Recent articles in Advisor Perspectives by David Blanchett and by Zvi Bodie and Dirk Cotton have dealt with single-premium immediate annuities (SPIAs) used to generate lifetime income in retirement. The focus of those articles was the pricing and the risks of going without inflation protection. In addition to SPIAs, insurers also offer variable annuities (VAs) and fixed-indexed annuities (FIAs) with optional riders known as guaranteed lifetime withdrawal benefits (GLWBs). I’ll expand on the recent articles by comparing the income-generating properties of SPIAs versus VAs and FIAs, and place particular emphasis on how inflation risk impacts inflation-adjusted income.

Example

This analysis is based on a 65-year-old female making a $100,000 purchase of an annuity product. She has the following purchase options:

- An inflation-indexed SPIA (also called a “real annuity”) with lifetime payments that adjust annually based on actual inflation (CPI-U) – Principal Financial;

- A “COLA” SPIA with lifetime payments that increase by fixed percentage each year – Penn Mutual;

- A VA/GLWB providing lifetime withdrawals that may ratchet up based on underlying investment performance – Vanguard/Transamerica; or

- A FIA/GLWB – providing lifetime withdrawals that increase each year based on the credited returns in the contract – Allianz.

In projecting retirement income, I assume this individual lives to age 90, which is the expected average for a female annuitant based on the latest Society of Actuaries annuity mortality table.

Inflation and investment modeling

The modeling for this analysis involves Monte Carlo projections of variable future inflation and investment performance. The inflation-indexed SPIA has the unique property that real, inflation-adjusted income will remain level regardless of inflation. Real income generated by the COLA SPIA will vary with inflation, and both inflation and investment performance will impact real withdrawals for the VA and FIA.

For investment modeling, stocks are assumed to earn an arithmetic average nominal return of 7% and bonds 3%, with standard deviations of 20% and 7% respectively.

For inflation modeling, there are strong indications pointing to a 2% future average. The current Treasury/TIPS spread is just under 2% and we also know that the Fed is targeting 2% inflation. However, my purely subjective view is that there is a somewhat greater risk of higher inflation, and I’ve modeled future average inflation based on the following probability distribution:

The modeling involves generating 10,000 25-year inflation scenarios. Each of the 10,000 scenarios involves random selection of average future inflation based on the above probability distribution. Then, based on inflation volatility since the early 1980s, I generate random year-by-year inflation assuming a 1.3% standard deviation.

Inflation-adjusted indexed SPIA versus COLA SPIA

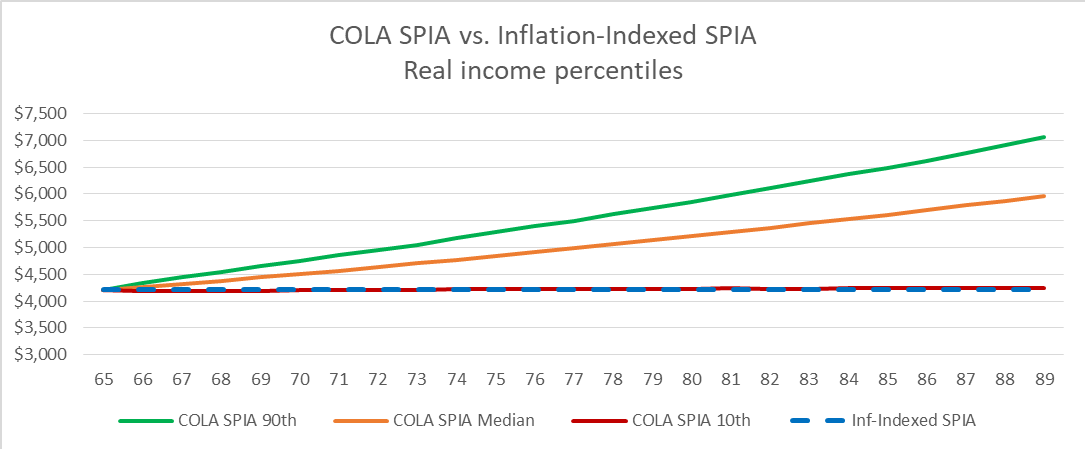

The first analysis compares a COLA SPIA to an inflation-indexed SPIA, similar to the analysis in the Blanchett article. Principal Financial is the only insurer currently offering an inflation-indexed SPIA, and, as of early June 2019, $100,000 would purchase an annual lifetime income of an initial $4,211 increasing with inflation each year.

