Hoisington Investment Management Co. was pummeled by its bullish stance on US bonds in recent years, driving its Treasury fund to some of the industry’s biggest losses as the Federal Reserve’s rate hikes sent prices tumbling.

But long-time chief economist Lacy Hunt sees the recent retreat in Treasury yields as the start of a rally that will gain steam once the US economy careens into a hard landing.

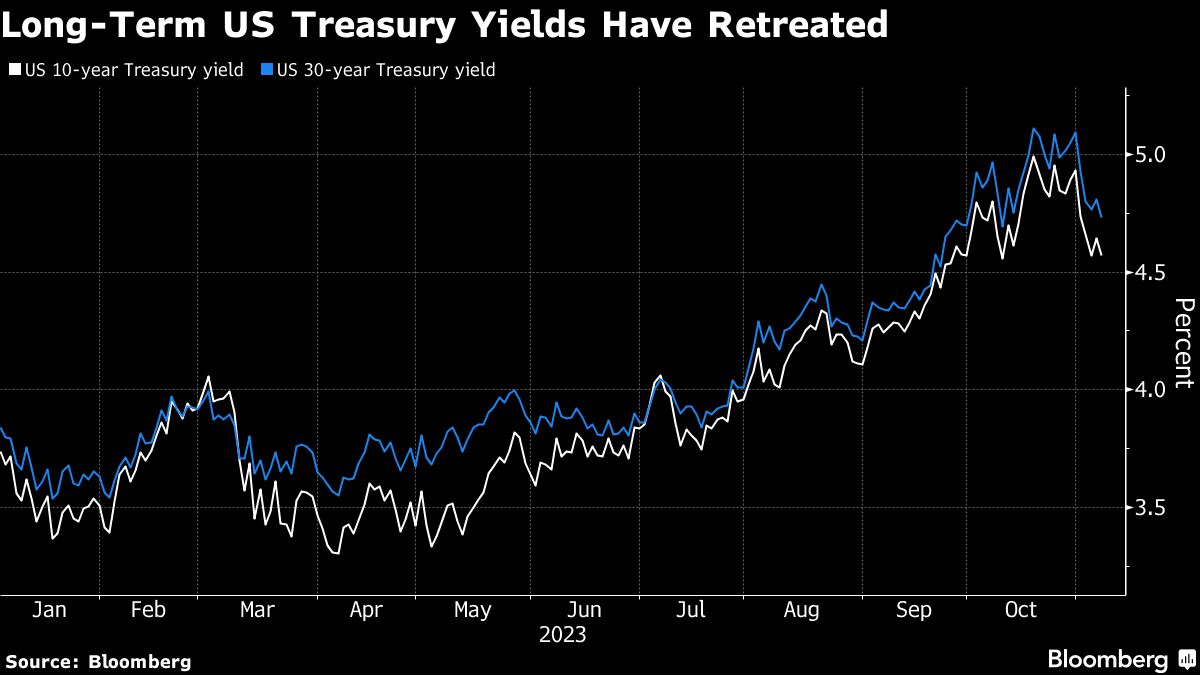

Long-term Treasury yields have slid sharply since late October on speculation that the Fed has completed its most aggressive tightening cycle in decades and the wave of new debt supply is abating. The benchmark 10-year yield has been hovering around 4.6% — well below the 16-year high of 5.02% reached on Oct. 23. That’s raised hopes that Treasuries might even eke out a small positive return in 2023 after two straight years of losses.

The Wasatch-Hoisington U.S. Treasury Fund is down about 12.7% this year and tumbled 34% in 2022, data compiled by Bloomberg show. That’s put it dead last among the funds tracked by Bloomberg in each of the past three years.

Despite that rough run, Hunt sees a fiscal and monetary backdrop that bodes well for bonds, anticipating that rates will move lower into next year and beyond.

For the bond market, “the cloud is breaking because the economy is heading into a hard landing,” Hunt said in an interview with Manus Cranny on Bloomberg Television. “But it’s a process that will take time. The US economy has very serious difficulties” that will “be with us for a long time in the future.”

Those expecting a bond recovery gained support last week when the US central bank left its benchmark rate unchanged and signaled in a post-meeting statement that the overall rise in longer-term Treasury yields had reduced the impetus to hike again.

“What we are going to see – we are beginning to see it now – is the yield curve will normalize,” the 81-year-old Hunt said. “Short yields will drop more rapidly than the long yields, but the greatest capital gains opportunities will be in the longer end of the curve.”

The curve has already gone through a major steepening move after long bond yields drew closer to those on short-term debt, though it remains inverted. Ten-year Treasury yields are about 35 basis points below those on two-year debt, though that gap exceeded 100 basis points as recently as July.

Hoisington was founded in 1980 by Van Hoisington, with Hunt helping guide investments since 1996. Hunt began his career in 1969 as an economist at the Dallas Fed.

While the runaway inflation that followed the pandemic and the massive fiscal and monetary policy stimulus it brought has been fixed, the large US national debt will weigh down growth for years to come, Hunt said. Over indebtedness is a problem, as well as other forces, like an aging population, that plagued the US before the pandemic and have only gotten worse since, he added.

“The problem for the US and the rest of the world is that there’s going to be very poor growth, very erratic growth,” he said. “But the inflationary problem in my view for all practical purposes has already been solved.”

While Hunt wouldn’t give a specific level for how low he expects yields to fall, he pointed to the firm’s 18-year duration as a sign of their conviction in the positive outlook for Treasuries. Duration is a measure of a bond portfolio’s sensitivity to changes in yield, and a longer position reflects a more bullish view.

“The 18-year duration speaks for itself,” he said. “When economic conditions weaken investors will see there is great advantage to holding the long duration Treasuries.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liz Capo McCormick, Manus Cranny