At 1,087 pages, a recent proposal to change capital rules would surely make life more complicated for big US banks. But will it make them safer?

The failure of three regional banks starting in March was an embarrassment for regulators, who had assured taxpayers that reforms put in place after the 2008 financial crisis had made the system much more resilient. The new proposal attempts to extend those reforms in light of the recent turmoil.

It recommends a few useful fixes. Recognizing that even regional lenders can cause risks to the entire financial system, regulators will now require banks with assets between $100 billion and $250 billion to comply with many of the tougher rules already applied to their bigger rivals. The proposal also revises a rule that had allowed those banks to opt out of counting unrealized gains and losses on some of their investments when calculating their capital ratios.

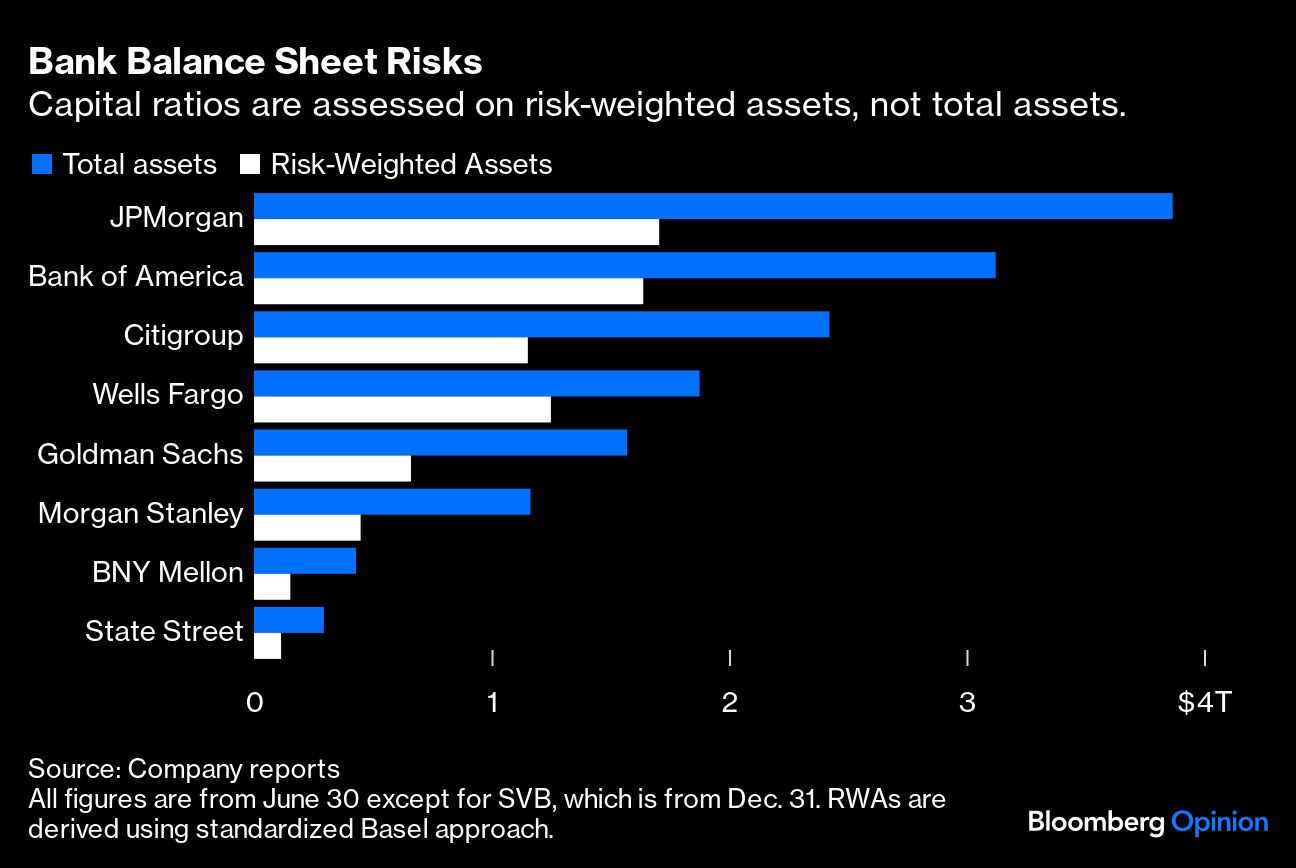

The heart of the proposal is a change to how capital is measured. Currently, banks can use their own models to assign risk-weightings to their assets, which determine how much capital they need. That allows different banks to measure the risk of the same loan differently, making it hard to compare capital adequacy across the system. More important, banks have an incentive to underestimate risk and boost leverage as they seek to maximize their return on equity.

Now regulators want to assign new standardized risk weightings instead. Much of the proposal explains how they plan to calculate the credit risk of particular assets and quantify the danger of operational losses. Trading desks can independently determine the risk of losses from market movements, but only if they use approved models. As a result of these and a few other requirements, regulators estimate the largest banks would need about 19% more capital and the biggest regionals will need as little as 5% more. Given that US banks remain overleveraged, this outcome would be progress of a kind.

Unfortunately, the proposal is flawed in key respects.

For one, it has little to say about the unexpectedly speedy exodus of depositors that occurred in March. When deposits can’t be relied on as a stable source of funding, the nature of banks’ balance sheets may require fundamental changes. Lenders may need to diversify sources of liquidity. Regulators should grapple with the implications of these changes more directly. (A forthcoming proposal to require more banks to issue long-term debt is a good start.)

Similarly, the capital proposal doesn’t do much to help banks weather sharply higher interest rates, the main cause of Silicon Valley Bank’s failure. Many banks hold large portfolios of “safe” fixed-income securities, which have no credit risk but lose value as rates rise. These bonds are often classified as "held-to-maturity,” which means banks don’t need to recognize a drop in value on their balance sheets or allocate capital to absorb potential losses. They should be required to have sufficient stable funding to support those assets. Otherwise, like SVB, they could be forced to start selling, locking in the losses.

Finally, for all their complexity, the proposed risk weightings aren’t likely to make banks much safer. Regulators have a poor history of judging the risks posed by different asset classes. After all, existing capital and liquidity rules have for years encouraged banks to load up on supposedly “risk-free” assets like government bonds, only for those securities to suffer huge losses as interest rates rose. There’s little reason to expect more accurate prognostications next time around.

A less complicated regime, simply requiring higher levels of loss-absorbing equity capital, would be both safer and less onerous. Such a reform would ensure banks have enough capacity to bear inevitable losses, strengthen the broader financial system and free regulators from the need to quantify every potential risk. It’s a good rule of thumb: When it comes to financial rules, simpler is usually safer.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.