The only retirement contract that both insures against longevity risk and hedges against inflation is a life annuity that is linked to the consumer price index (CPI). It is denominated in the same units of account as Social Security benefits. We call it a “real annuity,” although it is also referred to as an inflation-indexed single-premium immediate annuity (SPIA). In computing a person’s replacement ratio of preretirement income, we can add Social Security benefits and the income produced by a real annuity to arrive at a meaningful number.

An annuity that is not linked to the CPI we call a “nominal annuity.” It is measured in units that are different from Social Security, so it would be a mistake to add the two in computing a replacement ratio. Despite those obvious facts, real annuities are largely ignored in practice and they comprise a tiny portion of the annuities market. The vast majority of income annuities sold are fixed in nominal dollars. From the perspective of rational economic decision-making, this is a puzzle. Let’s call it the “nominal annuity puzzle.” The purpose of this article is to explore the reasons behind this puzzle and to suggest ways to solve it.

The lack of interest in real annuities can be explained by a lack of recognition that the purchase of a nominal annuity constitutes a speculative bet on future inflation rates and that the real annuity is the risk-free asset. Specifically, we disagree with advisors who suggest that:

- Nominal annuities should be the starting point for an analysis of the cost of real annuities;

- The cost of a real annuity is represented by its lower initial payment compared to that of a nominal annuity;

- Insurers don’t offer real annuities because they don’t want to accept inflation risk; and

- Graduated-payment annuities, which go up at the expected rate of inflation, are an adequate inflation hedge.

There is only one U.S. insurer offering income annuities with annual payments linked to the consumer price index (CPI) – The Principal. There are two websites that offer quotes for Principal SPIAs, ImmediateAnnuities.com, and BlueprintIncome.com.

Some advisors suggest that insurers don’t offer real annuities because they don’t want to accept inflation risk. However, an institution can hedge the risk of inflation by purchasing TIPS, or by means of inflation swaps or “CPI swaps.” The net result of combining a nominal annuity with an inflation hedge is a synthetic real annuity. Real annuities are not widely offered due to a lack of market demand and not because insurers can’t hedge inflation risk.

Hedging eliminates the risk of loss by giving up potential for gain. In contrast, when we insure, we pay a premium to eliminate the risk of loss but we retain the potential for gain. Real annuities hedge inflation risk; they do not insure it. This is an important distinction because hedging costs nothing (except for small transaction costs) while insurance can be quite expensive.

An analysis of the cost-effectiveness of real annuities will be heavily influenced by the manner in which the argument is framed. A common way of framing this annuity comparison is to assume that nominal annuities are the appropriate baseline and then to consider the “additional” cost of hedging inflation risk. This is opposite the way economists generally consider investment risk. We typically begin with the risk-free rate of return and then consider the wisdom of increasing our return by taking on additional risk.

This is also the correct framing of the real annuity comparison, i.e., beginning with the real annuity as the risk-free asset and then considering the additional payout that is implied by exposing the annuitant to inflation risk.

Economic theory implies that, faced with a choice between two annuities (SPIAs) costing the same amount, one of which is fixed in nominal dollars and the other in real dollars, a rational individual should consider the real annuity to be risk-free and the nominal annuity to be risky. The reason is that the individual cares about maintaining their level of consumption, given that future inflation (CPI) is uncertain. A consumer can only purchase goods and services with real dollars.

The other consideration in choosing between the two annuities is the individual’s beliefs about future inflation, its mean, variance, and tail risk (hyperinflation). Figure 1 shows U.S. annual inflation rates based on the Bureau of Labor Statistics CPI-U from 1914 to 2018.

For simplicity, let’s assume a flat term structure of real and nominal interest rates for which short-term bonds have approximately the same yield as long-term bonds so that we can talk unambiguously about the real and nominal rates of interest without specifying the maturity. When comparing two level-payment annuities of equal present value (i.e., cost), if the real rate of interest is lower than the nominal rate of interest, which is normally the case, the real annuity must have a lower starting value than the nominal annuity. The mathematics of compound interest and the time value of money guarantee this fact.

For example, let the present value of the annuities be $100,000, the risk-free real rate 1% per year, the nominal risk-free rate of interest 3% per year, and the number of years 20. The difference between the nominal and real risk-free rates is the forward rate of inflation, or the “break-even” inflation rate. It is an indicator of market expectations, consisting of an implicit forecast plus a risk premium. In this example, it is 2% per year over the next 20 years.

The term cost of living adjustment (COLA) is used by insurance companies to refer to one of two types of annual increases in the yearly payment:

-

Cost of living adjustments (COLA): A constant percent increase. Most insurers offer graduated payment increases from 1% to 5% per year. We refer to this type of annuity as a “graduated-payment nominal annuity,” and it is fundamentally different from a real annuity. Payments are not linked to inflation, so this type of COLA is not an inflation hedge.

