Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Compared to the dotcom and great financial crisis recessions, our fiscal and monetary response over the last two years has been far more aggressive. But the true cost – in terms of inflation – presents a more threatening risk.

If you think back to the financial crisis of 2008 and the resulting near collapse of the financial system, your impression may be that the government acted swiftly to stabilize the economy and end the crisis. In fact, had it not acted as it did, the U.S. may well have been thrust into another Great Depression.

By contrast, in terms of employment and economic output, the economic damage resulting from the 2020 global pandemic was much more severe than what was experienced following the 2008 crisis. Yet, the recent economic recovery was extraordinarily rapid compared to 2008. To a large extent, the speedier recovery was the result of the government’s stronger fiscal responses that played out in 2020 and 2021. But, as the macro economist Richard Duncan has pointed out, that quicker recovery has come with the severe cost of high inflation. And maybe more.

Over the one-year period between March 2020 and March 2021, laws were passed that authorized $5.1 trillion of fiscal support of the U.S. economy. This amount was nearly 25% of GDP. That is more than five times the stimulus the government provided in 2008. The chart below illustrates the level of government fiscal responses to three recent financial crises beginning with the dotcom bust of 2000.

Consider the level of fiscal stimulus unleashed between 2020 and 2021, and the fiscal responses to other crises as measured by share of GDP. In 2000, the fiscal response represented only 0.4% of GDP and just 7% of GDP in 2008.

Of course, the outsized fiscal response to the pandemic caused a tremendous ballooning of the government’s budget deficit. For example, in 2016, the deficit was $400 billion. It skyrocketed to $3.1 trillion in 2020, equal to 15% of GDP.

In both 2008 and 2020, we saw very aggressive monetary policy responses. Between August and October 2008, the Fed’s assets (a proxy for the monetary base) more than doubled, increasing from roughly $800 billion to slightly more than $2 trillion.

Over the next six years, the Fed undertook three rounds of quantitative easing (QE), ending in October 2014. Later, we saw massive monetary policy responses to the pandemic. Over the two-month period from March to May 2020, the Fed’s assets grew by an astonishing 69%. The Fed’s policy of monetary expansion did not end until April of this year, by which time its assets had grown to nearly $9 trillion. In 2020 alone, the Fed’s assets grew by more than $3 trillion.

Richard Duncan has pointed out that the impact of the pandemic on employment and economic output was more sudden and deeper than in the 2008 crisis. However, the recovery from the 2020 crisis was much faster. For example, following the decline in GDP in 2008, it took 12 quarters for GDP to get back to its 2007 level. In 2020, real GDP declined by 10.1%, much more than the 4% decline between 2008-2009. Yet, it took only six quarters for US GDP to return to its pre-crisis level.

In terms of unemployment, it’s the same story. Following the 2008 market breakdown, by October 2009 unemployment had jumped to 10%. It took a full 10 years for unemployment to return to its 2007, pre-crisis level. But although unemployment shot up from 3.5% in February 2020, to 14.8% in April 2020, it took only 2.5 years to recover.

The performance of stocks following both the 2028 and 2020 crises presented a similar pattern. After sustaining a 52% decline in the S&P 500 between October 2007 and May 2009, it took 65 months for stock prices to recover to pre-crisis level. By contrast, it took only seven months for the S&P to recover from its 20% decline between December 2019 and March 2020.

While the recovery in terms of employment and economic output was much faster following 2020 compared to 2008, it cost us a great deal in terms of surging inflation. We’ve experienced inflation this year as high as 9.1%, a level not seen since the 1970s. (Had we calculated inflation in the same manner as a generation ago, the number would be closer to 18%). Inflation never exceeded 3.8% following the 2008 crisis.

Duncan says that it is difficult to allocate the share of responsibility for inflation to fiscal and monetary policies, considering other factors such as supply chain disruptions and Russia’s invasion of Ukraine He disagrees with those who attribute sole responsibility for inflation to global supply-chain disruptions. His argument for this assertion is convincing. Other nations have also experienced a significant increase in inflation attributable to the U.S. fiscal stimulus. That stimulus fueled demand for imports, ballooning other countries’ exports, the production of which created upward pressure on prices.

How much additional foreign goods did the U.S. import following the pandemic? After years of remaining flat, between December 2019 and March 2022, U.S. imports increased by 44%. This outsized increase in U.S. demand contributed to global inflation. Duncan believes that as much as one-half of the increase in inflation is attributable to increased imports. He points out that the much smaller fiscal response to the 2008 crisis did not result in high inflation.

