Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is part three of a five-part series that develops an analytical framework for long-term, retirement-oriented investing. You can read part 1 here, part 2 here, part 3 here, and part 4 here. The author would like to thank Joe Tomlinson and Michael Finke for their helpful comments on this article series.

Introduction

In Part 4 of this series, I discussed a method of applying the long-run, risk-return insights from earlier in the series to a goals-based approach to retirement investing. This final article considers how to extend the process into the pre-retirement years.

Aside from the obvious difference that cash flows from retirement portfolios are not yet required, two additional factors typically exist in the pre-retirement years:

“Human capital”

Human capital can be defined as the present value of someone’s future career earnings. But since the majority of most people’s earnings are used for pre-retirement spending, a more useful definition for retirement planning is a net human capital measure constituting the present value of all future retirement savings.

Greater uncertainty in the retirement plan

The further from retirement, the less certain the retirement plan. This translates to the need for flexibility in the retirement investment strategy. On the plus side, it can also translate into “optionality” in the form of greater freedom to make course corrections as necessary.

The need for flexibility implies a benefit to maintaining liquidity pre-retirement, even if it’s just the “technical liquidity” (per Wade Pfau’s terminology) of assets that are dedicated to a specific goal but can be reallocated if plans change.

Human capital

Part 3 of this series demonstrated that for a long-run goal such as retirement investing, the low-risk investment is a long-term bond. For a young person, human capital typically looks very much like a long-term bond,1 and it can play the role of the low-risk asset. Moreover, the further someone is from retirement, the greater that bond will be; and for most people, the further they are from retirement, the smaller their financial asset base (i.e., their investment capital).

Consequently, the consideration of human capital introduces a sensible case for an individualized investment glidepath. Often this can start at a very high level of risk assets (e.g., stocks) early in one’s career, when relatively low-risk human capital predominates, then glide into a portfolio with a risk capacity-appropriate asset mix late-career, when human capital is nearly exhausted.

For example, suppose someone is 35 years old, has $100,000 in retirement savings, can expect to contribute $50,000 plus inflation per year to investment accounts for retirement,2 and is aiming at an age-65 retirement. The homegrown tool we use at my firm to calculate real income can also be used to estimate that this individual’s present value of future savings is nearly $1.2 million. Financial capital and human capital comprise about 8% and 92% of total retirement capital, respectively. For anyone with even a small amount of risk capacity/tolerance, this implies that even 100% portfolio exposure to stocks likely undershoots theoretically optimal risk exposure,3 given the magnitude of the long-term bond-like human capital element.

Admittedly, there is a problem here. Young investors’ retirement-income liabilities are of higher duration than their human-capital assets. In fact, every withdrawal cash flow in retirement usually comes later than every deposit cash flow in their careers. This relates to the observation in a footnote in Part 3 that a decline in interest rates is bad for most bond investors, contrary to the popular, short-term view. Since U.S. Treasurys don’t exist at ultra-long maturities anyway, there is little that can be done about this problem early in one’s career, though optionality (to save more than planned or retire later if necessary) can attenuate this issue. And since the optimal portfolio might theoretically involve levered exposure to risk assets, taking anything away from a 100% stock portfolio is likely suboptimal.

But as the investor ages, financial capital grows and human capital shrinks. At the same time, available long-term bonds become a closer match to retirement income needs. Consequently, just as it becomes optimal for investors to hold long-term bond exposure matching the duration of projected retirement income liabilities, it becomes possible for them to do so.

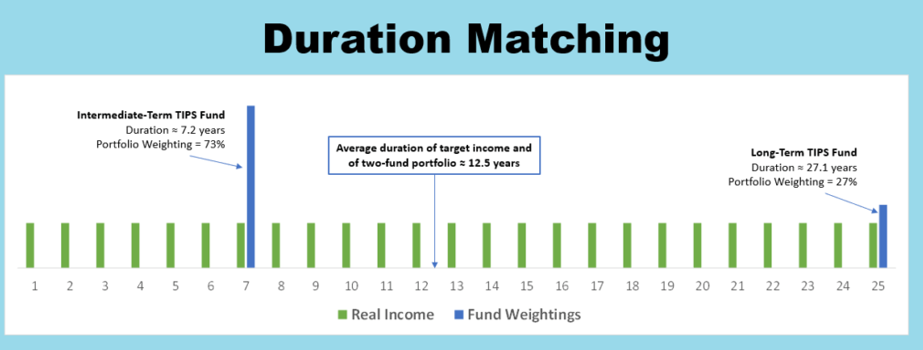

Duration matching, a technique mentioned in the last article and described in my article on TIPS ladders, is especially helpful in this context. The idea is that the weighted average of a long-term and an intermediate-term TIPS fund, targeting the same real duration as the desired series of inflation-adjusted cash flows, can provide an imperfect but quite good facsimile of the variance in the present value of those cash flows.