For the COLA SPIA, I determined what fixed annual percentage increase in payments this individual could obtain for $100,000 with the same initial $4,211 payment as for the inflation-indexed SPIA. The pricing service CANNEX provides pricing for 15 companies offering COLA SPIAs, and, for this 65-year-old female, the best rates are from Penn Mutual. By combining COLA SPIAs with 3% and 4% step-ups, we can construct a SPIA that will pay an initial $4,211 with payments increasing by 3.6% each year. These are nominal payments, so the real inflation-adjusted payments will vary depending on Monte Carlo generated inflation. The chart below provides a comparison of the inflation-indexed SPIA versus the COLA SPIA.

The projection for the inflation-indexed SPIA is depicted by a dashed blue line and it remains level over the full retirement at $4,211 in real dollars. For the COLA SPIA, nominal income will increase at a fixed 3.6% each year, but real income will vary depending on inflation. I show the 90th percentile (green), median (orange), and 10th percentile (red).

It turns out by pure coincidence that the 10th percentile for the COLA SPIA almost exactly matches the inflation-adjusted indexed SPIA. So there’s a 90% chance that purchasing the COLA SPIA will generate more real income than the inflation-indexed SPIA and a 10% chance it will do worse. This result is consistent with Blanchett’s findings. The upward-sloping median result for the COLA SPIA indicates that it beats inflation on average; this would be expected given its 3.6% annual increases in payments versus inflation averaging 2.3% overall. The 90th percentile beats inflation by a bigger margin.

These results look very favorable for the COLA SPIA, but it’s worth cautioning that they are a direct reflection of my particular inflation model, which was built with considerable subjectivity. Higher future average inflation would reduce the advantage of the COLA SPIA and higher inflation volatility would increase the spread between 10th and 90th percentile results. The inflation-indexed SPIA has the unique property of providing a pure hedge against very high inflation, which is a material risk that every retiree must acknowledge and consider.

SPIAs versus VA/GLWB

Next I’ll use the previous SPIA chart as a base case and provide a comparison with the lifetime withdrawals generated by investing $100,000 in a variable annuity with a GLWB. The particular VA/GLWB I have chosen is a Vanguard product that has Transamerica as the insurer. In this example, the 65-year-old can withdraw 5% or $5,000 in the first year, and nominal withdrawals may ratchet up (i.e., increase without future decreases) depending on underlying investment performance. For investments, I assume the Vanguard balanced fund with 65% stocks. More details about the Vanguard product can be accessed via this link.

The ratcheting-up feature of GLWBs is prominent in how these products are promoted – “Your withdrawals can increase, but never decrease.” But, in real terms, allowable withdrawals will vary and may indeed decrease. The chart below superimposes projections for the VA/GLWB over the previous projections for the SPIAs. For the VA/GLWB I use dashed lines and the same red, orange, and green colors for 10th, median, and 90th percentiles.

Withdrawals from the VA/GLWB start out at a higher level ($5,000) than the SPIA payouts ($4,211). They also follow more varied paths, depending on the variability of underlying investment performance and inflation. This chart brings home the important point that results in real dollars, reflecting actual spending power, can indeed decrease, even substantially – which is very different from the marketing message used to promote certain products.

Compared to the SPIAs, the VA/GLWB offers a wider range of potential outcomes, both upside and downside as might be expected when investment performance is brought into the picture. It’s hard to determine which product offers the better median performance because the paths cross, but I’ll address this later in the article with summary measures for all the products.