-

CPI-U index: As mentioned, The Principal offers a true Bureau of Labor Statistics (BLS)-derived CPI adjustment in addition to nominal and graduated-payment annuities. This percentage is recalculated January 1st of each year. Your annuity income can either increase or decrease for that year based on the government's reported change in the CPI.

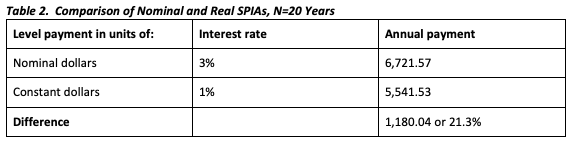

Let’s consider how to compare these income streams. Nominal and real annuities are as different from each other as annuities denominated in different currencies. For example, think of an annuity denominated in U.S. versus Canadian dollars. If I live in the U.S., I will almost surely not be interested in the Canadian annuity, unless I want to speculate on the U.S./Canadian dollar exchange rate. Now suppose that the interest rate in Canada is 1% per annum and in the U.S. it is 3%. A 20-year nominal annuity would offer a level payment of 5,541.53 Canadian dollars per year while the U.S. annuity would offer payments of 6,721.57 U.S. dollars (see Table 1).

Should we regard the difference of 1,180.04 as the cost of choosing Canadian rather than U.S. dollars?

Clearly, it is not a cost. The two annuities are in different currencies.

Canadian retirees will choose a Canadian annuity and U.S. retirees to choose the U.S. dollar annuity. For a Canadian to buy a U.S.-dollar annuity would be speculation on the future exchange rate between the two currencies. Retirees would avoid such speculation as imprudent if they understood its nature.

Similarly, constant and nominal annuities are denominated in different “currencies.” The real annuity is measured in constant dollars – we can call them “CPI bundles.” In Table 2 as in Table 1, we can see that nominal and constant dollars are different “currencies” so that their difference does not represent a cost, either.

Choosing the nominal annuity amounts to speculating about the future value of the CPI, i.e., on the rate of inflation. It might be tempting to do so if one believes that the actual rate of inflation will be less than the 2% spread between the nominal and real interest rates. But then the annuitant would be deliberately exposed to inflation risk and betting that future inflation rates will be lower than the market consensus at the time the annuity is purchased. Like foreign exchange-rate bets, this sort of speculation is imprudent for retirees.

To see this, let’s consider the actual history of the CPI. In Figures 2a and 2b, we compare the 20-year history of a real annuity versus a level-payment nominal annuity from 1970 to 1990 in terms of their “real values.” The real value of the annuity is the inflation-adjusted purchasing power of the annuity’s annual payments to the annuitant. For the real annuity, annual payments are fixed at $4,550. The level-payment nominal annuity’s payment start at $6,440. By 1976 the payment’s real value has fallen to $4,550 ex post. By 1990, its real value was $1,723.

Note that CPI-adjusted annuity payments ex ante equal CPI-adjusted annuity payments ex post and this is what we mean by “risk-free.“

Figure 2b adds to Figure 2a the annual payments of a 3% graduated-payment nominal annuity (blue dashed line) assuming that future inflation (ex ante) indeed equals that 3% per year assumption along with the real value of these payments (solid blue line).

In times of high inflation, such as the U.S. experienced in the 1970s and early 1980s, a real annuity will quickly provide for more real dollars of consumption than a nominal annuity. Beginning in 1970, the real annuity would have provided more real income after only about five years (the initial payment from a level-payment nominal annuity will be higher than that of a real annuity when inflation is expected).

We note that inflation from 1970-1990 averaged about 6.4% per year and that the 3% graduated-payment nominal annuity payments fell far behind the payments of the CPI-adjusted annuity in real dollars.