When the target cash flows are all in the future, the later years may still be beyond the maximum TIPS maturity. For example, someone planning to retire in 10 years and then commence 25 years of real income per the image above would have income in years 31-45, but no bonds are available at those maturities. But that investor’s overall target duration is about 22 years.4 and that duration can be matched by a two-fund portfolio heavily weighted to the long-term fund.

Moreover, as time elapses, the target duration will decrease, the amount of capital available for deployment will typically grow, and plans will change and become more concrete. With a duration-matched, pre-retirement portfolio, just two trades are required to match all such changes, versus potentially dozens with a true bond ladder. I will typically switch to a TIPS ladder when a client is ready to “lock in” real income at or near retirement. And because this process glides into TIPS exposure, it arguably smooths out the timing risk inherent to the alternative of making a large one-time switch from other assets to TIPS at whatever prevailing real interest rates happen to be at the time.5

The foregoing discussion focused entirely on the capture of “required/inflexible” income with TIPS. But because Social Security often captures most of that goal, the total return-based “flexible” income portfolio is often much larger. Yet the same theory still applies. Early in one’s career, the long-run human capital asset is a sensible complement to a stock-heavy investment portfolio. As retirement approaches, this portfolio can glide instead into a more traditional 80/20, 60/40, etc. stock/bond portfolio, where more traditional short/intermediate-term bonds can be appropriate due to the employment of flexible withdrawal rules that adapt the liability to the asset base, as also described in Part 4 of this series.6

For a growth goal (e.g., legacy), a static 100% equity position may be appropriate. But it is typically the case that retirement investing is laser-focused on building toward retirement income in the early years of one’s career, and only branches into solving for additional goals when retirement gets nearer.

Meet the new theory, same as the old theory?

Close observers will have noticed that the above construct resembles a glidepath born of “time diversification” arguments to the effect that stock risk disappears over long horizons – the very thing this series disputed in Part 2. Has all this effort resulted in the same substance with slightly different packaging?

To an obviously rhetorical question, the answer is always “no.” Here are a few examples of differences:

This is a multi-glidepath approach, where at least one glidepath slides into horizon-matched TIPS rather than cash or short-term bonds, for reasons discussed in Parts 2 and 3.

Paradoxically, this goals-based approach can provide a solid rationale for higher equity exposure in the early years than is typically seen in a traditional glidepath. In the later years, a glidepath for inflexible expenses has a much lower risk asset exposure, and none in retirement.

Another counterexample would be someone with a large financial asset base – a large inheritance, for example – even at a young age. In that event, financial capital may already be a substantial percentage of total capital. Considerations of risk capacity/tolerance may indicate a significant allocation to long-term bonds – the long-horizon low-risk asset – whereas the traditional theory would claim the long horizon in and of itself suggests a stock-heavy portfolio is appropriate and would typically buy shorter-term bonds for a “low risk” complement, contra our findings in Part 3.

