A quirk in retirement fund accounting is making corporate pensions look particularly flush now, giving them more incentive to cut risk by dumping equities and buying bonds.

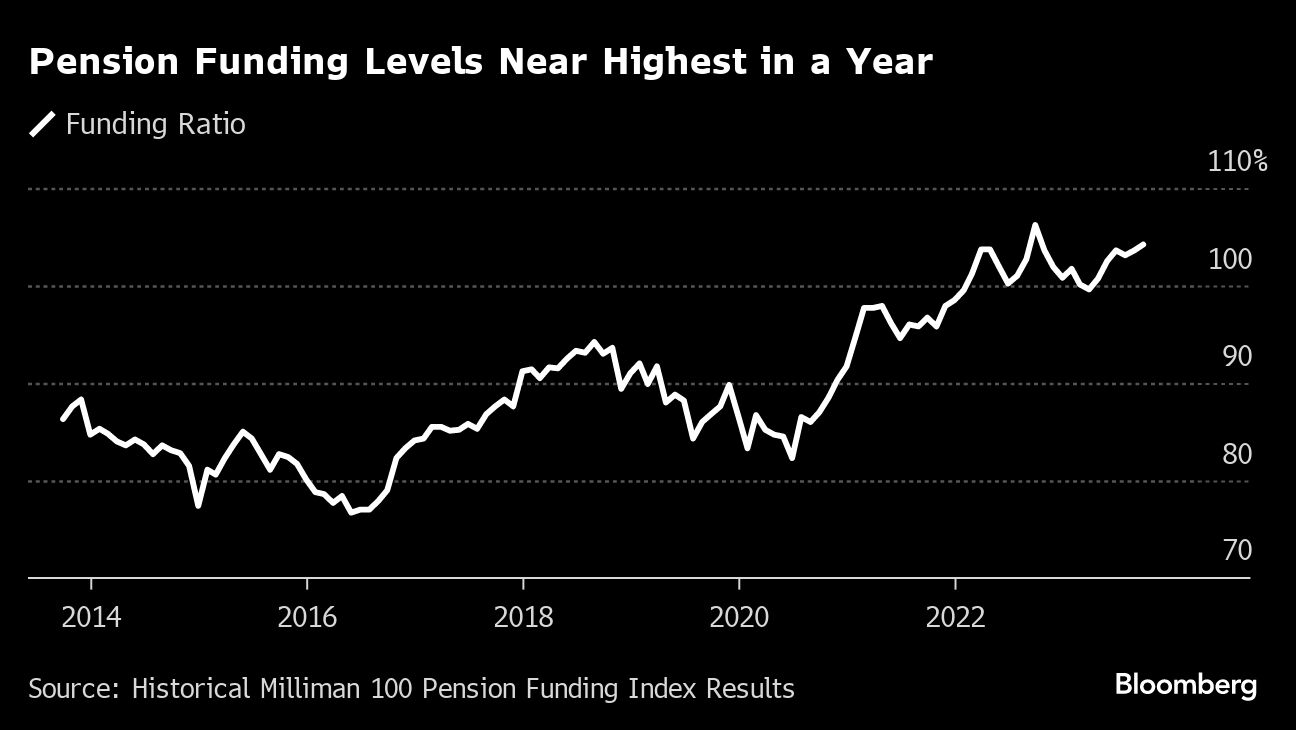

Corporate bond yields, used to value companies’ pension payouts, have jumped since early last year, effectively allowing fewer dollars now to fund future obligations. That oddity in pension accounting has helped leave retirement plans with 104.2% of the funding they need as of the end of October, data from the Milliman 100 Pension Funding Index shows.

That’s the greatest level of overfunding since October 2022 according to the index, which looks at aggregate funding ratios for the 100 biggest corporate pensions. Funding levels have been climbing for more than a decade, helped by a surging stock market.

The surplus could further boost bond buying, according to JPMorgan Chase & Co. Fully funded pensions often sell equities and buy bonds, particularly corporate notes, to lock in higher yields that can cover future obligations.

“Pension plans are taking advantage of the highest yields in many, many years, which is logical and what they should do and they’re doing it,” said Eric Beinstein, JPMorgan’s head of US high grade credit research and strategy, in an interview. “Not only does the fixed-income yield look attractive, but equity volatility is also a lot higher now. So, you’re not incentivized to hang on another year, thinking maybe stocks will be up.”