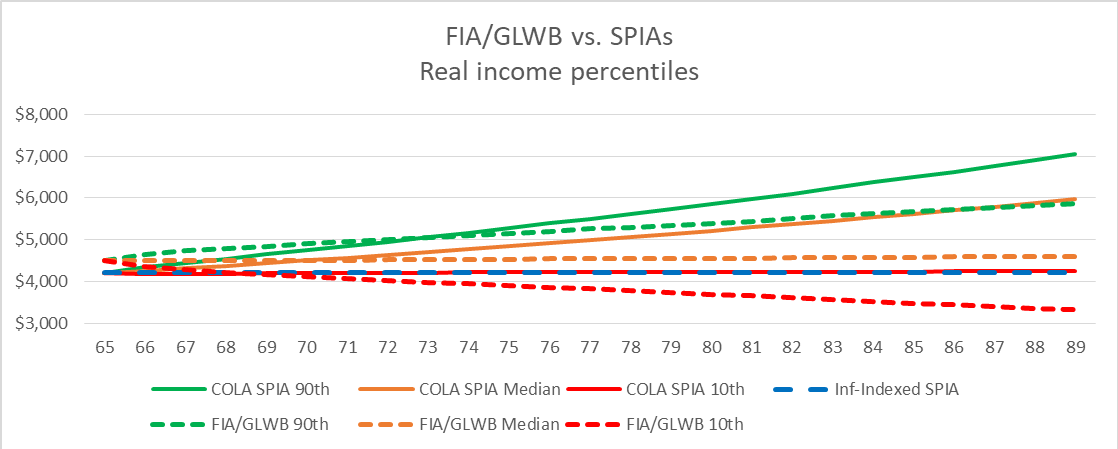

SPIAs versus FIA/-GLWB

Now we’ll compare the SPIAs to an overlay of a fixed-indexed annuity (FIA) with a GLWB, in this case the Allianz Core Income 7 described in more detail here. FIAs are similar to VAs, but the range of potential outcomes is constrained by caps and floors on performance of an investment index or by crediting partial participation in index performance. For the FIA in this example, the index will be a performance of the S&P 500 without dividends (assumed 2% for modeling) with returns (referred to as “interest credits”) constrained to a band between a 0% minimum and a 4.5% cap. Allowable FIA/GLWB withdrawals start at 4.5% or $4,500 for this example and their nominal value increases each year by the interest credit. Because of the 0% minimum, allowable withdrawals can never decrease in nominal terms, although there can be real decreases.

The chart below replaces the VA/GLWB projections from the previous chart with FIA/GLWB projections and again provides a comparison to the SPIA base case projections.

The results we see are less positive than in the previous chart for the VA/GLWB. Instead of a tradeoff of performance versus volatility, we now see projected performance (dashed lines) that is inferior to the COLA SPIA (solid lines) for all the percentiles shown. The median case does appear to match inflation (flat line), but from a lower base $4,500 than for the VA/GLWB ($5,000). Overall the COLA SPIA appears to be a superior to the FIA/GLWB as an income generator.

In fairness, I should point out that this result reflects one particular FIA and the way this particular product is structured. There are many different FIA products and different ways of structuring them – choices of index, return crediting method, timing of commencing withdrawals, and others. So it’s hard to make blanket judgments. I view this particular analysis more as an example of how to evaluate FIA products rather than providing a verdict on the product line.

One very important negative about both FIAs and VAs is that insurers typically have flexibility to change terms, such as the fees and caps, after purchase. For example, the Vanguard VA/GLWB currently charges 1.20% per year for the GLWB, but has the flexibility to raise this to a maximum of 2%. The cap on the Allianz FIA is currently 4.5% but can be lowered to a minimum of 0.25% at the discretion of the insurer. Insurers have no such flexibility with SPIAs, so the payment structure is more certain.

Although there is only one issuer of inflation-indexed SPIAs, there is more competition among issuers of COLA SPIAs and especially among issuers of “vanilla” level-pay SPIAs. Given the simple structure of those products, issuers can compete only on price and the COLA rate. This creates a relatively efficient, consumer-friendly market. By contrast, issuers VA/GLWBs and FIA/GLWBs can compete on any of the terms underlying the complex structure of those products. That creates a market where it is more difficult for consumers to know that they are paying a fair, competitive price.

Summarizing the results

The following chart compares the products by calculating internal rates of return, based on an upfront investment of $100,000 and 25 years of payments.

On this basis, the COLA SPIA and the VA/GLWB appear to be the most attractive of the four products. A footnote on the VA/GLWB is that it is the only product I project to leave a bequest at age 90. And the text box shows the projected IRRs with bequests projected for the median and 90th percentiles. With the bequest, the IRR median for the VA/GLWB is 1.91%, very close to the 1.87% for the COLA SPIA.

Final comments

It’s unfortunate that projections for annuity products that clients see are typically done in nominal terms. Clients should be made aware of what can happen to real, inflation-adjusted spending power. Projections of steady, non-decreasing nominal income can mislead, when in fact real income will be variable and can potentially decrease.

It’s also unfortunate that only one company offers an inflation-indexed SPIA and that the pricing is not as aggressive as for COLA SPIAs, where there is competition. A more attractively priced inflation-indexed SPIA would provide a better way to avoid what Bodie and Cotton properly refer to as betting on inflation. This is the sole source of variability in the COLA SPIA projections and contributes to the variability shown for the VA and FIA.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

More Fixed Income Topics >