Prepare for the Destruction of $34 Trillion in the Coming Months

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

What would be the impact on your business if $34 trillion in wealth assets were destroyed over the next several months? Answering this question will help you plan for the worst effects of what will be a monumental episode of wealth destruction. There is still time to act to protect the income generation capacity of your retiree clients.

With inflation hitting 9.1%, what is off the table are those actions that propelled asset prices upwards for 14 years. In a dramatic Fed policy reversal, quantitative easing is gone, as are zero-percent interest rates. The economist Richard Duncan declared, “Americans should prepare for a very hard landing?” How hard? Harder than we wish to imagine. Several years ago, while vacationing in Miami, my kids asked me to take them parasailing. The way I stomach felt “sailing” 400 feet above the water is an apt analogy.

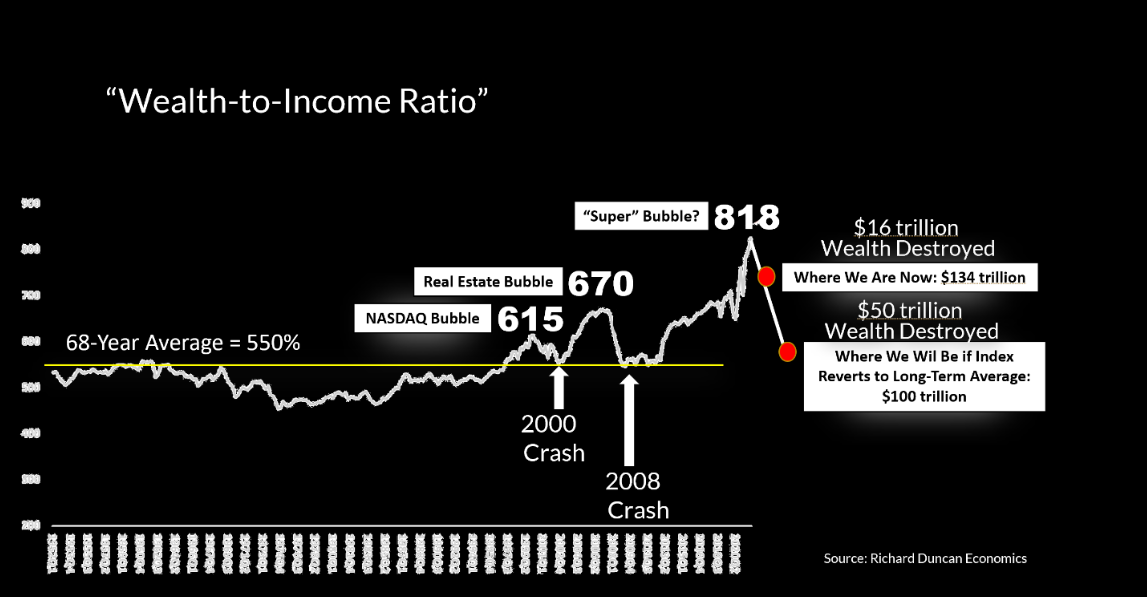

The behavior of a key index

Between 2009 and the end of 2021, household sector wealth soared by 150%, increasing from $60 trillion to $150 trillion. To track the household sector wealth, the Fed’s publishes an index called Household Net Worth as a Percentage of Disposable Personal Income. The index, which is commonly referred to as the Wealth-to-Income Ratio, has a 68-year average is 550%. Its interesting to observe how the index behaved in the face of past examples of record high stock prices. For example, in March 2000, the index reached a then, all-time high of 615%. Notable for sky-high valuations of soon-to-be-failed companies such Worldcom, Global Crossing, NorthPoint Communications, Alta Vista, InfoSpace, Pets.com, Ask Jeeves, and Excite, this was the apogee of the “Dot-Com bubble” that burst shortly thereafter. By October of 2002, the NASDAQ 100 had fallen by 78%.

How did the wealth-to-income ratio react? The index reverted to its long-term average of 550%.

In October 2007, the wealth-to-income ratio reached another all-time high of 670%. Over the next 18 months, the Dow fell by more than 50%. The index? It again fell right back to its long-term average of 550%.

As of June 30, 2022, the wealth-to-income ratio stood at a never-before-seen level of 818%. Richard Duncan has calculated that, due of the sell-off in stocks, $16 trillion of wealth has been destroyed this year, dropping total household wealth to $134 trillion. If over the next several months, the index once again falls back to its long-term average, we can expect an additional $34 trillion in wealth destruction, taking total household sector wealth from $150 trillion down to $100 trillion. This is a likely outcome barring some extraordinary policy reversal by the Fed. But it is hard to imagine that happening given today’s rate of inflation.

“Actual” inflation is likely much higher than the official number. According to Shadow Government Statistics, if inflation were calculated in the manner that it was back in 1990, we would have an “official” inflation rate of more than 17%. If you’ve visited a supermarket lately, you probably view the 1990 calculation as the mote accurate measure.

How did we get here?

