I’m entering my 20th year of writing on investments and money. I consider myself an accidental journalist, first writing for the local business journal and, within a year, writing for major publications such as Money Magazine, The Wall Street Journal, AARP, Advisor Perspectives, and others.

I’m entering my 20th year of writing on investments and money. I consider myself an accidental journalist, first writing for the local business journal and, within a year, writing for major publications such as Money Magazine, The Wall Street Journal, AARP, Advisor Perspectives, and others.

Rather than go back and reminisce about the articles I’m most proud of, I think a better exercise is to look at those I got wrong and reflect on what might be learned. Many of my pieces are behind a paywall or even no longer online, so I’m limiting to those that can still be accessed without a fee.

A Narrower, Pricier ETF I May Buy (8/4/2021): This was about the Direxion Low Priced Stock ETF (LOPX) that bought stocks trading between $2 and $5. I noted it was similar to my fun gambling portfolio where, once a year or so, I would buy a small amount of a stock that had plunged in value and had up to a 50 percent chance of going bankrupt. I’ve had some spectacular returns – one stock over 10,000 percent – with my gambling portfolio.

I did buy a little of this fund and it promptly had large losses and was closed. Though I lost a little of my gambling money in this fund, it was an email from someone who told me they read my piece, bought the same fund, and lost money as well, that really hurt.

What did I learn? The handsome returns from my gambling portfolio were likely luck. My gambling satisfies a part of the brain that wants to have a little fun. But buying it in an ETF took away the fun, as there wasn’t the incredible volatility of an individual stock and the extreme adrenaline rush when the stock surged. So I regret this column because I took gambling into buying one specific fund. Even if it had turned out well for the fund, I shouldn’t have recommended one specific gambling fund.

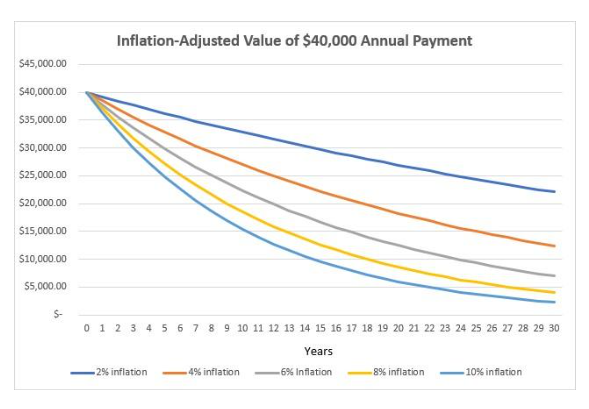

An Annuity Hater Revisits SPIAs (1/14/2019): In this piece, I concluded “A SPIA provides some longevity insurance at a reasonable rate. Even using a corporate bond comparison, the cost of longevity insurance isn’t terrible; if one assumes the proper comparison is half Treasury and half corporate bonds, the longevity insurance is free.”

While I noted the inflation risk in this piece, I regret not showing just how devastating it could be. It’s far more devastating than longevity risk. At that time, one could buy a full CPI-adjusted annuity, but the insurance industry no longer offers such a product. I think it’s because the insurance company actuaries don’t want to take this risk, though some in the insurance industry told me it was because few people were buying it.

Inflation is unknowable, and even historic inflation would eat into buying power. While counterintuitive, an SPIA with a fixed COLA has even more inflation risk than one without, as the duration of the payments is longer.

Although I’m not an annuity hater, I wish I had put the chart above in that piece. I don’t hate annuities; I just run the numbers.

What the Election Teaches Us About Investing (11/14/2012): This piece was about Nate Silver’s FiveThirtyEight.com website accurately predicting the election, calling all 50 states correctly. The analogy was in understanding the odds of an expensive portfolio besting a low-cost index fund. In the article, I actually wrote, “Silver noted that the polls as a whole would have had to be biased for Romney to prevail. His conclusion was based on statistics and probabilities, not emotions.”

Well, that was a terrible analogy to the odds of investing. Silver wasn’t so accurate in subsequent elections, and there is growing evidence that polls have been biased. The analogy falls flat as one of two candidates would win, while, after fees, the majority of active investors are all but certain to underperform passive investors with the lowest fees. While I stand by my conclusion, the argument I made to support it was flawed.

What’s Wrong in Healthcare Can Be Clearly Seen in My Colonoscopy (5/6/2006): This was about the rapid rise in healthcare, and I predicted an imminent collapse of our healthcare financing system. Fast-forward more than 18 years, and our system remains mostly unchanged, with healthcare taking up more and more of the nation’s GDP and leading the U.S. to spend far more than any other country, while having one of the shortest life expectancies of any developed country.

While the increase in costs has moderated a bit, I was completely wrong that our current financing system would collapse. Insurance companies and providers are doing just fine. We could actually pay down our national debt with the savings of getting our expenditures down to that of the second-most- expensive country (France), and that could be done in a variety of ways while preserving capitalism. My flaw was thinking logic and politics were related.

Challenging Morningstar’s Safe Withdrawal Rates (1/16/2023): In 2022, Morningstar updated its state of retirement income report and concluded that a 3.8 percent inflation-adjusted annual withdrawal rate would survive for 30 years 90 percent of the time. This was an increase from 3.3 percent in the prior year. The report was authored by three of the most brilliant minds in the industry: Christine Benz, Jeff Ptak, and John Rekenthaler.

I argued that my assumptions in a Monte Carlo simulation showed lower returns, and that expenses and emotions were not accounted for. In an email, Rekenthaler’s response to my piece was to tell me, “If I were to write a rebuttal to our work, I would raise those points as well.”

They were right and I was wrong. I failed to take into account that real interest rates had soared. A year earlier, TIPS provided a yield of negative one percent but were then approaching a positive two percent return. In fact, a 30-year TIPS ladder guaranteed a more than four percent real safe withdrawal rate.

It’s not that I think one should have too many eggs in a TIPS ladder, but I failed to connect the dots and realize that the real risk-free rate had dramatically risen, which increases the expected return of a diversified portfolio.

Conclusion

They say hindsight is 20/20, but I’m not even sure that is true. I still can’t explain why stocks gained in 2022 as COVID changed our lives. While I have regrets for these pieces and have probably forgotten a few more, I feel pretty good when comparing my wrongness to the likes of Jim Cramer (Bear Stearns is not in trouble) or Dave Ramsey (eight percent retirement withdrawal rate). And at least I own up to my mistakes.

Will I make more mistakes? Absolutely, but I hope I learn more from what I got wrong than what I got right.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Allan Roth

I’m entering my 20th year of writing on investments and money. I consider myself an accidental journalist, first writing for the local business journal and, within a year, writing for major publications such as Money Magazine, The Wall Street Journal, AARP, Advisor Perspectives, and others.

I’m entering my 20th year of writing on investments and money. I consider myself an accidental journalist, first writing for the local business journal and, within a year, writing for major publications such as Money Magazine, The Wall Street Journal, AARP, Advisor Perspectives, and others.