Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

The business cycle has progressed to the point where the front end will outperform the long end of the yield curve.

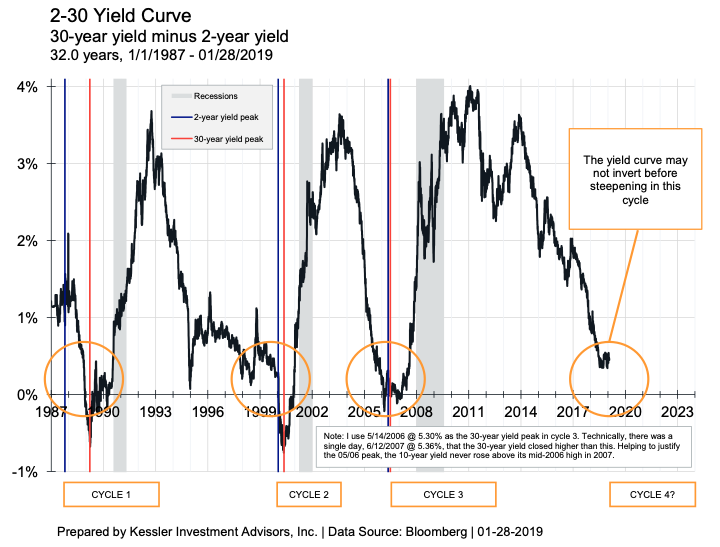

In the last three recession eras (cycles 1-3 in the chart below), yields at the front end of the yield curve moved lower more than the long end of the yield curve, by a lot – an average of 1.8 times as much. This happened because as the Fed lowered rates during those recessions, the front end of the yield curve (e.g. the 2-year U.S. Treasury) followed changes in the lowered Federal Funds rate, while the long-end of the yield curve began to anticipate the stimulus of lowered rates having a positive future effect, causing them to fall less.

In bond lingo, the yield curve steepened.

Because of this, holding duration-equivalent amounts of 2-year Treasuries (using leverage) will outperform the rest of the U.S. Treasury yield curve in a recession-era environment. In recent articles, I have advocated holding positions primarily at the long end of the curve. But enough evidence exists to begin moving U.S. Treasury exposure forward on the curve. Let me explain why.

A less hawkish Fed means inversion may not happen

The chart below shows the difference between the 30-year and 2-year yields over time. Quite simply, when the line rises, it is a better time to own the 2-year; when the line falls, it is better time to own the 30-year (assuming equal amounts of duration exposure). During recession eras (cycles 1-3), the line tends to go up.

In the past three cycles, this line fell below zero (yield curve inversion) before it turned around and went up. The yield curve inverted because the Fed raised rates above the rate of the 30-year before everything turned around. Currently, the 30-year yield is 45 basis points above the 2-year yield (as of 1/28/2019).

It would seem logical to wait for the yield curve to invert before moving to the short-end of the yield curve, but there is a good reason why an inversion may not happen before the market begins to price in lower Fed rates. As I pointed out before, the Fed’s mandate is a coincident indicator (labor) and a lagging indicator (inflation). Because of this, the Fed has historically tightened well after when some leading indicators began to falter….waiting longer to be sure the cycle has turned.

But, as we are approaching the fourth recession in which rich data and asset prices have existed (I consider the modern era of rich data to have begun around 1990), there is a greater awareness and trust in leading indicators amongst the Fed. In the period after the last Fed rate hike on December 19 of last year, and before any economic data has blatantly suggested a recession, a whole chorus of FOMC members have laid the groundwork for not raising rates in March (including usual hawk Esther George, and past chairperson, Janet Yellen). On its face, this is just a posture of patience with a presumed bias towards raising later in the year, but, I doubt there will be enough time to raise again.

An important corollary of my prior article is that no matter what the proximate causes are to each recession-era (i.e, the savings and loan crisis in the early 1990s, the Dot-Com crisis in the early 2000s, or the sub-prime crisis in 2006-2008), they share common timing. Narratives wrap around the recession after the fact, but the cycle itself progresses with or without the story. Once certain economic signposts pass by (housing market falling, yield curve flattening, expansion age), the rest of the recession era events come along with some regularity. We know that housing peaked about a year ago, the expansion is 9.5 years old, and the yield curve is very flat (e.g., the 2-year and 5-year are nearly the same yield as-of 1/28/2019). Past timing would suggest that the window for raising rates is quickly closing.

In the last three recession eras, the yield curve began to steepen near the last Fed raise in the cycle. If December 19, 2018 was the last raise in this cycle, then the yield curve will cyclically steepen from here. Conversely, if the last raise is still to come (or even just the expectation of one), then the yield curve could flatten until then. Either way, begin shifting interest rate exposure towards the front of the yield curve.

Eric Hickman is president of Kessler Investment Advisors, Inc., an advisory firm located in Denver, Colorado specializing in U.S. Treasury bonds.

Read more articles by Eric Hickman