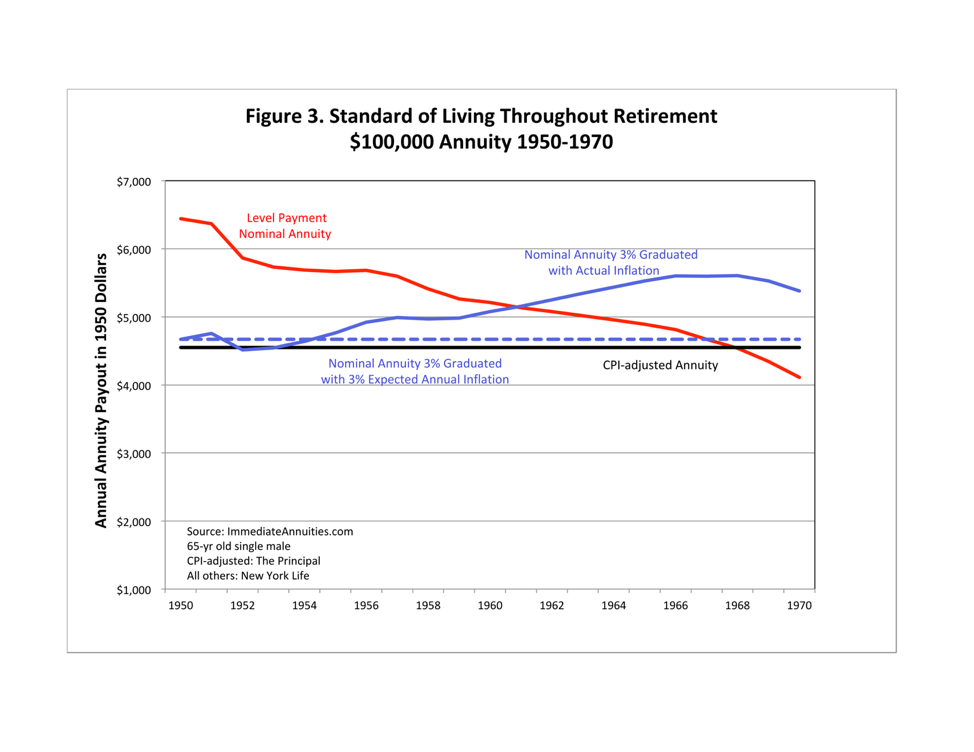

In periods of lower inflation, such as the period from 1950-1970 shown in Figure 3, the break-even period for the payment is longer. Annualized inflation ran just above 2% per year during that period and the real payments from the level-payment nominal annuity remained greater than those of the real annuity for about 18 years. Except for a brief early period, the real value of 3% graduated-payment annuity payments always exceeded those of the real annuity and exceeded the real value of the graduated-payment annuity payments after 11 years.

Some advisors and retirees consider the difference between the initial payment of the nominal annuity ($6,440 in the above example) and the real annuity ($4,550 in the example), or $1,890, to be the cost of inflation protection with the real annuity. That is incorrect, in the same way that the direct comparison of U.S. and Canadian dollars was incorrect. The two annuity payments are in different “denominations” or units of measure. The figures above show that the constant-dollar difference in payments can vary substantially year-over-year depending on inflation.

We recognize the argument that real annuities are offered by a single U.S. insurer whose pricing is not subject to competitive pressures, but we don’t address annuity pricing. Instead, we note that nominal annuities are a speculative bet on future inflation rates, a bet that is imprudent for retirees and, indeed, one which many would make unwittingly.

Purchasing a nominal rather than a real annuity is a decision to intentionally expose the annuitant to inflation risk. This inflation bet is similar to the example above in which a Canadian retiree buys a U.S. dollar-denominated annuity and inadvertently speculates on the future foreign exchange rate. Neither is the kind of speculation a retiree should consider.

Nonetheless, all financial products have pros and cons and, given their full appreciation in the context of the remainder of the retirement plan, a retiree can make a rational decision to purchase nominal or real annuities, or neither. Annuitants should understand before choosing that nominal annuities include a speculative bet on future inflation rates and the potential for substantial losses of purchasing power should high rates of inflation return, while real annuities include neither.

The safer choice for a retiree is the real annuity, which avoids speculating on inflation rates, while hedging inflation and its tail risk.

Zvi Bodie is an independent financial consultant and educator. His main professional interest is to firmly establish finance as an applied science built on the principles explained in his books and websites. He is Professor Emeritus at Boston University, where he taught from 1973 to 2016. He has served on the finance faculty at the Harvard Business School and MIT's Sloan School of Management. His textbook, Investments, coauthored by Alex Kane and Alan Marcus, now in its eleventh edition, is the market leader. His other textbook Financial Economics coauthored by Nobel-Prize winning economist Robert C. Merton has been translated into nine languages. In 2007 the Retirement Income Industry Association gave him their Lifetime Achievement Award for applied research. Currently he serves as senior advisor to the Investments and Wealth Institute and consults for a number of financial firms including Dimensional Fund Advisors. In 2019 the Plan Sponsors Council of America awarded him their Lifetime Achievement Award. Zvi's website is zvibodie.com (not bodie.com, which belongs to a ghost town in California).

Dirk Cotton is a retired executive of America Online (AOL) who holds a bachelor's degree in computer science and an MBA and researches, speaks and writes about retirement finance at his nationally-recognized blog, The Retirement Cafe. His 2015 paper on sequence of returns risk won the Retirement Management Journal’s Thought Leadership Award. He is also a Thought Leader and contributor to Advisor Perspectives.

We would like to thank Bob Huebscher for numerous contributions to this paper and for his outstanding editing of the final product. We also thank Robert Merton for suggesting that this was an important topic to cover and for inspiring us to write it.

More Alternative Investments Topics >