing checks for free – but that in effect is what a central bank does. Yet if ordinary citizens and corporations can’t overdraft their accounts without criminal liability, how can the Fed or the European Central Bank or any central bank get away with printing “electronic money” and distributing it via helicopter flyovers in the trillions and trillions of dollars?

Investors and ordinary citizens might wonder then, why the fuss over the fiscal cliff and the increasing amount of debt/GDP that current deficits portend? Why the austerity push in the U.K., and why the possibly exaggerated concern by U.S. Republicans over spending and entitlements? If a country can issue debt, have its central bank buy it, and then return the interest, what’s to worry?

Alfred E. Neuman for President (or House Speaker!).Well ultimately government financing schemes such as today’s QE’s or England’s early 1700s South Sea Bubble end badly. At the time Sir Isaac Newton was asked about the apparent success of the government’s plan and he responded by saying that “I can calculate the movement of the stars but not the madness of men.” The madness he referred to was the rather blatant acceptance by government and its citizen investors, that they had discovered the key to perpetual prosperity: “essentially costless” debt financing. The plan’s originator, Scotsman John Law, could not have conceived of helicopters like Ben Bernanke did 300 years later, but the concept was the same: writing checks for free.

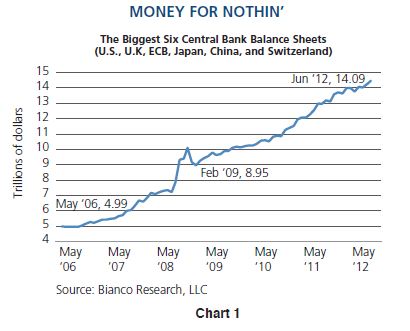

Yet the common sense of John Law – and likewise that of Ben Bernanke – must have known that only air comes for free and is “essentially costless.” The future price tag of printing six trillion dollars’ worth of checks comes in the form of inflation and devaluation of currencies either relative to each other, or to commodities in less limitless supply such as oil or gold. To date, central banks have been willing to accept that cost – nay – have even encouraged it. The Fed is now comfortable with 2.5% inflation for at least 1–2 years and the Bank of Japan seems willing to up their targeted objective to something above as opposed to below ground zero. But in the process, zero-bound yields and their QE check writing may have distorted market prices, and in the process the flow as well as the existing stock of credit. Capital vs. labor; bonds/stocks vs. cash; lenders vs. borrowers; surplus vs. deficit nations; rich vs. the poor: these are the secular anomalies and mismatches perpetuated by unlimited check writing that now threaten future stability.

Ben Bernanke has publically acknowledged these growing disparities. “We are quite aware,” he said in November 2011, “that very low interest rates, particularly for a protracted period, do have costs for a lot of people… I think the response is, though, that there is a greater good here, which is the health and recovery of the U.S. economy… I mean, ultimately, if you want to earn money on your investments, you have to invest in an economy which is growing.”

That growth now is to be measured each and every employment Friday via an unemployment rate thermostat set at 6.5%. We at PIMCO would not argue with that objective. Yet we would caution, as Bernanke himself has cautioned, that there are negative consequences and that when central banks enter the cave of quantitative easing and “essentially costless” electronic printing of money, there may be dragons.

Investment conclusions

Investors should be alert to the longterm inflationary thrust of such check writing. While they are not likely to breathe fire in 2013, the inflationary dragons lurk in the “out” years towards which long-term bond yields are measured. You should avoid them and confine your maturities and bond durations to short/intermediate targets supported by Fed policies. In addition, be aware of PIMCO’s continued concerns about the increasing ineffectiveness of quantitative easing with regards to the real economy. Zero-bound interest rates, QE maneuvering, and “essentially costless” check writing destroy financial business models and stunt investment decisions which offer increasingly lower ROIs and ROEs. Purchases of “paper” shares as opposed to investments in tangible productive investment assets become the likely preferred corporate choice. Those purchases may be initially supportive of stock prices but ultimately constraining of true wealth creation and real economic growth. At some future point, risk assets – stocks, corporate and high yield bonds – must recognize the difference. Bernanke’s dreams of economic revival, which would then lead to the day that investors can earn higher returns, may be an unattainable theoretical hope, in contrast to a future reality. Japan we are not, nor is Euroland or the U.K. – just yet. But “costless” check writing does indeed have a cost and checks cannot perpetually be written for free.

William H. Gross

Managing Director

Past performance is not a guarantee or a reliable indicator of future results. Investing in thebond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk. Equities may decline in value due to both real and perceived general market, economic and industry conditions. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2012, PIMCO.

© PIMCO