The government’s stance on tax cuts represents a notable difference between the fiscal policy strategies undertaken in 2008 and 2020. In 2008, tax cuts totaling hundreds of billions of dollars were a prominent component of the response to the crisis. In 2008, tax cuts accounted for 40% of the government’s fiscal stimulus versus 10% in 2020. Therefore federal government revenues fell by more than $400 billion in 2009 but increased by $626 billion in 2021. Government revenues did decline in 2020, but by only 1%. In 2021, government revenue ballooned by 18%.

Duncan asserts that government stimulus prevented a depression in both 2008 and 2020. He also states that the Great Depression of the 1930s could have been prevented had the government, between 1930 and 1931, stepped in with dramatic increases in fiscal stimulus. Clearly, policymakers have learned from the mistakes made during the 1930s.

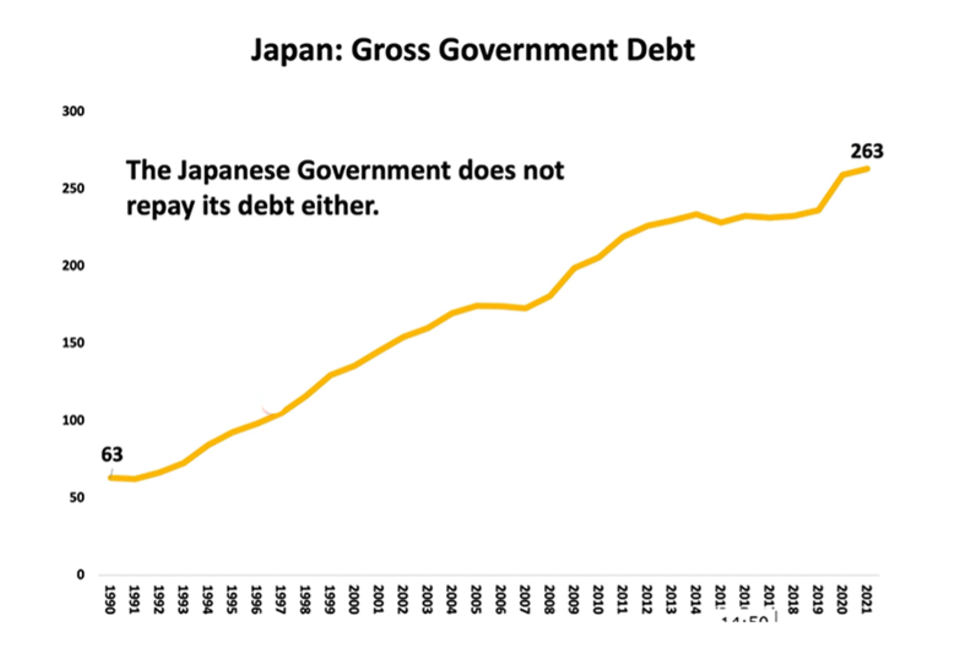

We often hear the concern expressed that future generations will be saddled with repaying the debt generated by our reckless spending. But as the charts below illustrate, the government never repays its debt.

Source: Richard Duncan Economics

Source: Richard Duncan Economics

Says Duncan, “The U.S. government doesn’t repay its debt. And the Japanese government doesn’t repay its debt either.”

The following chart shows that Japan’s debt, as a percentage of GDP, has increased from 63% in 1990 to 263% in 2021. This may indicate that, if needed, the US can afford to take on a much greater level of debt. In relative terms, at 127% of GDP, US debt is less than one-half that of Japan’s. Even with debt approaching 300% of GDP, Japan has experienced no significant inflation. Over recent years, it has spent more time battling deflation.

A key question for us to consider is, “How much damage will the Fed have to inflict on the economy and unemployment to bring down inflation?” As Duncan states, “Only after inflation has fallen back to the Fed’s 2% target will we know if a very rapid economic recovery was worth the price.”

In terms of destroyed wealth, the price yet to be paid may be exorbitant. In this article, I predicted the painful, near-term destruction of $34 trillion in wealth assets. Advisors must be mindful of the potentially devastating impact on clients’ post-retirement standards-of-living. This is a moment to take special care to mitigate timing risk.

My thanks to Richard Duncan for allowing me to share data from his excellent and highly recommended Macro Watch video newsletter.

Wealth2k® founder David Macchia is an entrepreneur, author, IP inventor and public speaker whose work involves improving the processes used in retirement income planning. David is the developer of the widely used The Income for Life Model®, and the recently introduced Women And Income®. David has authored many articles on the subjects of retirement income planning and financial communications. He is the author of two books, Constrained Investor®, and Lucky Retiree: How to Create and Keep Your Retirement Income with The Income for Life Model®

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.