Companies are launching a number of debt deals designed to pay out a dividend to their private equity owners, at a time when buyout firms are under pressure to return money to clients.

Clayton Dubilier & Rice-backed Wolseley Group on Tuesday announced a new £350 million ($462 million) senior secured bond sale, with the proceeds to be used to finance a distribution to shareholders and refinance existing debt for the British plumbing and heating company, according to a person familiar with the matter.

It’s the latest in a series of such deals. Power equipment company Aggreko Ltd on Monday offered $2.085 billion of debt, with $323 million earmarked for a dividend distribution to owners TDR Capital and I Squared Capital.

That followed last week’s €1 billion ($1.1 billion) bond sale by German chemicals company Currenta Group, where €186 million was for a distribution to owner Macquarie Group Ltd. In the loan world, Czech pharma company Zentiva priced a €600 million term loan partly to fund a distribution to shareholder Advent International.

These sales come at a time when private equity firms are under pressure to generate earnings from their portfolio companies after an extended period of muted dealmaking. So far there’s no sign debt investors have been protesting, given the offerings coincide with a marked shift toward positive risk sentiment.

“Private equity firms need to monetize their assets. In many cases equity multiples are lower than when they acquired businesses, so a dividend recap is the best option to show you created some value,” said Nicolas Jullien, head of fixed income at Candriam SA. Such debt-for-dividend deals are known as “dividend recapitalizations” in the market.

“But it’s not without risk in a higher rate environment — you might create more zombie companies with too much debt,” he added.

Private equity executives argue that some of the businesses that are doing these dividend recapitalizations have reduced leverage in recent years and have strong balance sheets, and therefore can well afford to take on a bit of additional debt.

Spokespeople for Advent, CD&R, I Squared and Macquarie declined to comment. TDR didn’t immediately respond to a request for comment.

Receptive Conditions

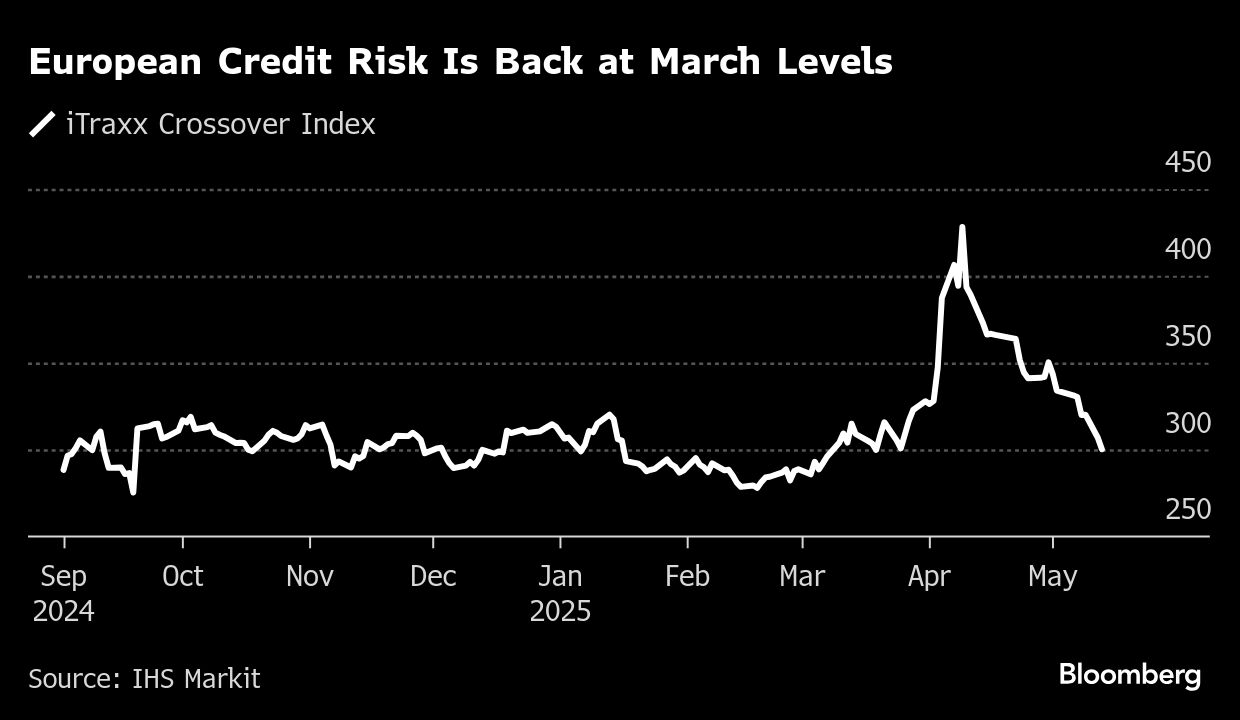

Market conditions also appear receptive given European credit risk is back to where it was prior to US President Donald Trump’s tariff shock in early April. The closely watched iTraxx Crossover index of credit default swaps dropped as low as 299.8 basis points on Tuesday, its lowest since late March.

That’s a boon for private equity firms, who are taking the longest in more than a decade to give investors their money back. The buyout industry was sitting on some $3.6 trillion of unrealized value at the end of 2024 across 29,000 unsold portfolio companies, according to Bain & Co. Distributions to investors as a share of net asset value fell to a record 11% last year, compared with an average 25%.

The issue has become particularly urgent since dealmaking, which was broadly expected to return this year, has remained highly challenging. A number of private equity-backed companies such as Stada and Golden Goose Group have had to push back plans for an initial public offering.

Permira-backed Golden Goose has told investors that it plans to set aside €100 million in cash for a potential dividend payout to its private equity owners while its IPO ambitions stay on hold. The payout is planned for some time in the 2025/2026 financial year.

There’s strong demand for more deals in the European high-yield market following the snap back from April’s lows, according to Chris Ellis, a high-yield portfolio manager at Axa Investment Management.

“Borrowers have spent a few years being quite sensible following the Covid and inflation shocks,” he said. “They have kept balance sheets in prudent order, and so do now have some scope to relever.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Abhinav Ramnarayan, Eleanor Duncan