Illustrating a multi-glidepath solution

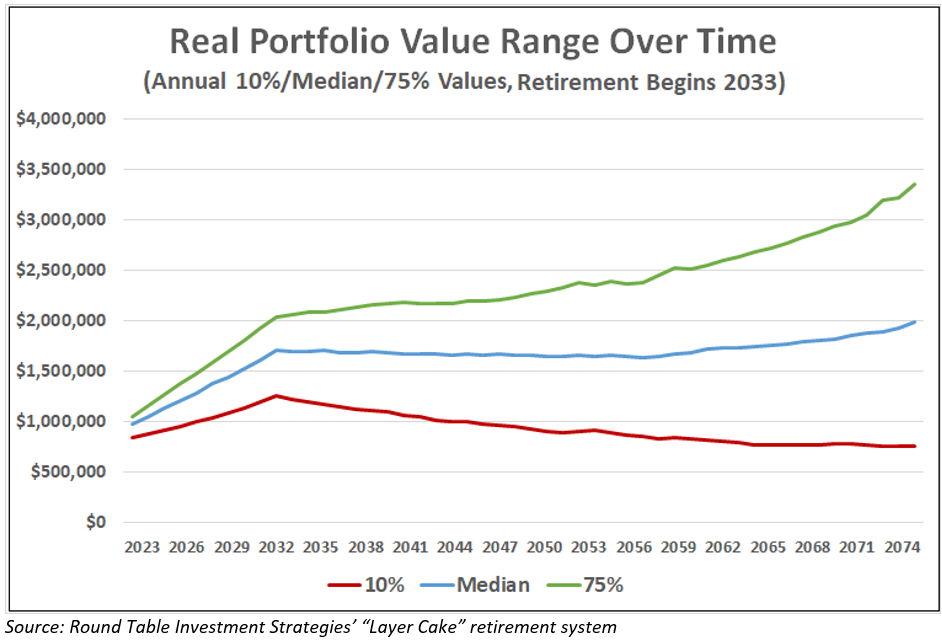

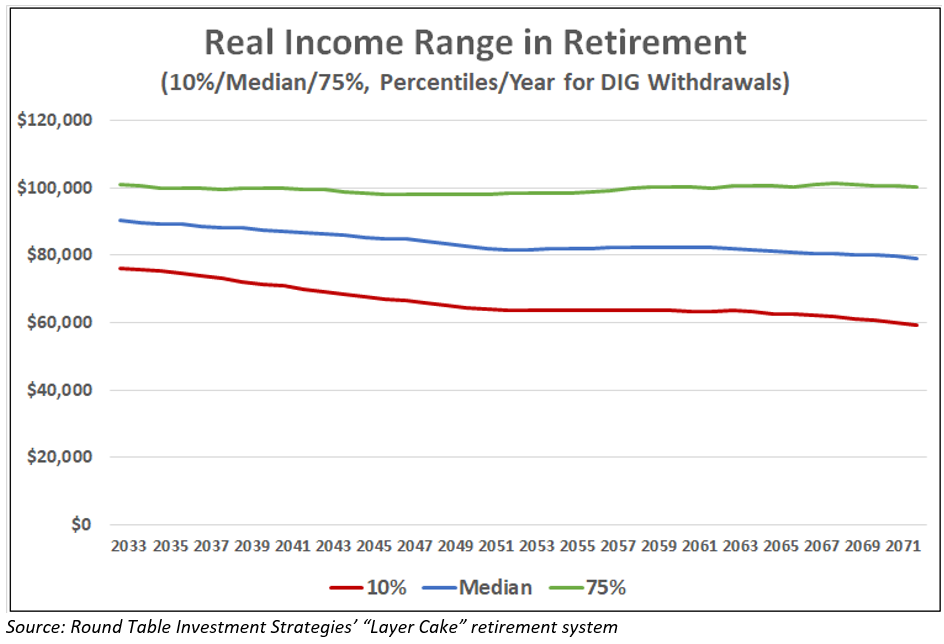

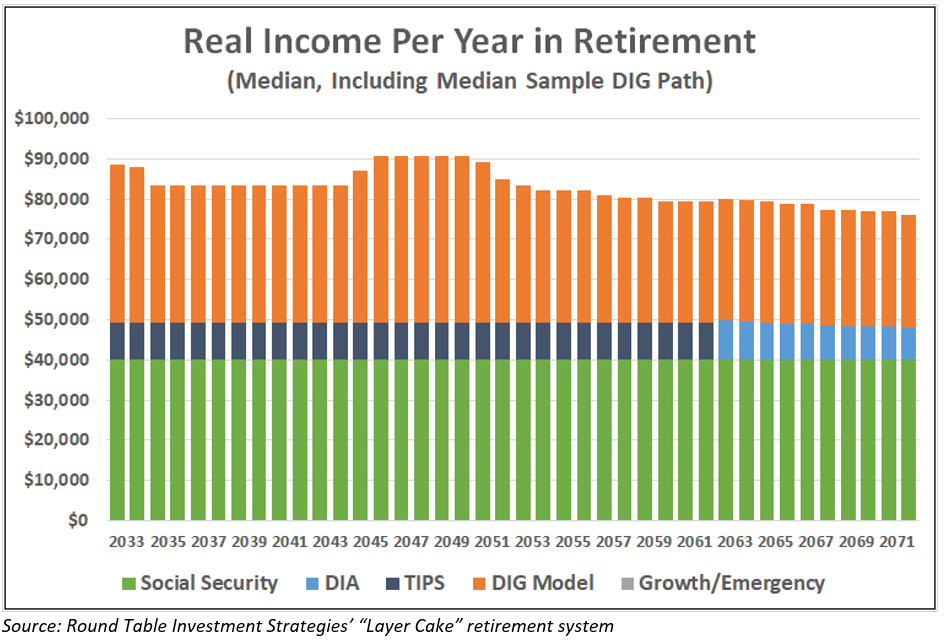

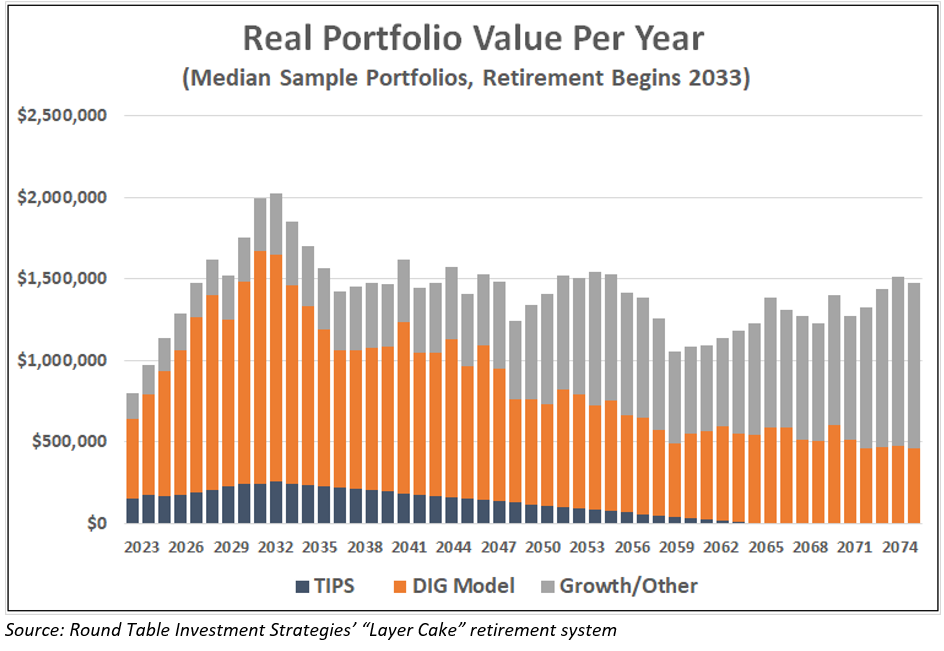

In Part 4, I showed a few in-retirement charts from my company’s proprietary “Layer Cake” goals-based retirement investing model. The model can also illustrate “good”/“normal”/“bad” outcomes for a multi-glidepath approach before retirement.

In the example below, an investor is 10 years from planned retirement and has $800,000 divided between a TIPS glidepath plus the projected cost of a deferred income annuity (DIA), a total-return glidepath into a “dynamic income and growth” (DIG) guardrails model, and emergency and growth portfolios. $50,000/year in portfolio additions will be divided across the TIPS, total return, and growth models.

The first chart below shows 10th, 50th, and 75th percentile Monte Carlo-derived total portfolio levels to and through retirement, starting at the end of the current year. The second chart shows 10/50/75-percent real income levels commencing the first year of retirement. The third and fourth charts show the breakout of sample median income and portfolio level, respectively, with the different sub-portfolios as described in Part 4 of this series.7