Since March 2022, the 100 US public companies sponsoring the largest plans have enjoyed surplus or near-surplus funding levels overall, Milliman’s analysis through October 31 shows. Retirement plans were underfunded for much of the decade or so following the 2008 financial crisis, but that trend reversed after the central bank started raising rates.

“By and large, it is an industry that moves slowly,” said Matt McDaniel, who leads US pension strategy and solutions at consulting firm Mercer. “There probably should be a little bit more urgency. There is one of the ironies of pension risk, is that the better funded you get, the higher your risk is because you have more to lose.”

Traditional yield buyers, namely pension funds and insurance companies, were net buyers of corporate debt through the first half of the year and make up about 30% of total US corporate bond ownership, according to Morgan Stanley.

“While we don’t have real-time data to track these flows, anecdotally demand has accelerated further in 3Q so far, especially in September,” strategists including Vishwas Patkar wrote in an October note. “There is significant room to grow, especially if complete duration hedging is the ultimate goal.”

The strategists expect yield buyer demand to stay robust, though they say “some normalizing of rates volatility is needed.”

The demand comes as US investment-grade debt issuance has shrunk — helping tighten spreads on corporate debt.

“We are under-supplied in the product that liability-driven investors want to own the most and that is long duration,” said Maureen O’Connor, global head of high-grade debt syndicate at Wells Fargo & Co. “A lot of that has to do with pensions rotating from equities to fixed-income.”

Insurers and pensions are known as liability-driven investors as their strategies involve funding future liabilities. Their investments, such as equity or debt, are determined by their obligations.

The average spread on US corporate bonds stood at 113 basis points on Tuesday — 11 basis points tighter than the average of 124 basis points seen over the last decade, even after more than a year-and-a-half of monetary tightening, which has raised recessionary risks.

Long-Duration Bet

Across most multi-tranche high-grade deals this year, the longer-dated tranches have been the most oversubscribed, and new issue concessions are now tightest at the long-end of the curve, according to O’Connor. That shows liability-driven investors are willing to buy at very close to fair value, she said.

“The liability-driven investors’ bid for duration and the absence of supply has been topical almost all year,” she said. “And it’s definitely going to continue to be, going forward.”

Still, that doesn’t mean the tightening is “logical,” JPMorgan strategists led by Beinstein pointed out in a September report. There’s a lot of time between 10 and 30 years for credit risk to deteriorate, which risk premiums ought to provide compensation for, but instead they’ve fallen to the low end of the historical range, they noted.

Bingeing on Bonds

Pensions usually see the present value of their liabilities drop as rates climb. By the end of October, pension liabilities had fallen to about $1.179 trillion, from $1.685 trillion at the end of February 2022, just before the Fed started hiking, Milliman’s data shows.

“I’m not an economist, and I don’t think anybody can forecast interest rates, but it’s hard to believe that interest rates would be significantly higher than they are right now,” said Zorast Wadia, principal and consulting actuary at Milliman. When rates eventually come down, “pensions are going to see a rise in their liabilities unless they’re locked in.”

Last month, 10- and 30-year Treasury yields started crossing above 5% before retreating, further incentivizing pension plans to double down on fixed-income investments. Higher bond yields have also boosted the percentage that retirees can withdraw annually from personal savings over 30 years, with a strong chance of not running out of money, according to Morningstar’s annual retirement income report out last week.

“We are seeing plan sponsors — a lot of plan sponsors actually — set explicit investment strategies that say, ‘When I hit a trigger point of 95% funded or 100% funded, I’m going to take X number of assets from the equity portfolio and move it to the fixed-income portfolio’,” said Mercer’s McDaniel.

“Those that don’t have those formal-type strategies are still having the same conversations and saying, ‘Hey, if I took 60% equity risk when I was 80% funded and now I’m 105% funded, it probably makes sense to be taking a little bit less today’,” he added. “So, we’re definitely seeing plan sponsors making those moves.”

Meanwhile, US equity markets have been rattled this year by war in the Middle East and concerns around the strength of US consumers, giving pension fund managers another reason to move into safer assets like bonds.

“We’re always out talking to our clients and those that we work with saying, ‘Look, we’ve seen this story before where funded status looks great and it falls down’,” said McDaniel. “‘Let’s make sure once you get to those periods where funded status is in a good spot, you’re doing something to protect yourself’.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.