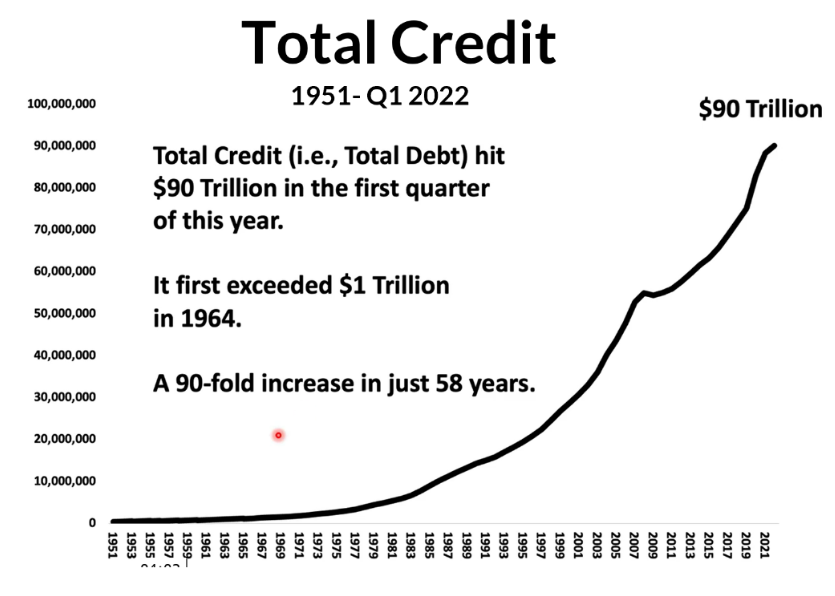

It was in 1964 when total credit first exceeded $1 trillion. Over the subsequent 50 years, total credit expanded 90-fold, rising to today’s total of $90 trillion. Since 1968, when Congress authorized the delinking of gold and the dollar, credit growth became the primary driver of economic growth (total credit = total debt). Over the past five decades, for the U.S. economy to avoid a recession, credit growth must be at least 2% after inflation. Between 1952 and 2009, nine times credit growth fell short of 2% after inflation. In all nine cases, the U.S. entered economic recession.

Duncan has pointed out that, between the early 1980s and 2009, credit growth substantially outpaced economic growth. The surge in credit expansion blew the economy into an bubble leading to the 2008 crash. But from 2009 thru 2019, credit growth and economic growth were demonstrably weaker. The government responded to both the 2008 crash and the COVID-19 pandemic with massive fiscal stimulus. The Fed respond to both crises by slashing the federal funds rate to 0%, and by created unprecedented amounts of money. In both instances, the combination of huge fiscal stimulus and massive money creation twice prevented the economy from falling into depression. These policy responses created never-before-seen levels of wealth that drove consumption and economic growth.

From 2008 to 2021, total government debt nearly tripled, increasing to $28.3 trillion. And the Fed’s balance sheet increased by more than 800%. Classic economics may have predicted hyperinflation resulting from these moves. But that was prevented by the massively deflationary impact of globalization. In fact, from 2009-2020, inflation averaged just 1.6%. That began to change in 2021. Duncan says, “The reemergence of high rates of inflation threatens to collapse the global economic bubble that has been forming for decades.” In fact, since the fourth quarter of 2020, credit growth has been contracting. Remember, when this happens, we can expect an economic recession.

What will the Fed and the government do now? This time, it is unlikely that the government will step in to save investors. Additional fiscal stimulus would likely drive inflation even higher. And in the face of high inflation, the Fed’s response is money destruction, not money creation. Investors, therefore, are in a very tough place.

The risk to retirees

I've written numerous times about a segment of retirees I call “constrained” investors. I’ve also expressed my belief that advisors owe a heightened level of care to these investors as they approach or enter retirement. To properly plan income for constrained investors, risk mitigation measures must be incorporated into their investing strategies. Constrained investors require protection against both timing and longevity risks This is why I have argued vigorously that investment advisors owe it to constrained investors to recommend annuities. On my Constrained Investor website, I state, "Timing Risk is a big, scary monster of a financial threat. Don't let it feast on your income!”

Unfortunately, timing risk is enjoying a lavish buffet. Ultimately, longevity risk is an even greater threat to millions of constrained investors. I speak with advisors frequently and always find a moment to quote my catch phrase, “No retiree stops needing income.”

I have a prediction about how retirement income planning by investment advisors will unfold: If we experience a financial bloodbath that features an additional $34 trillion in wealth destruction, history will show that this was the event that once-and-for all broke the dominance of withdrawal strategies. And I will be able to happily remove “defender of annuities” from my LinkedIn profile.

Wealth2k® founder David Macchia is an entrepreneur, author, IP inventor and public speaker whose work involves improving the processes used in retirement income planning. David is the developer of the widely used The Income for Life Model®, and the recently introduced Women And Income®. David has authored many articles on the subjects of retirement income planning and financial communications. He is the author of two books, Constrained Investor®, and Lucky Retiree: How to Create and Keep Your Retirement Income with The Income for Life Model®

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All