Course corrections

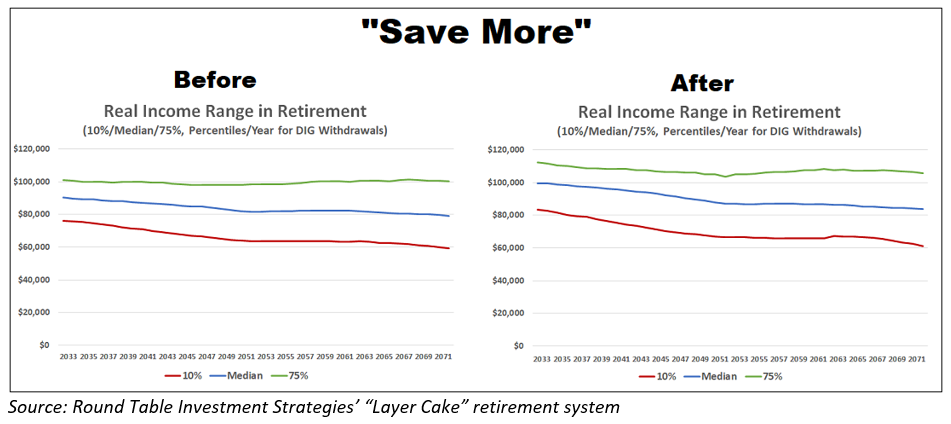

The use of good/normal/bad outcomes enables us to illustrate a range of solutions to one obvious question: What if I build a goals-based investment plan, and it turns out my plan can’t, in expectation, fund all my goals? For example, suppose the investor illustrated above has a $100,000/year retirement income budget, about $10,000/year more than the median outcome.

In general, there are four categories of solutions, which can be employed separately or combined. Two affect the asset side (i.e., the investment base), one affects the liability side (i.e., the nature of the goals), and one affects both:

You can save more

This improves the asset side by increasing the quantity of assets available to deploy for retirement income. For example, below is how the model changes if the investor above can add an additional $20,000 per year to the total return glidepath. Saving more increases income across the good, normal, and bad outcomes.

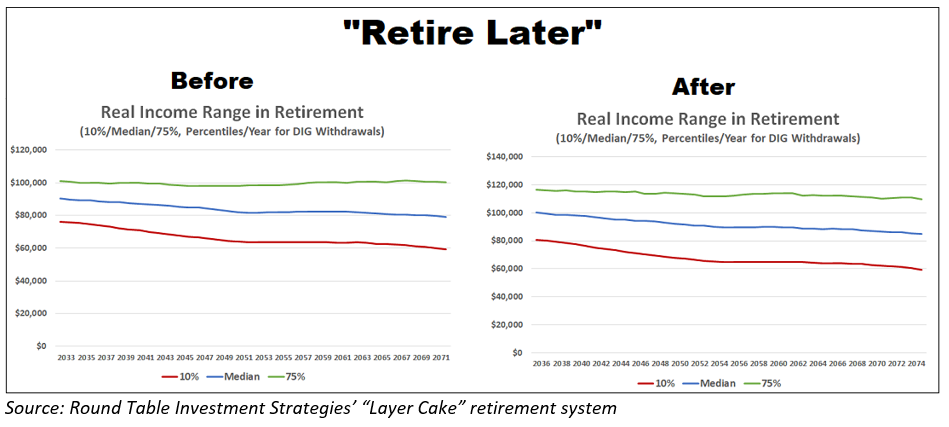

You can retire later

This improves the asset side by increasing the number of years of savings. It also improves (in an actuarial sense) the liability side by decreasing the number of years of retirement a person must cover with retirement assets. The charts below illustrate waiting three extra years to retire, such that retirement income in the “after” case begins three years later. Retiring later also increases income across the good, normal, and bad outcomes.8

You can adjust your goals

An option on the liability side is to lower the income target, most likely by reducing the amount of “flexible” spending. There is no before/after in this case, since the goals are being adjusted to the present reality of the assets. But the model still suggests a ~25% chance of meeting the original income goal.

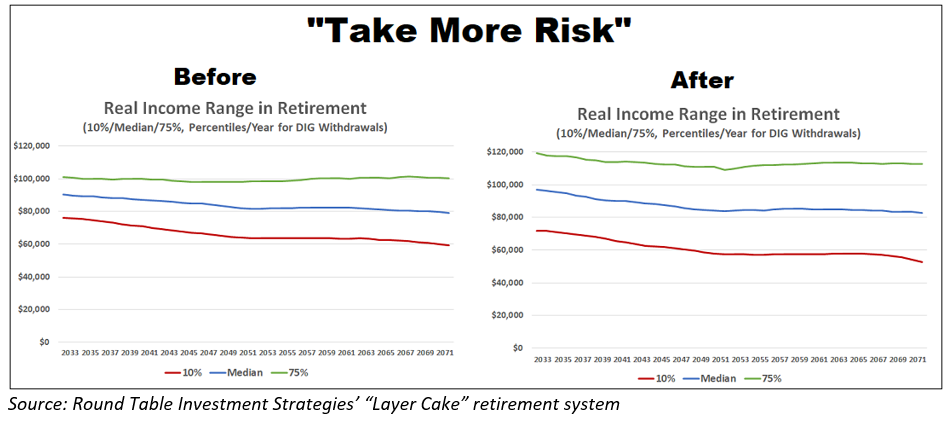

You can take more risk

This is often the default selection for retirement planners, but as this series has discussed at length, risk is always risky, even at long horizons. By taking more risk, you improve outcomes in expectation and under most scenarios, but the worst-case scenarios get even worse. In the example below, we take more risk by shifting assets from the TIPS glidepath to the total-return glidepath and by increasing terminal stock exposure in the total-return glidepath. The initial median outcome nearly rises to the $100,000 goal, and the “good” 75th percentile outcome rises more significantly. But in exchange, the 10th percentile outcome declines from nearly $80,000 to barely more than $70,000 in year-1 real income. Moreover, income on all three paths drops off slightly faster, because we calibrate our total-return model for real income to decline slightly over time in expectation, to align with research such as David Blanchett’s “spending smile” in retirement.

Taking more risk does increase someone’s odds of meeting their retirement goals, but it does so in a way that can make things even worse if markets perform poorly.

A common refrain in the advice profession goes something like this: “First determine your required rate of return, then make a plan to achieve it.” If I respond with, “Okay, my required return is 25% per year, what’s my plan?” most every advisor will rightly recoil at the danger that would be incurred in pursuing such a plan.

But how many advisors effectively perceive a discontinuity, such that replacing 25% with, say, 9% becomes somehow unproblematic? The research presented in this series suggests that there is no such discontinuity, but rather a spectrum whereby targeting any expected return above the risk-free rate requires the introduction of investments that improve outcomes on average and in most cases but make the worst cases even worse. The higher the target return, the more the risky assets, the better the upside, and the worse the downside. This can be acceptable if the downside is still sufficient to meet inflexible goals. But there should be a plan for what is to be done in the unlikely but non-negligible event that risk/return ex ante proves to be more risk and less return ex post, even over a long investment horizon.

Afterword

In Part 4 of this series and here in Part 5, I illustrated goals-based, long-horizon investing concepts with outputs from a proprietary “Layer Cake” model developed by my firm, Round Table Investment Strategies. We are migrating this model from spreadsheets to a web-based software system. The primary use case will be to serve our clients’ needs at Round Table, but we are considering making the system available to other advisors. If readers would have interest in using the layer cake software to model a goals-based retirement investment plan, please let me know in the APViewpoint comments on this article, or feel free to reach out to us.

In his role as chief investment officer for Round Table Investment Strategies, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 An exception can be if someone’s income has stock beta, as Moshe Milevsky, Zvi Bodie, and John Campbell have pointed out.

2 A more common scenario typically involves smaller contributions in the early years and larger contributions in the later years, but the concept is the same.

3 In a personal conversation with Prof. Robert C. Merton – whom I’ve referenced repeatedly in this series as my greatest inspiration in the field of finance – he mentioned that his theoretical glidepath models often start at 200% or 300% equity exposure. But he would acknowledge the impracticalities of attempting such a thing in practice.

4 The duration calculation requires assumptions about how to extrapolate real interest rates beyond 30 years. I typically use the 30-year CMT rate for all longer-term real cash flows. Insofar as this is inaccurate and/or other yield-curve effects cannot be perfectly mimicked through duration matching, a duration-matched portfolio will produce imperfect, but still reasonably effective, liability immunization.

5 It is admittedly debatable whether this is a true financial benefit in expectation. But the smoothing out of purchase timing tends to produce a psychological benefit at minimum and more consistent results across cohorts.

6 See also the explanation in Part 4 for why a risk-heavy total return portfolio may be appropriate even in retirement for someone with a sufficient base of safe income.

7 The orange bars illustrate a single sample outcome for the guardrails-based “DIG Model” described in Part 4. In this case, good markets enable a “pay raise” (i.e., increased real withdrawals) in 2044 and 2045, but over the long run the retiree experiences a slight decrease in real spending.

8 It is possible for poor market returns in the intervening three years to cause the year-1 retirement income stemming from the total return portfolio to be lower than it would have been three years prior. However, this is not a true case of outcomes growing worse, since those same poor markets would also have affected in-retirement asset value and income in the “before” case.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.